Executive Summary

Income Tax

- Expenses through International Credit card will comes into the specified limit of LRS and TCS is applicable on the same.

- Changes proposed in Rule 11UA to calculate the FMV of shares and charged excess amount u/s 56(2)(viib).

- Few investors/entities are excluded from the purview of Section 56(2)(viib).

- Leave encashment limit increased to Rs.25,00,000 w.e.f. 01.04.2023.

- CBDT releases the guidelines for Complete scrutiny for FY 2023-24.

- India has signed DTAA with Chile.

Goods & Services Tax (GST) & Customs

- GSTN added new facility to verify document reference number (RFN).

- Extension time limit for filling GSTR-1 whose principal place of business in the State of Manipur.

- GSTN issues advisory on Deferment of Implementation of Time Limit on Reporting Old e-Invoices

- CBIC rolls out Automated Return Scrutiny Module for GST returns.

- E-invoices limit is reduced to Rs.5Crore from Rs.10Crore w.e.f.01.08.2023.

Companies Act 2013/ Other Laws

- Application for removal of Company’s name to be made to Registrar C-PACE.

- MCA has notified Companies (Removal of Names of Companies from the Register of Companies) Second Amendment Rules, 2023

- MCA streamlines approvals for mergers vide Companies (Compromises, Arrangements and Amalgamations) Amendment Rules, 2023.

- RBI withdraws Rs. 2000 notes from circulation; will continue to remain a legal tender

- RBI mandates banks to maintain daily data on Rs. 2000 banknotes’ deposits/exchange in a prescribed format

- SEBI tweaks ICDR norms; underwriting agreement now a pre-requisite for IPO filings

- Clearing Corps in Commodity Derivatives can now align Core Settlement Guarantee Fund as per SEBI circulars

![]()

![]()

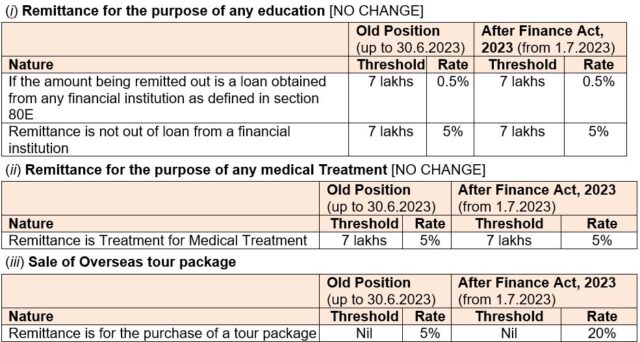

• CBDT vide Press Release dated 19.05.2023 has clarify that the use of international credit cards for meeting his/her expenses by a person when he is abroad will come under the purview of LRS, earlier only Debit card was covered. Further, to avoid any procedural ambiguity, it has been decided that any payments by an individual using their international Debit or Credit cards upto Rs. 7 lakhs per financial year will be excluded from the LRS limits and hence, will not attract any TCS. Existing beneficial TCS treatment for education and health payments will also continue.

• CBDT vide Press Release dated 19.05.2023 has clarify that the use of international credit cards for meeting his/her expenses by a person when he is abroad will come under the purview of LRS, earlier only Debit card was covered. Further, to avoid any procedural ambiguity, it has been decided that any payments by an individual using their international Debit or Credit cards upto Rs. 7 lakhs per financial year will be excluded from the LRS limits and hence, will not attract any TCS. Existing beneficial TCS treatment for education and health payments will also continue.

Instances have come to notice where the LRS payments are disproportionately high when compared to the disclosed incomes. Therefore, TCS rates are increased. Primary Impact only on investment in assets such as real estate, bonds, stocks outside India by HNI and tour travel packages or gifts to non-residents.

TCS rates with the changes brought about in Finance Act, 2023 are tabulated as under

- CBDT vide Press Release dated 05.2023 has proposes changes to Rule 11UA in respect of ANGEL TAX and also proposes to notify Excluded Entities.

