Contents

Highlights- Budget 2019-20

Highlights- Economic Survey 2018-19

KNM credentials

Annexure – I to Budget Highlights

1. Highlights- Budget 2018-19

Finance Minister Nirmala Sitharaman presented her first budget, outlining the priorities of Prime Minister Narendra Modi in his second term after a massive election victory.

- Vision for $5 trillion economy driven by investment

- Transforming rural lives

- New Jal Shakti Mantralaya to ensure Har Ghar Jal

- Enhancing ease of direct and indirect taxation

- Strengthening connectivity Infrastructure

- Gandhipedia to sensitize society

- India’s soft power

- Harnessing India’s space abilities

- Enhanced interest deduction for affordable housing loan

- Tax benefits for corporate tax payers

- No scrutiny to check the valuation for ‘Angel Tax’ if start-ups and investors file declaration

- Aadhaar for NRI’s with Indian Passport

- Scheme of faceless electronic tax assessment

- Reform, Perform, Transform agenda: GST, IBC, RERA etc.

- Changing common man’s life: MUDRA, UJJWALA, SAUBHAGYA etc.

DIRECT TAXES

- Personal Income Tax

- No change in income tax slab rates for F.Y. 2019-20 for Individuals/HUF/AOPs/BOI.

| Slab Rates | ||

| Income (INR) | Rate of Tax | |

| Up to INR 250,000* | NIL | |

| INR 250,001 to INR 500,000 | 5% | |

| INR 500,001 to INR 1,000,000 | 20% | |

| Above INR 1,000,000 | 30% | |

*Basic exemption in case of Senior Citizen (Age 60 Years to 79 Years) is INR 300,000 and very senior citizen (Age 80 Years or more) is INR 500,000. There is no change in the exemption for 2019-20.

- Rebate under Section 87A remain unchanged for resident individual (whose income does not exceed 5,00,000) the amount of rebate is 100% of tax calculated before cess or 12,500 whichever is less.

- Surcharge: In case of Individuals/ HUF/ AOPs/BOI Proposed Surcharge are as under levied on categories of whose annual taxable income is as follows:

| Total income | Rate of Surcharge |

| Upto 5 million | Nil |

| Above INR 5 Million to INR 10 Million | 10% |

| Above INR 10 Million to INR 20 Million | 15% |

| Above INR 20 Million to INR 50 Million | 25% |

| Above 50 Million | 37% |

- Surcharge will remain at 12% on persons, other than companies, firms and cooperative societies having income above INR 10 Million.

- Domestic company where Total turnover/Gross receipts in last previous year does not exceed INR 40 Million the rate of income tax shall be applicable 25% in place of 30%.

- Health and Education Cess @ 4% is levied on income tax and surcharge, if any is also same.

- Standard deduction of INR 50,000 in a year shall be allowed instead of Rs.40,000 as compared to last year

Section 80C A new clause (XXV) of Section 80C has been inserted i.e. Central Govt. Employees

contribution under pension scheme referred under section 80CCD-For a fixed period of not less than three years and which is in accordance with scheme notified by CG. (w.e.f. AY 2020‐21).

Section 80CCD In case of central govt employee deduction under this section can be claimed upto 14% of the salary. Earlier the limit was 10%. (w.e.f. AY 2020‐21).

Section 80EEA To provide a deduction in respect of interest up to one lakh fifty thousand rupees on loan taken for residential house property from any financial institution subject to the following conditions:

(i) loan has been sanctioned by a financial institution during the period beginning on the 1st April, 2019 to 31st March 2020.

(ii) the stamp duty value of house property does not exceed forty‐five lakh rupees;

(iii) assessee does not own any residential house property on the date of sanction of loan.

It is also proposed that where a deduction under this section is allowed for any interest, deduction shall not be allowed in respect of such interest under any other provisions of the Act for the same or any other assessment year. (w.e.f. AY 2020‐21).

Section 80EEB Deduction in respect of interest on loan taken for the purchase of an electric

vehicle from any financial institution up to one lakh fifty thousand rupees subject to the following conditions:

- the loan has been sanctioned by a financial institution including a non‐banking financial company during the period beginning on the 1st April, 2019 to 31st March, 2023;

(ii) the assessee does not own any other electric vehicle on the date of sanction of loan.

It is also proposed that where a deduction under this section is allowed for any interest, deduction shall not be allowed in respect of such interest under any other provisions of the Act for the same or any other assessment year. (w.e.f. AY 2020‐21).

Section 80‐IBA It is proposed to amend the said section, so as to modify certain conditions regarding the housing project approved on or after 1st day of September, 2019. The modified conditions are as under:

(i) the assessee shall be eligible for deduction under the section, in respect of a housing project if a residential unit in the housing project have carpet area not exceeding 60 square meter in metropolitan cities or 90 square meter in cities or towns other than metropolitan cities of Bengaluru, Chennai, Delhi National Capital Region (limited to Delhi, Noida, Greater Noida, Ghaziabad, Gurgaon, Faridabad), Hyderabad, Kolkata and Mumbai (whole of Mumbai Metropolitan Region); and

(ii) the stamp duty value of such residential unit in the housing project shall not exceed forty five lakh rupees.

- Corporate Taxation

Corporate Tax of 25% extended to companies with turnover up to INR 4000 million from INR 2500 million in financial year 2017-18 so it will cover 99.3% companies in India. Rest will charge with tax rate 30% in addition to Education cess & Surcharge if any.

Section 35AD/40A/43/43CA/44AD In order to promote other electronic modes of payment, it is proposed to amend the above section so as to include such other electronic mode as may be prescribed, in addition to the already existing permissible modes of payment in the form of an account payee cheque or an account payee bank draft or the electronic clearing system through a bank account. (w.e.f. AY 2020‐21)

Section 40 In case an assessee fails to deduct Tax at Source on any sum paid to a Non-Resident, then if the Non-Resident has filed his return of Income and has disclosed such sum of money

received from the assessee then there will be no disallowance under section 40 (a). (w.e.f. AY 2020‐21

Section 43B It is proposed to amend section 43B of the Act to provide that any sum payable by the assessee as interest on any loan or advances from a deposit‐taking NBFCs and systemically non NBFCs shall be allowed as deduction if it is 43B important deposit‐taking actually paid on or before the due date of furnishing the return of income of the relevant previous year. (w.e.f. AY 2020‐21)

Section 43D The existing provisions of section 43D of the Act, inter‐alia provides that interest income in relation to certain categories of bad or doubtful debts received by certain institutions or banks or corporations or companies, shall be chargeable to tax in the previous year in which it is credited to its profit and loss account actually received, whichever is earlier.