Proposed changes in Rule 11 UA :

- Rule 11UA currently prescribes two valuation methods with respect to valuation of shares namely, Discounted Cash Flow (DCF) and Net Asset Value (NAV) method for resident investors. It is proposed to include 5 more valuation methods, available for non-resident investors, in addition to the DCF and NAV methods of valuation.

Further, where any consideration is received by a company for issue of shares , from any non-resident entity notified by the Central Govt , the price of the equity shares corresponding to such consideration may be taken as the FMV of the equity shares for resident and non-resident investors subject to the following:

- To the extent the consideration from such FMV does not exceed the aggregate consideration that is received from the notified entity and

- The consideration has been received by the company from the notified entity within a period of ninety days of the date of issue of shares which are the subject matter of valuation.

- On similar lines, price matching for resident and non-resident investors would be available with reference to investment by Venture Capital Funds or Specified Funds.

- It is proposed that the valuation report by the Merchant Banker for the purposes of this rule would be acceptable, if it is of a date not more than ninety days prior to the date of issue of shares which are subject matter of valuation.

- Further, to account for forex fluctuations, bidding processes and variations in other economic indicators, etc. which may affect the valuation of the unquoted equity shares during multiple rounds of investment, it is proposed to provide a safe harbor of 10 % variation in value.

The draft Rules on the above lines will be shared for public comments for 10 days, after which these will be notified.

- CBDT vide CIRCULAR NO. 5 OF 2023, DATED 22-05-2023 has issued guidelines for the purposes of removal of difficulties in view of the New Section 194BA inserted by Finance Act 2023. As per new section mmandates a person, who is responsible for paying to any person any income by way of winnings from any online game during the financial year to deduct income-tax on the net winnings in the person’s user account. Tax is required to be deducted at the time of withdrawal as well as at the end of the financial year. Net winning is required to be computed in the manner as may be prescribed. The manner of computation of net winning has now been prescribed in Rule 133 of the Income-tax Rules, 1962, videnotification no. 28/2023, dated 22nd May, 2023. There are multiple FAQs are issued in this circular. Net winnings for the purposes of calculating tax required to be deducted under section 194BA shall be calculated as under

Net winnings = A-(B+C), where

A = Amount withdrawn from the user account;

B = Aggregate amount of non-taxable deposit made in the user account by the owner of such account during the financial year, till the time of such withdrawal; and

C = Opening balance of the user account at the beginning of the financial year

- CBDT vide NOTIFICATION F.NO.225/66/2023/IT A-II, DATED 24-05-2023 has release the guidelines for Compulsory selection of return for complete scrutiny during FY 2023-24.

- CBDT vide NOTIFICATION 29&30/2023, DATED 24-05-2023 has exempt the certain class of Non-resident investor from the ambit of Section 56(2)(viib). Finance Act 2023 has amended the provisions of Section 56(2)(viib) and as per the amendments Non-resident also comes into purview of Angel Tax. CBDT gives the clarity that few entities and also start-ups which fulfilles the conditions are not covered by the provision.

- CBDT vide NOTIFICATION 31/2023, DATED 24-05-2023 has increased the leave encashment limit to Rs.25,00,000 from Rs.3,00,000 u/s 10(10AA) w.e.f. 01.04.2023.

![]()

![]()

- CBDT vide NOTIFICATION No. 24/2023, DATED 03-05-2023 has notifies the Agreement and Protocol between the Government of the Republic of India and the Government of the Republic of Chile for the elimination of double taxation and the prevention of fiscal evasion and avoidance with respect to taxes on income, was signed at Chile on the 9th day of March, 2020.

*******

![]()

![]()

- As per Notification No.10/2023 Dated 10/05/2023 CG on the recommendations of the Council, hereby makes the following further amendment in the notification No.13/2020 In the notification first paragraph with effect from the 1st day of August, 2023, for the words “ten crore rupees”, the words “five crore rupees” shall be substituted.