The benefit of this provision is presently available to public financial institutions, scheduled banks, cooperative banks, State financial corporations, State industrial investment corporations and public companies like housing finance companies. With a view to provide a level playing field to certain categories of NBFCs who are adequately regulated, it is proposed to amend section 43D of the Act so as to include deposit‐taking NBFCs and systemically important non deposit‐taking NBFCs within the scope of this section. (w.e.f. AY 2020‐21)

Section 79 Section 79 of the Income Tax Act provides conditions for carry forward and set off of losses in case of a company not being a company in which the public are substantially interested. Clause (a) of this section applies to all such companies, except an eligible start‐up as referred to in section 80‐IAC, while clause (b) applies only to such eligible startup. (w.e.f. AY 2020-21)

Section 80JJAA in order to encourage other electronic modes of payment, it is proposed to amend the above section so as to include such other electronic mode as may be prescribed, in addition to the already existing permissible modes of payment in the form of an account payee cheque or an account payee bank draft or the electronic clearing system through a bank account. (w.e.f. AY 2020‐21)

Section 80LA in order to further incentivize operation of units in IFSC, it is proposed to amend the said section so as to provide that the deduction shall be increased to one hundred per cent for any ten consecutive years. The assessee, at his option, may claim the said deduction for any ten consecutive assessment years out of fifteen years beginning with the year in which the necessary permission was obtained. (w.e.f. AY 2020‐21)

Section 115JB To give benefit to those Companies where NCLT (under cases of oppression and

mismanagement) has suspended its Directors and has appointed Central Government nominee Directors, and its subsidiary and the subsidiary of such subsidiary, for calculating book profit under section 115JB, the aggregate amount of unabsorbed depreciation and loss (excluding depreciation) brought forward shall be allowed to be reduced. (w.e.f. AY 2020‐21)

Section 115‐O Distribution of dividend by companies operating in IFSC, it is proposed to amend the provision of the said section to provide that any dividend paid out of accumulated income derived from operations in IFSC, after 1st April 2017 shall also not be liable for tax on distributed profits. (w.e.f. AY 2020‐21)

Section 115QA The expression “not being shares listed on a recognizes stock exchange is proposed to be omitted. As a result proposed amendment buy back of shares in the case of listed companies will also liable for DDT. (w.e.f. 05.07.2019)

Section 115R To incentivize relocation of Mutual Fund in IFSC, it is proposed to amend the said section so as to provide that no additional income‐tax shall be chargeable in respect of any amount of income distributed, on or after the 1st day of September, 2019, by a Mutual Fund of which all the unit holders are non‐residents and which fulfills certain other specified conditions. (w.e.f. AY 2020‐21)

Section 115UB In order to remove the genuine difficulty faced by Category I and II AIFs , it is proposed to amend section 115UB to provide that

(i) the business loss of the investment fund, if any, shall be allowed to be carried forward and it shall be set‐off by it in accordance with the provisions of Chapter VI and it shall not be passed onto the unit holder;

(ii) the loss other than business loss, if any, shall also be ignored for the purposes of pass through to its unit holders, if such loss has arisen in respect of a unit which has not been held by the unit holder for a period of at least twelve months;

(iii) the loss other than business loss, if any, accumulated at the level of investment fund as on 31st March, 2019, shall be deemed to be the loss of a unit holder who held the unit on 31st March, 2019 in respect of the investments made by him 18 in the investment fund and allowed to be carried forward by him for the remaining period calculated from the year in which the loss had occurred for the first time taking that year as the first year and it shall be set‐off by him in accordance with the provisions of Chapter VI; (iv) the loss so deemed in the hands of unit holders shall not be available to the investment fund for the purposes of chapter VI. (w.e.f. AY 2020‐21)

- International Taxation/ Transfer Pricing

Section 9 of the Act deals with Income deemed to accrue or arise in India. Under the Act, non–residents are taxable in India in respect of income that accrues or arises in India or is received in India or is deemed to accrue or arise in India or is deemed to be received in India. Under the existing provisions of the Act, a gift of money or property is taxed in the hands of donee/receiver, except exemptions given u/s 56(2)(x). Presently, these gifts are made by persons being residents in India to persons outside India and are claimed to be nontaxable in India as the income does not accrue or arise in India. To make these gifts taxable in India, it is proposed to provide that income as referred u/s 2(24)(xviia), arising from any sum of money paid, or any property situate in India transferred, on or after 5th July, 2019 by a person resident in India to a person outside India shall be deemed to accrue or arise in India. However, the gifts to relatives and on account of marriage as provided u/s 56(2)(x) will continue to be exempt. DTAA provisions will also apply. (w.e.f. AY 2020‐21)

Section 9A which deal with off-shore funds has prescribed some condition to be fulfilled for being an eligible investment fund. Certain conditions contained in clause (j) relating to monthly average of the corpus of the fund and clause (m) relating to the remuneration paid by the fund to the eligible fund manager have been relaxed. (w.e.f. AY 2020‐21)

Sec 10(15) Any income by way of interest payable to a non‐resident by a unit located in IFSC in respect of monies borrowed by it on or after 1st day of September, 2019, shall be exempt. (w.e.f. AY 2020‐21)

Section 115A The method of calculation of income‐tax payable by a non‐resident (not being a company) or by a foreign company where the total income includes any income by way of dividend (other than referred in section 115‐O), interest, royalty and fees for technical services; etc. Section 80LA, provides for deduction in respect of certain incomes to a unit located in an IFSC. However, sub‐section (4) of section 115A prohibits any deduction under chapter VIA which includes section 80LA.

In order to ensure that units located in IFSC claim full deduction, it is proposed to amend section 115A of the Act so as to provide that the conditions contained in sub‐section (4) of section 115A shall not apply to a unit of an IFSC for under section 80LA is allowed. (w.e.f. AY 2020‐21)

Section 92CD In this section a clarification has given in regards to the cases where assessment or reassessment has already been completed and modified return of income has been filed by the tax payer under sub-section (1) of said section, the Assessing Officers shall pass an order modifying the total income of the relevant assessment year determined in such assessment or reassessment, having regard to and in accordance with the Advance Pricing Agreement (APA). (w.e.f. 01.09.2019)

Section 92CE It is proposed to amend clause (iii) of the 92CE(1) so as to provide that the secondary adjustment will be applicable where the primary adjustment to transfer price is determined by an advance pricing agreement entered into by the assessee under section 92CC on or after 1st April, 2017.

-It is also proposed to insert a second proviso in sub‐section (1) so as to provide that no refund of any taxes paid, if any, by virtue of provisions of sub‐section (1) as they stood immediately before their amendment by this Bill, shall be claimed and allowed.

-It is proposed to amend said 92CE(2) so as to provide that the interest shall be computed on the excess money or part thereof and that the excess money can be repatriated from any of the associated enterprises of the assessee, which is not resident in India, besides the associated enterprise with which the excess money is available. (w.r.e.f. 01.09.2019)

-It is also proposed to insert sub‐section (2A) in the said section so as to provide that where the excess money or part thereof has not been repatriated in time, besides the existing requirement of calculation of interest, the assessee will have the option to pay additional income tax at the rate of eighteen per cent. on such excess money or part thereof.

-It is also proposed to insert sub‐section (2B) so as to provide that the tax on the excess money or part thereof so paid by the assessee under sub‐section (2A) shall be treated as final payment tax in respect of excess money or part thereof not the of the repatriated and no further credit therefore shall be claimed by the assessee or by any other person in respect of the amount of tax so paid.

-It is also proposed to insert sub‐section (2C) so as to provide that no deduction under any other provision of this Act shall be allowed to the assessee in respect of the amount.

Section 92D provides that the information and document to be kept and maintained by a constituent entity of an international group, and filing of required form, shall be applicable even when there is no international transaction undertaken by such constituent entity.

It is also proposed to provide that information shall be furnished by the constituent entity of an international group to the prescribed authority. (w.e.f. AY 2020‐21)

Section 228A which seeks to provide for tax recovery in cases where details of property of such person are not available but the said person is a resident in India.

The amendment in sub‐section (2) of the said section seeks to provide for tax recovery where details of property of assessee in default are not available but the said assessee is a resident in a foreign country. (w.e.f. 01.09.2019)

Section 286 The word alternate reporting entity is proposed to be omitted in sec 286(9)(a)(i). As a result of the proposed amendment, the amended sub clause seeks to provide that the accounting year in case of an alternate reporting entity, resident in India, whose ultimate parent entity is outside India, shall not mean the previous year but an annual accounting period, with respect to which the parent entity of the international group prepares its financial statements under any law for the time being in force or the applicable accounting standards of the country or territory of which such entity is resident.( w.r.e.f 01.04.2017)

- Capital Gain

Section 47 With a view to provide tax‐neutral transfer of certain securities by Category III Alternative Investment Fund (AIF) in IFSC, it is proposed to amend the said section so as to provide that any transfer of a capital asset, specified in the said clause by such AIF, of which all the unit holders are non‐resident, are not regarded as transfer subject to fulfillment of specified conditions.

It is also proposed to widen the types of securities listed in said clause by empowering the Central Government to notify other securities for the purposes of this clause. (w.e.f. AY 2020-21)

Section 50C In order to encourage other electronic modes of payment, it is proposed to amend the above section so as to include such other electronic mode as may be prescribed, in addition to the already existing permissible modes of payment in the form of an account payee cheque or an account payee bank draft or the electronic clearing system through a bank account. (w.e.f. AY 2020-21)

Section 50CA The provision of sec 50CA for transfer of shares specified in sec 56(2)(x) is not applicable where consideration for transfer of share is approved by specified authorities and the person transferring the shares has no control over such determination of consideration. (w.e.f. AY 2020-21)

Section 54GB The following conditions specified u/s 54GB to claim exemption from capital gain arising from the transfer of LTCA being a residential property owned by the eligible assessee are proposed to be relaxed:

(i) extend the sun set date of transfer of residential property for investment in eligible start‐ups from 31st March 2019 to 31st March 2021;

(ii) relax the condition of minimum shareholding of fifty per cent of share capital or voting rights to twenty five per cent.

(iii) relax the condition restricting transfer of new asset being computer or computer software from the current five years to three years. (w.e.f. AY 2020-21)

Section 111A Clause (a) of the Explanation to section 111A provides that the “equity oriented fund” shall have the meaning assigned to it in the Explanation to clause (38) of section 10. It is proposed to amend the said Explanation so as to provide that “equity oriented fund” shall have the meaning assigned to it in clause (a) of the Explanation to section 112A. (w.e.f. AY 2020-21)

- Income From Other Sources

Section 56(2)(x)(A) In order to encourage other electronic modes of payment, it is proposed to amend the above section so as to include such other electronic mode as may be prescribed, in addition to the already existing permissible modes of payment in the form of an account payee cheque or an account payee bank draft or the electronic clearing system through a bank account.

The specified in provision of sec 50CA for transfer of shares sec 56(2)(x) is not applicable where consideration for transfer of share is approved by specified authorities and the person transferring the shares has no control over such determination of consideration. (w.e.f. AY 2020-21)

Sec 56(viib) The scope of benefit allowed to VCF is proposed to be extended to a specified fund which has been defined as under:‘(aa) “specified fund” means a fund established or incorporated in India in the form of a trust or a company or a limited liability partnership or a body corporate which has been granted a certificate of registration as a Category II Alternative Investment Fund and is regulated under the Securities and Exchange Board of India (Alternative Investment Fund) Regulations, 2012 made under the Securities and Exchange Board of India Act, 1992; (ab) “trust” means a trust established under the Indian Trusts Act, 1882 or under any other law for the time being in force; (w.e.f. AY 2020-21)

Sec 56(2)(viii) The existing provisions pertain to the above clause were incorrectly referring to sec 145A(b) which was omitted/substituted by new sec 145A by finance act 2017 and therefore in the absence of any provisions similar to any provisions in the new sec 145A similar to those of persubstituted 145A(b), there was an anomaly since instead of substituted sec 145A another sec 145B was having a reference. The anomaly has been resolved by making a reference to 145B(1) with retrospective effect. (w.r.e.f. AY 2017-18)

- Permanent Account Number (PAN) /Income Tax Return (ITR)

Section 139 Mandatory furnishing of ITR by certain persons :In order to ensure that persons who enter into certain high value transactions do furnish their return of income, it is proposed to amend section 139 of the Act so as to provide that a person shall be mandatorily required to file his return of income, if during the previous year, he-

- has deposited an amount or aggregate of the amounts exceeding INR 10 Million in one or more current account maintained with a banking company or a cooperative bank; or

- has incurred expenditure of an amount or aggregate of the amounts exceeding two lakh rupees for himself or any other person for travel to a foreign country; or

- has incurred expenditure of an amount or aggregate of the amounts exceeding one lakh rupees towards consumption of electricity; or

- fulfils such other prescribed conditions, as may be prescribed.

A person who is claiming rollover benefits on investment in a house or a bond or other assets, under sections 54, 54B, 54D,54EC, 54F, 54G, 54GA and 54GB of the Act, shall also, necessarily be required to furnish a return, if before claim of the rollover benefits, his total income is more than the maximum amount not chargeable to tax. (w.e.f. AY 2020‐21).

Section 139A Inter-changeability of PAN & Aadhaar and mandatory quoting in prescribed transactions. Amendment of section Ay 2020‐21 The Aadhar and PAN have been made interchangeable. Further, it shall be mandatory on a person to quote and verify his PAN/Aadhar No. in respect of certain specified transactions At the same time it is proposed to provide that every person receiving such 139A documents shall also ensure that the PAN or the Aadhaar number as the case may transactions. time, number, be, has been duly quoted. (w.e.f. AY 2020‐21)

Section 139AA The existing proviso to the sub‐section (2) of section 139AA, provides that the PAN allotted to a person shall be deemed to be invalid, in case the person fails to intimate the Aadhaar number, on or before the notified date. In order to protect validity of transactions previously carried out through such PAN, it is proposed to amend the said proviso so as to provide that if a person fails to intimate he Aadhaar number, the PAN allotted to such person shall be made inoperative in the prescribed manner. (w.e.f. 01.09.2019)

Section 140A The existing provisions of section 140A contain provisions relating to computation of tax liability after allowing credit for prepaid taxes and certain admissible reliefs, credits etc. However, the relief under section 89 is not specifically mentioned in above section, which is resulting into genuine hardship in the case of taxpayers who are eligible for this relief. In view of the above, it is proposed to amend section 140A as to provide that computation of tax liability shall be made after allowing relief under section 89. (w.r.e.f. 01.04.2017)

- Tax deducted at Sources (TDS)

Section 194DA The rate of TDS is proposed to increase to 5% from the existing of 1%. (w.e.f. 01.09.2019)

Section 194‐IA As per the clarification sale consideration for the immovable property shall include the payments made towards some of such payments like those for rights to amenities like club membership fee, car parking fee, electricity and water facility fees, maintenance fee, advance fee etc. (w.e.f. 01.09.2019)