As per Notification No.11/2023 Dated 24/05/2023 CG on the recommendation of council make following amendment in the Notification NO 83/2020 In the said notification, after the third proviso, the following proviso shall be inserted, namely:-―Provided also that the time limit for furnishing the details of outward supplies in FORM GSTR-1of the said rules for the tax period April, 2023, for the registered persons required to furnish return under sub-section (1) of section 39 of the said Act whose principal place of business is in the State of Manipur, shall be extended till the thirty-first day of May, 2023..This notification shall be deemed to have come into force with effect from the 11thday of May, 2023.

- GSTN added new facility to verify document reference number (RFN) mentioned on offline communication issued by state GST authority on 28/04/2023Under this feature, the State Tax office can generate a RFN for the physically generated correspondence sent to the taxpayer, which can be validated by the taxpayer (both pre-login and post-login). The facility to verify RFN of System-generated documents, once deployed, shall also be available in a seamless manner using the same link.

- CBIC rolls out Automated Return Scrutiny Module for GST returns in ACESGST backend application for Central GST officers. This module will enable the officers to carry out scrutiny of GST returns of Centre Administered Taxpayers selected on the basis of data analytics and risks identified by the system In the module, discrepancies on account of risks associated with a return are displayed to the GST officers. Implementation of this Automated Return Scrutiny Module has commenced with the scrutiny of GST returns for FY 2019-20, and the requisite data for the purpose has already been made available on the GST officers’ dashboard.

GSTN issues advisory on Deferment of Implementation of Time Limit on Reporting Old e-Invoices that it has been decided by the competent authority to defer the imposition of time limit of 7 days on reporting old e-invoices on the e-invoice IRP portals for taxpayers with aggregate turnover greater than or equal to 100 crores by three months. The next date of implementation will be shared by them.

*******

![]()

![]()

- Application for removal of Company’s name to be made to Registrar C-PACE.

The Ministry of Corporate Affairs notified the Companies (Removal of Names of Companies from the Register of Companies) Amendment Rules, 2023 to amend the Companies (Removal of Names of Companies from the Register of Companies) Rules, 2016. The provisions will come into force on 1-5-2023.

Key Points:

- Rule 4 (1) relating to Application for removal of name of company has been revised which says that an application for removal of name of company under Section 248 (2) will now be made to the Registrar, Centre for Processing Accelerated Corporate Exit in Form No. STK-2 with a fee amounting to Rs. 10,000.

2. Rule 4 (3-A) relating to Application for removal of name of company has been inserted. The Registrar, Centre for Processing Accelerated Corporate Exit will be established under Section 396 (1) and this Registrar of Companies has the power of exercising functional jurisdiction of processing and disposal of applications made in Form No. STK-2 and all matters related to Section 248 having territorial jurisdiction all over India.

- Form No. STK- 2 relating to “Application by company to ROC for removing its name from register of companies” has been revised.

4. Form No. STK- 6 (Public Notice) has been revised.

- Form No. STK- 7 relating to “Notice of Striking Off and Dissolution” has been revised.

- MCA tightens norms for closure of firms vide Companies (Removal of Names of Companies from the Register of Companies) Second Amendment Rules, 2023

The Ministry of Corporate Affairs notified the Companies (Removal of Names of Companies from the Register of Companies) Second Amendment Rules, 2023 to amend the Companies (Removal of Names of Companies from the Register of Companies) Rules, 2016. The provisions came into force on 10-5-2023.

Key Points:

- Rule 4 relates to “Application for removal of name of company” which says that an application for removal of name of a company under Section 248(2) will be made to the Registrar, Centre for Processing Accelerated Corporate Exit in Form No. STK-2 along with fee of Rs. 10000.

- New Provisions have been inserted regarding the same:

- The Company cannot file an application unless it has filed overdue financial statements and overdue annual returns up to the end of the financial year in which the company ceased to carry out its business operations.

- Where the Registrar’s action has already been initiated against the Company, it can only file the application for removal of names, after filing pending financial statements and annual returns.