Section 194M TDS to be deducted by Individual and HUF (Other then those required to deduct the same under section 194C/194J of the Act) in respect of payments akin to the nature as referred in section 194C/194J of the Act in case the aggregate of such payments exceeds Rs. 50 Lakhs in a year. TDS to be deposited through PAN and there is no required to obtain TAN. (w.e.f. 01.09.2019)

Section 194N TDS @ 2% on cash withdrawal from account maintained with Bank, Banking Co‐operative Society, & Post Office if such cash withdrawal exceeds Rs 1 crore during the previous year. The provisions are not applicable in case the payee is Government, Banking Company or Banking Cooperative Society, post office, White Label ATM operator, Banking correspondents and such other class of persons as the Central Government Specify. (w.e.f. 01.09.2019)

Section 195 It is proposed to amend the provisions of sec 195(2) to allow for prescribing the form and manner of application to the Assessing Officer and also for the manner of determination of appropriate portion of sum chargeable to tax by the Assessing Officer through ONLINE mechanism. Similar amendment is also proposed to be made in sub‐section (7) of section 195 which are applicable to specified class of persons or cases. (w.e.f. 01.09.2019)

Section 197 The newly inserted section 194M shall also be amenable to certificate of deduction at lower rate. (w.e.f. 01.09.2019)

Section 201 In case an assessee fails to deduct Tax at Source on any sum paid to a Non- Resident, then if the Non-Resident has filed his return of Income and has disclosed such sum of money received from the assessee then the assesse shall not be deemed to be an assessee in default under section 201 (1).

Consequently, Section 201 (1A) is also being amended to provide that Interest on TDS shall also be required to be paid only till the date of filing of ITR by such Non Resident. (w.e.f. 01.09.2019)

It is also proposed to amend section 201(3) of the act for being treated the assessee in default.

Section 206A The present section provided for filing a statement of interest paid to residents without deduction of TDS at source if the amount of interest paid was upto Rs.10,000/‐. The aforesaid limit of Rs 10 000/‐ where the payee was a banking company was raised to Rs.40,000/‐ by finance Act NO. 1 of 2019. Also there was no provision of adding, deleting or modifying the details.

As per the newly substituted section the monetary limit as increased by Finance Act 2019 as well as relaxation to delete, add, update the information or to file correction statement has been provided. (w.e.f. 01.09.2019)

- Charitable Trust

Section 12AA It is proposed to give sufficient powers to Pr.CIT/CIT to verify the genuiness of the activity of the trust or institution under the Income Tax Act or any other law governing the trust or institution and if non compliance have been found he may by an order in writing cancel the registration of such trust or institution. (w.e.f. 01.09.2019)

Section 13A AY 2020‐21 In order to encourage other electronic modes of payment, it is proposed to amend the above section so as to include such other electronic mode as may be prescribed, in addition to the already existing permissible modes of payment in the form of an account payee cheque or an account payee bank draft or the electronic clearing system through a bank account.

- Other Major Amendments

Sec 10(12A) Sixty per cent of the total amount payable to the person at the time of closure or his opting out of the scheme. Earlier the limit was 40% of the amount

Section 143 The existing provisions of section 143 contain provisions relating to computation of tax liability after allowing credit for prepaid taxes and certain admissible reliefs, credits etc. However, the relief under section 89 is not specifically mentioned in above section, which is resulting into genuine hardship in the case of taxpayers who are eligible for this relief. In view of the above, it is proposed to amend section 143 as to provide that computation of tax liability shall be made after allowing relief under section 89. (w.r.e.f. 01.04.2007)

Section 234A/B/C In the ITR forms, the tax liability was computed after allowing the relief permissible to an assessee under Section 89(1). It was thereafter on this tax on total income as determined that interest chargeable under Section 234A, 234B & 234C were to be computed, based on the computation as per ITR forms.( w.r.e.f. 01.04.2007)

Section 239 A form for claiming refund was to be filed under Rule 41, where Form ‐30 was the prescribed form for claiming the refund of income tax. In order to mitigate the filing of Form No. 30, the claim of refund made by filing the IT returns would be a valid claim of refund of income tax and there shall not be any requirement to claim the refund of taxes through/by filing Form No. 30. Thus ITR filed claiming refund of taxes would be enough. (w.e.f. 01.09.2019)

Section 246A Under the proposed amendments, the AO will only pass an order modifying the assessment or reassessment already made and will not be able to assessee or reassess, denovo. Since there will be no assessment or reassessment, there would not be any consequential assessment or reassessment order which could be appealed against. further, there would be an order modifying the earlier assessment and reassessment which has been made appealable now. (w.e.f. 01.09.2019)

Section 269SS/ST/T In order to encourage other electronic modes of payment, it is proposed to amend the above sections so as to include such other electronic mode as may be prescribed, in addition to the already existing permissible modes of payment/receipt in the form of an account payee cheque or an account payee bank draft or the electronic clearing system through a bank account. (w.e.f. 01.09.2019)

Section 269SU it is proposed to insert a new section 269SU in the Act so as to provide that every person, carrying on business, shall, provide facility for accepting payment through the prescribed electronic modes, in addition to the facility for other electronic modes of payment, if any, being provided by such person, if his total sales, turnover or gross receipts in business exceeds fifty crore rupees during the immediately preceding previous year. (w.e.f. 01.11.2019)

Section 270AThis section relates to impositions of penalty for under reported and mis reported income. Where an assessee had filed a return of income for the first time in pursuance of a notice u/s 148 of the act he could have contended that there is no under reported or mis reported income. Various amendments have been made to 270A(2), 270A(3) and 270A(10) so as to provide that where return is furnished for the first time under section 148, a person shall be considered to have under‐reported his income, if the income or deemed income assessed is greater than the maximum amount not chargeable to tax. (w.r.e.f. A.Y 2017‐18

Section 271DB The failure to provide facility for electronic modes of payment prescribed under section 269SU shall attract penalty of a sum of five thousand rupees, for every day during which such failure continues. However, the penalty shall not be imposed if the person proves that there were good and sufficient reasons for such failure. Any such penalty shall be imposed by the Joint Commissioner. (w.e.f. 01.11.2019)

Section 271FAA Presently the penalty is imposable only in respect of reporting entities being prescribed reporting financial institution as referred u/s 285BA(1)(k). There was an anomaly wherein penalty u/s 271FFA was not imposable in case of failure by those reporting entities as referred under clauses (a) to (j) of section 285BA(1).

The amendment proposes to omit the reference to clause (k) and thus to ensure correct furnishing of information in the SFT and widen the scope of penalty to cover all the reporting entities under section 285BA . (w.e.f. 01.09.2019)

Section 272B As per section 139A, it shall be mandatory on a person to quote and verify his PAN/Aadhar No. in respect of certain specified transactions. At the same time, it is proposed to provide that every person receiving such documents shall also ensure that the PAN or the Aadhaar number, as the case may be, has been duly quoted and verified.

In case of each such default, the person required to authenticate and specify the PAN [the person entering the transaction] and the other person in receipt of such documents relating to the quoting of PAN/Aadhar and its verification shall each be liable to a penalty of Rs.10,000/‐ . (w.e.f. AY 2020-21)

Section 276CC The monetary limit specified in class 2 of the proviso to sec 276CC has been increased to Rs 10,000/‐ from the existing limit of Rs 3000/‐ while computing the tax payable for this clause self assessment tax and TCS if any paid before the expiry of A.Y. will also be considered. (w.e.f. AY 2020-21)

Section 285BA The present requirement of reporting u/s 285BA was prescribed under clauses (a) to (k) of 285BA(1). It is proposed to obtain information by widening the scope of furnishing of statement of financial transactions by mandating furnishing of statement by certain prescribed persons other than those who are currently furnishing the same. The power has been assumed by insertion of clause (l) of section 285BA(1).

Presently upon filing of a defective SFT return, an opportunity was permitted to the reporting entity to rectify the defect and in case of failure to rectify the defect within the said period of days or such extended period the SFT return was treated as invalid , and provisions of the act would apply as if there was a failure to furnish the SFT. The proposed amendment seeks to provide that reporting entity had furnished inaccurate information in the statement. (w.e.f. 01.09.2019)

Rule 68B Clause 68 of the Bill seeks to amend rule 68B of the Second Schedule of the Income‐tax Act relating to time limit for sale of attached immovable property. Sub‐rule (1) of the said rule provides that no sale of immovable property attached towards the recovery of tax, penalty, etc., shall be made after the expiry of three years from the end of the financial year in which the order giving rise to a demand of any tax, interest, fine, penalty or any other sum, for the recovery of which the immovable property has been attached, has become conclusive or final, as the case may be.

It is proposed to amend the said sub‐rule so as to extend the said period from three years to seven years.

It is further proposed to insert a new proviso in the said sub‐rule so as to provide that the Board may, for reasons to be recorded in writing, extend the aforesaid period by a further period not exceeding three years. (w.e.f. 01.09.2019)

INDIRECT TAXES

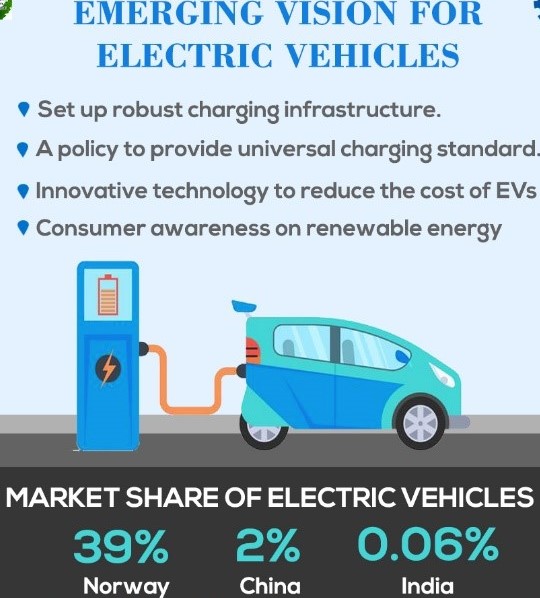

- GST Rate reduced on electric vehicles from 12% to 5%.

- Proposed to move to an electronic invoice system wherein invoice details will be captured in a central system at the time of issuance.

- Custom duty is being increased on items such as cashew kernels, PVC, Vinyl flooring, tiles, metal fittings, etc.

- To promote domestic manufacturing, custom duty reductions are being proposed on certain raw materials and capital goods such as CRGO sheets, amorphous alloy, etc.

- Export duty is being rationalised on raw and semi-finished leather to provide relief to this sector.

- Proposes to increases Special additional Excise Duty and Road and Infrastructure cess each by one rupee a litre on petrol & diesel. It is also proposed to increase custom duty on gold and other precious metals from 10% to 12.5%.

- Tobacco products and crude attract National Calamity and Contingent duty.

- A Legacy Dispute Resolution Scheme that will allow quick closure of litigations from pre-GST regime.

Major Amendments

| Central Goods and Service Tax, 2017 | |

| A | For facilitating trade or consumer |

| 1 | Providing for a composition scheme for supplier of services or mixed suppliers (not eligible for the earlier composition scheme) having an annual turnover of upto Rs 50 lakhs in preceding financial year. [section10 ] |

| 2 | Enhancing the threshold exemption limit from Rs. 20 lakhs to an amount exceeding Rs. 40 lakhs for a supplier of goods [section 22]. |

| 3 | Providing for furnishing return on annual basis and quarterly payment of taxes by a composition dealer [section 39] |

| 4 | Prescribing that specified suppliers shall have to mandatorily give the option of specified modes of electronic payment to their recipients [New section 31A]. |

| 5 | Empower the Commissioner to extend the due date for furnishing of (i) Annual return and Re-conciliation statement [section 44] (ii) Monthly and Annual Statement by an e-commerce operator [section 52] |

| 6 | Providing facility to the registered person to transfer an amount from one head to another head in the electronic cash ledger [section 49] |

| 7 | Providing for charging interest only on the net cash tax liability [section 50] |

| 8 | Enable the Central Government to disburse refund amount of state taxes to the taxpayers [section 54] |

| 9 | Providing for constitution, qualification, appointment, tenure, conditions of services of the National Appellate Authority for Advance Ruling and the procedures for filing of appeals and rectification of orders. To empower the National Appellate authority at par with civil courts [sections 95, 101A, 101B, 101C, 102, 103,104,105, 106] |

| B | For improving compliance |

| 10 | Prescribing mandatory Aadhaar authentication for specified class of existing/new taxpayers [section 25] |

| C | Miscellaneous |

| 11 | Empowering the National Anti-profiteering Authority to impose penalty equivalent to 10% of the profiteered amount [section 171] |

| CUSTOMS ACT, 1962 | |||

| A | For facilitating trade | ||

| 1 | Allowing furnishing of departure manifest by a person notified by the Central Government [ section 41]. | ||

| B | For improving compliance | ||

| 2 | Introducing provisions for verification of Aadhar or any other identity and other compliance by a person for protecting the interests of revenue or to prevent smuggling [New section 99B] | ||

| 3 | Provision to enable the proper officer to scan or screen, with the prior approval, any person who has any goods liable to confiscation secreted inside his body and to enable the magistrate to take action upon the report of scanning by the proper officer [Section 103]. | ||

| 4 | Empowering proper officer of customs to arrest a person who has committed an offence outside India or Indian Customs waters and to make certain offences as cognizable and non-bailable [section 104] | ||

| 5 | (a) Empowering the proper officer to provisionally attach any bank account for safeguarding the government revenue and prevention of smuggling [section110]. (b) Providing powers to release bank account provisionally attached under section 110 on fulfilment of certain conditions [ section 110A]. | ||

| 6 | Provide for penalty on any person who has obtained any instrument by fraud, collusion , wilful misstatement or suppression of facts which is utilised for payment of duty [New section 114 AB] | ||

| 7 | Provide for making the offence punishable if the instrument obtained by fraud, collusion, wilful misstatement or suppression of facts, is used for making payment of duty exceeding 50 lakh rupees [section 135] | ||

| 8 | Enhancing maximum penalty to (a) Rs 4 lakh for violation of provisions of the Act; (b) Rs 2 lakh for violation of Rules or Regulation [section 158] | ||

| C | For reducing litigation | ||

| 9 | Providing for that in respect of cases covered under deemed closure proceedings under section 28, no fine in lieu of confiscation shall be imposed on the infringing goods [section 125]. | ||

| CUSTOMS TARIFF ACT, 1975

| |||

| A | Amendment in Act, | ||

| 1 | Amendment to the section 9 so as to insert sub-section (1A) to provide for anti-circumvention measure in respect of countervailing duty. | ||

| 2 | Amendment to section 9C of the Customs Tariff Act, 1975 so as to provide appeal provisions against determination of safeguard duties to allow appeal against determination of safeguard duty by designated authority with CESTAT. | ||

| B | Amendment in the First Schedule of the Customs Tariff Act, 1975 | ||

| 1 | First Schedule to the Customs Tariff Act, 1975 is amended to: (i) Create specific tariff lines for specific products, presently classified as “others”; (ii) Rectify the errors to align it with HSN. | ||

| 2 | Amendment in Chapter Notes to Chapter 98, so as to exclude Printed books imported for personal use from the purview of Chapter 98. Printed books imported for personal use will now attract applicable duty. | ||

Securities Contract (Regulation) Act,1956

- Under section 23A – Penalty for failure to furnish information, return, etc.