- A Company will not be allowed to file an application for removal of names, once the Registrar has issued notice for publication.

- MCA streamlines approvals for mergers vide Companies (Compromises, Arrangements and Amalgamations) Amendment Rules, 2023.

The Ministry of Corporate Affairs notified the Companies (Compromises, Arrangements and Amalgamations) Amendment Rules, 2023 to amend the Companies (Compromises, Arrangements and Amalgamations) Rules, 2016.

Key Points:

- Rule 25 has been modified in order to streamline approvals for mergers by way of deemed approvals. Rule 25 (5) now provides that if no objection/suggestion is received within a period of 30 days from the Registrar of Companies/ Official Liquidator, and if the Central Government (‘CG’) thinks that the scheme is in the public interest or in the interest of creditors, CG can issue a confirmation order of such scheme of merger or amalgamation in Form No. CAA.12 within a period of 15 days after the expiry of said 30 days. If the CG does not issue a confirmation order within 60 days, it will be deemed that there is no objection, and a confirmation order will be issued.

- Rule 25 (6) provides that if the objections/suggestions are received within 30 days, the CG can take following actions:

- A confirmation order will be issued within 30 days, if the objections/ suggestions are deemed unsustainable, and the CG thinks that the scheme is in the public interest or the interest of creditors.

- In case CG thinks that the scheme is not in the public interest or the interest of creditors, CG can file an application stating the objections/ opinion to consider scheme under 232 of Companies Act, 2013 before the Tribunal within 60 days. If the Central Government does not issue a confirmation order or file an application.

*******

![]()

![]()

- RBI withdraws Rs. 2000 notes from circulation; will continue to remain a legal tender

The Reserve Bank of India (RBI) on 19.05.2023 announced the withdrawal of the Rs 2,000 banknote from circulation with the public being “encouraged” to deposit or exchange the notes at bank branches until September 30, 2023. At the same time, the central bank maintained that these notes will enjoy legal tender status even beyond the September 30 deadline.

- RBI mandates banks to maintain daily data on Rs. 2000 banknotes’ deposits/exchange in a prescribed format

In furtherance to the RBI’s direction on the withdrawal of Rs. 2,000 notes from circulation, the banks have been advised to provide appropriate infrastructure at the branches such as shaded waiting space, drinking water facilities, etc. considering the summer season.

Further, Banks shall have to maintain daily data on the deposit and exchange of Rs. 2000 banknotes in the prescribed format (specifying date, bank name, and amount deposited/exchanged) and submit the same as and when required.

.

*******

![]()

![]()

- SEBI tweaks ICDR norms; underwriting agreement now a pre-requisite for IPO filings

The SEBI has notified amendment in SEBI (ICDR) Regulations, 2018. As per the amended norms, if the issuer making an IPO, desires to have the issue underwritten, it shall, prior to the filing of the prospectus, enter into an underwriting agreement with the merchant bankers or stock brokers, indicating the maximum number of specified securities they shall subscribe to, at a predetermined price which shall not be less than the issue price

- Clearing Corps in Commodity Derivatives can now align Core Settlement Guarantee Fund as per SEBI circulars

Earlier, SEBI issued circulars prescribing norms relating to Core Settlement Guarantee Fund (SGF), Min. Reqd. Corpus of core SGF, etc. for Clearing Corporations (CCs) and Stock Exchanges. SEBI recently received representations to review the target corpus level & to harmonise the methodology for computation of core SGF corpus in Commodity Derivatives Segment. Now, after receiving representations, SEBI directed that the CCs can now align their core SGF in terms of earlier issued SEBI circulars.

*******

![]()

![]()

Disclaimer: Information in this note is intended to provide only a general update of the subjects covered. It is not intended to be a substitute for detailed research or the exercise of professional judgment. KNM accepts no responsibility for loss arising from any action taken or not taken by anyone using this publication. Updates are for the period from 26th Apr till 25th May. 2023.