The penalty under this section can also be levied where the listed entity fails to furnish information, return, etc to the SEBI. Earlier the penalty was levied if the listed entity failed to report to the stock exchange only.

SEBI Act, 1992

. Under section 14 – Fund

- The General Fund constituted under the said section can be utilized for capital expenditure as per annual capital expenditure plan approved by the Board and the Central Government.

- New Insertion – Reserve Fund shall be constituted and 25% of the annual surplus shall be transferred to such Reserve Fund.

- After application towards expenses, the surplus of the General Fund to be transferred to Consolidated Fund of India.

- Under section 15C – Penalty for failure to redress investors’ grievances.

- Penalty shall be levied under the section if the listed entity fails to redress investors’ grievances when called upon to do so either in writing or by means of electronic communication.

iii. Under Section 15F – Penalty for failure in case of stock brokers

- Penalty for non-compliance by stock brokers extended to one crore rupees.

- New Section 15HAA inserted

- Penalty for alteration, destruction, etc., of records and failure to protect the electronic database of Board inserted.

- Penalty shall not be less than one lakh rupees but which may extend to ten crore rupees or three times the amount of profits made out of such act, whichever is higher.

Reserve Bank of India, 1934

It is proposed to insert New sections 45-ID & 45-IE in the act provide power to the Reserve Bank to remove directors of a non-banking financial company other than Government Company from office, and supersession of Board of Directors of a non-banking financial company, on certain grounds.

It is also Insert new section 45MMA in the act So as to provide power to RBI to take action against auditors if Auditor fails to comply any direction give or order made by RBI.

It is also proposed to insert a new section 45MBA in the Act relating to resolution of a non-banking financial Company.

PROHIBITION OF BENAMI PROPERTY TRANSACTIONS ACT, 1988

In section 23 of the Act provides that the Initiating Officer after obtaining prior approval

of the Approving Authority shall have power to conduct any inquiry or investigation in respect of any person, place, property , assets document or other relevant records. (w.r.e.f. 01.11.2016)

Section 24 of the said Act provides that where the Initiating Officer is of the opinion that the person in possession of the property held benami may alienate the property during the period specified in the notice, he may, with the previous approval of the Approving Authority, by order in writing and Initiating officer shall pass order within 90 days from date of issue.

THE BLACK MONEY (UNDISCLOSED FOREIGN INCOME AND ASSETS) AND IMPOSITION OF TAX ACT, 2015

Definition mentioned under section 2 of the assessee (Resident) are in line with the definition mentioned in the section 6 of the Income Tax Act, 1961. It is also proposed to provide that the previous year of acquisition of the undisclosed asset located outside India shall be determined without giving effect to the provisions of section 72(c) of the Act.

2. Economic Survey 2017-18

The Department of Economic Affairs, Finance Ministry of India presents the Economic Survey in the parliament every year, just before the Union Budget. The Economic Survey 2018-19 has been tabled by the Finance Minister, Smt. Nirmala Sitharaman, in the Parliament on 04th July’2019. This survey has been prepared by the Chief Economic Advisor Sh. Krishnamurthy Subramanian. Being the first economic survey of Modi 2.0, it outlines strategic blueprint to achieve Prime Minister’s Vision for $ 5 trillion economy by 2024-25

Fiscal Deficit:

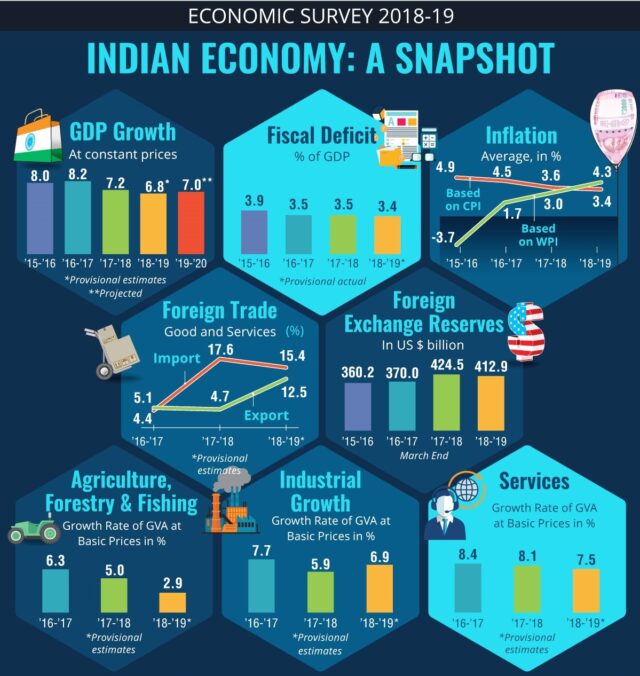

- FY 2018-19 ended with fiscal deficit at 3.4 per cent of GDP and debt to GDP ratio of 44.5 per cent (Provisional).

- The revised fiscal glide path envisages achieving fiscal deficit of 3 per cent of GDP by FY 2020-21 and Central Government debt to 40 per cent of GDP by 2024-25.

- As per cent of GDP, total Central Government expenditure fell by 0.3 percentage points in 2018-19 PA over 2017-18: 4 percentage point reduction in revenue expenditure and 0.1 percentage point increase in capital expenditure.

GDP Growth:

- GDP growth for the Financial Year 2018-19 ended at 6.8%.The year 2019-20 has delivered a huge political mandate for the government, which augurs well for the prospects of high economic growth. Real GDP growth for the year 2019-20 is projected at 7 per cent

- Sustained real GDP growth rate of 8% needed for a $5 trillion economy by 2024-25.

Inflation and monetary policy:

- Retail inflation based on consumer price index – Combined (CPI-C) fell to 3.4 per cent in 2018-19 from 3.6 per cent in 2017-18, 4.5 per cent in 2016-17, 4.9 per cent 2015-16 and 5.9 per cent in 2014-15.

- CPI rural inflation declined during FY 2018-19 over FY 2017-18. However, CPI urban inflation increased marginally during FY 2018-19. Many States witnessed fall in CPI inflation during FY 2018-19. Average retail inflation, measured by Consumer Price Index (CPI), in 2017-18 (April – December) seen at 3.3 per cent.

- WPI inflation stood at 4.3 per cent in 2018-19, higher as compared to 3.0 per cent in 2017-18. The Reserve Bank of India (RBI) has cut the repo rate by 25 basis points to 6.0 per cent in August 2017.

External Sector:

- The current account deficit is projected at 2.4 per cent of GDP in 2018-19, up from 1.8 per cent in 2017-18. this is within reasonable levels.

- The widening of the current account deficit has been driven by a deterioration of trade deficit from 6.0 per cent of GDP to 6.7 per cent across the two years. Rise in crude prices in Q4 of 2018-19 and a decline in the growth of merchandize exports have led to the deterioration of trade deficit.

- India’s balance of payment situation showed some signs of stress during H1 of 2018-19 as sharp rise in crude oil prices caused current account deficit (CAD) to deteriorate. Until end of Q3 for which data is available (April-December 2018-19), India’s CAD stood at US$51.9 billion (2.6 per cent of GDP) as compared to US$35.7 billion (1.8 per cent of GDP) a year ago for the same period. The trade deficit increased to US$145.3 billion during the same period from US$118.4 billion in the corresponding period of previous year.

- The growth in merchandise exports from 5.2 per cent in 2016-17 to 8.8 per cent in 2018-19 mainly resulted from high growth in Petroleum, Oil & Lubricants (POL) exports, which increased from 3.1 per cent in 2016-17 to 24.2 per cent in 2018-19, while non POL exports grew modestly from 5.4 per cent to 7.0 per cent during the same period (Figure 5).

- The growth in merchandise imports from 0.9 per cent in 2016-17 to 10.4 per cent in 2018-19 can also be attributed to a sharp rise in growth rate of POL imports from 8 per cent in 2016-17 to 29.7 per cent in 2018-19. The non-POL imports also increased from -0.2 per cent in 2016-17 to 4.5 per cent in 2018-19 (Figure 6), possibly depicting a downturn in the economy.

- Net Private transfer receipts, mainly representing remittances by Indians employed overseas, increased by 12.4 per cent in 2018-19 (P) as compared to 11.5 per cent in 2017-18.

Direct and Indirect Tax data and the Indian Economy:

- Budget 2018-19 envisaged a growth of 16.7 per cent in gross tax revenue (GTR) over the revised estimates (RE) of 2017-18. GTR was estimated at `22.7 lakh crore for BE 2018-19, which was 12.1 per cent of the GDP. The growth in GTR was estimated to be led by 17.3 per cent growth in indirect taxes and 14.4 per cent growth in direct taxes over the revised estimates of 2017-18. Broadly, 51 per cent of GTR was estimated to accrue from direct taxes and the remaining 49 per cent from indirect taxes.

- As per Provisional Actuals (PA) for 2018-19, fiscal deficit stood at 3.4 per cent of GDP. In 2018-19, direct taxes grew by 13.4 per cent (PA) owing to improved performance of corporate tax. However, indirect taxes fell short of budget estimates by about 16 per cent, following a shortfall in GST revenues (including CGST, IGST and compensation cess) as compared to the budget estimates. GST was implemented in July 2017.

- After the initial transitional issues following the roll-out of GST, revenue collection picked up from annual average of `89.8 thousand crore in 2017-18 to `98.1 thousand crore in 2018-19 (Figure 15). Accordingly, Gross Tax Revenue as a proportion of GDP declined to 10.9 per cent of GDP in 2018-19 (PA), lower by 0.3 percentage points as compared to 2017-18.

- Lower GST rate for Electric cars from 12% to 5%.

- Net employment generation in the formal sector was higher at 8.15 lakh in March, 2019 as against 4.87 lakh in February, 2018 as per EPFO.

Industry:

- In terms of use-based classification of IIP, the index of infrastructure/construction goods remained higher at 7.5 per cent in 2018-19 driven by the robust performance of cement and steel sectors. Large scale public spending has boosted the demand for these sectors. Primary goods and consumer non-durables have registered a positive growth rate of 3.5 per cent and 3.9 per cent in 2018-19 respectively. On the other hand, the capital goods sectors registered a moderate growth of 2.8 per cent in 2018-19 which is indicative of shortfall in investment activities. Overall investment as indicated by the real gross fixed capital formation has increased by 10 per cent in 2018-19. But its share in GDP at current prices is estimated to be only marginally higher at 29.3 per cent during 2018-19. Within consumer goods, consumer durables have shown improved performance with a growth of 5.5 per cent in 2018-19.

- Core Gross Value Added (GVA) (measured as GVA except ‘Agriculture & allied’ activities, and ‘Public administration & defense’) shows higher growth than that of overall GVA in 2018-19. Core GVA growth picked up from 6.5 per cent in 2017- 18 to 7.0 per cent in 2018-19, whereas GVA growth slowed down marginally from 6.9 per cent in 2017-18 to 6.6 per cent.

- Growth of sales (YoY) of over 1700 non-governmental non-financial (NGNF) listed manufacturing companies was 21.6 per cent in Q1, 19.3 per cent in Q2 and 13.2 per cent in Q3 during 2018-19. According to RBI, NGNF listed manufacturing companies posted double digit growth rate in nominal sales in Q4 of 2016-17 and continued its recovery path till Q2 of 2018-19 with minor moderations in between.

- The construction of national highways (NH) proceeded at a rapid pace with more than 20 per cent of the existing highway length of 132,000 km being constructed in the last four years alone. Around 1, 90, 000 km of rural roads constructed under Pradhan Mantri Gram Sadak Yojana (PMGSY) since 2014.

- Service sector growth declined from 8.1 per cent in 2017-18 to 7.5 per cent in 2018-19, due to decline in the growth in ‘Public administration, defense & other services’ and ‘Trade, hotel & transport’ sector. Yet, the sector continues to be the main contributor to growth of the Indian economy. Services share in employment is 34 per cent in 2017.

Accelerated sub-sectors: Financial services, real estate and professional services.

Decelerated sub-sectors: Hotels, transport, communication and broadcasting services.

- 6 million foreign tourists received in 2018-19 compared to 10.4 million in 2017-18.Forex earnings from tourism stood at US$ 27.7 billion in 2018-19 compared to US$ 28.7 billion in 2017-18.

- The market size of medical tourism in India is estimated at `195 billion (US$ 3 billion) in 2017. The value of medical tourism is forecasted to reach US$ 9 billion by 2020. India currently has around 18 per cent of the global medical tourism market.

Ease of Doing Business in India:

- Consistent trade facilitation efforts have resulted in substantive improvement of India’s performance in Trading Across Borders indicator from 146 in 2017 to 80 in the year 2018. Further, these initiatives have also contributed to overall improvement in ‘Ease of Doing Business’ environment in the country, as also recognized by the World Bank.

- Insolvency and Bankruptcy Code led to recovery and resolution of significant amount of distressed assets and improved business culture. Till March 31, 2019, the CIRP yielded a resolution of 94 cases involving claims worthINR1, 73,359 crore. As on 28 Feb 2019, 6079 cases involving INR84 lakh crores have been withdrawn. As per RBI reports, INR50,000 crore received by banks from previously non-performing accounts. Additional INR50,000 crore “upgraded” from non-standard to standard assets.

Prepared by

KNM MANAGEMENT ADVISORY SERVICES PVT. LTD.

E-mail: services@knmindia.com

Web site: www.knmindia.com

Prepared by

3. ANNEXURE – I to Budget Highlights 2019-20

PROPOSED CHANGES IN CUSTOMS DUTY RATES

| Chapter/ heading/ sub-heading/ Tariff item | Commodity | Rate of Duty | ||

| From | To | |||

| Incentivizing domestic value addition, ‘Make in India’ | ||||

| A. | Reduction in Customs duty on inputs and raw materials to reduce costs | |||

| Chemicals | ||||

| 1 | 2710 | Naphtha | 5% | 4% |

| 2 | 2910 20 00 | Methyloxirane (Propylene Oxide) | 7.5% | 5% |

| 3 | 2903 15 00 | Ethylene dichloride (EDC) | 2% | Nil |

| 4 | 28, 70 | Raw materials used in manufacture of Preform of Silica: – a) Silicon Tetra Chloride b) Germanium Tetra Chloride c) Refrigerated Helium Liquid d) Silica Rods e) Silica Tubes | Applicable Rate | Nil |

| Textile

| ||||

| 5

| 5101, 5105

| Wool fibre, Wool Tops | 5% | 2.5% |

| Steel and other base metals | ||||

| 6 | 7225, 7225 19 90 | Inputs for the manufacture of CRGO steel: – a) MgO coated cold rolled steel coils b) Hot rolled coils c) Cold-rolled MgO coated and annealed steel d) Hot rolled annealed and pickled coils e) Cold rolled full hard | 5% | 2.5% |

| 7 | 7226 99 | Amorphous alloy ribbon | 10% | 5% |

| 8 | 8105 20 10 | Cobalt mattes and other intermediate products of cobalt metallurgy | 5% | 2.5% |

| D | Capital Goods | |||

| 9 | 82, 84, 85 or 90 | Capital goods used for manufacturing of following electronic items, namely- (i) Populated PCBA (ii) Camera module of cellular mobile phones (iii) Charger/Adapter of cellular mobile phone (iv) Lithium Ion Cell (v) Display Module (vi) Set Top Box (vii) Compact Camera Module | Applicable rate | Nil |

| B | Changes in Customs duty to provide level playing field to domestic industry | |||

| Food Processing | ||||

| 10 | 0801 32 10 | Cashew kernels, broken | Rs. 60 per kg or 45% whichever is higher | 70% |

| 11 | 0801 32 20, 0801 32 90 | Cashew kernels | Rs. 75 per kg or 45% whichever is higher | 70% |

| Chemicals, Plastics and Rubber | ||||

| 12 | 15, 2915 70, 3823 11 00, 3823 12 00, 3823 13 00, 3823 19 00 | Palm stearin and other oils having 20% or more free fatty acid, Palm fatty acid distillate and other industrial monocarboxylic fatty acids. acid oils from refining for use in manufacture of oleochemicals and soap | Nil | 7.5% |

| 13 | 3904 | Poly Vinyl Chloride | 7.5% | 10% |

| 14 | 3918 | Floor cover of plastics, Wall or ceiling coverings of plastics | 10% | 15% |

| 17 | 3926 90 91, 3926 90 99 | Articles of plastic | 10% | 15% |

| 4002 31 00 | Butyl Rubber | 5% | 10% | |

| 18 | 4002 39 00 | Chlorobutyl rubber or bromobutyl rubber | 5% | 10% |

| Paper Industry | ||||

| 19 | 48 | a. Newsprint b. Uncoated paper used for printing of newspapers c. Lightweight coated paper used for magazines | Nil | 10% |

| 20 | 4901 1010, 4901 91 00, 4901 99 00 | Printed books (including covers for printed books) and printed manuals | Nil | 5% |

| Textile | ||||

| 21 | 5603 94 00 | Water blocking tapes for manufacture of optical fiber cables | Nil | 20% |

| 22 | Ceramic products | |||

| 23 | 6905, 6907 | Ceramic roofing tiles and ceramic flags and pavings, hearth or wall tiles etc. | 10% | 15% |

| Steel and base metal products | ||||

| 24 | 7218 | Stainless steel products | 5% | 7.5% |

| 25 | 7224 | Other alloy steel | 5% | 7.5% |

| 26 | 7229 | Wire of other alloy steel (other than INVAR) | 5% | 7.5% |

| 27 | 8302 | Base metal fittings, mountings and similar articles suitable for furniture, doors, staircases, windows, blinds, hinge for auto mobiles | 10% | 15% |

| 28 | Electronic goods and machine | |||

| 29 | 8415 90 00 | Indoor and outdoor unit of split system air conditioner | 5% | 7.5% |

| 30 | 8474 20 10 | Stone crushing (cone type) plants for the construction of roads | 5% | 7.5% |

| 31 | 8504 40 | Charger/ power adapter of CCTV camera/ IP camera and DVR / NVR | 5% | 7.5% |

| 8518 21 00, 8518 22 00 | Loudspeaker | |||

| 32 | 8521 90 90 | Digital Video Recorder (DVR) and Network Video Recorder (NVR) | 10% | 20% |

| 33 | 8525 80 | CCTV camera and IP camera | 10% | 20% |

| 34 | 9001 10 00 | Optical Fibres, optical fibre bundles and cables | 10% | 20% |

| 35 | Automobile and automobile parts | 10% | 20% | |

| 6813 | Friction material and articles thereof etc. | 10% | 15% | |

| 36 | 7009 | Glass mirrors, whether or not framed, including rear-view mirrors | 10% | 15% |

| 37 | 8301 20 00 | Locks of a kind used in motor vehicles | 10% | 15% |

| 38 | 8421 39 20 8421 39 90 | Catalytic Converter | 5% | 10% |

| 8421 23 00 | Oil or petrol filters for internal combustion engines | 7.5% | 10% | |

| 39 | 8421 31 00 | Intake air filters for internal combustion engines | 7.5% | 10% |

| 40 | 8512 10 00, 8512 20 10, 8512 20 20 | Lighting or visual signaling equipment of a kind used in bicycles or motor vehicles | 10 % | 15% |

| 41 | 8512 30 10 | Vehicle Horns | 10% | 15% |

| 42 | 8512 20 90, 8512 30 90, | Other visual or sound signalling equipment for bicycle and motor vehicle | 7.5% | 15% |

| 43 | 8512 90 00 | Parts of visual or sound signaling equipment, windscreen wipers, defrosters and demisters of a kind used in cycles or motor vehicles | 7.5% | 10% |

| 44 | 8512 40 00, 8539 10 00, 8539 21 20, 8539 29 40 | Windscreen wipers, defrosters and demisters, Sealed beam lamp units, Other lamps for automobiles. | 10% | 15% |

| 8702, 8704 | Completely Built Unit (CBU) of vehicles | 25% | 30% | |

| 45 | 8706 | Chassis fitted with engines, for the motor vehicles of headings 8701 to 8705 | 10% | 15% |

| 46 | 8707 | Bodies (including cabs), for the motor vehicles of headings 8701 to 8705 | 10% | 15% |

| C | Reducing customs duty to promote electrical mobility | |||

| 47 | Any Chapter | Parts for exclusive use Electric vehicles – a. E-drive assembly b. On board charger c. E compressor d. Charging Gun | Applicable rate | Nil |

| D | Changes in Customs duty to address the problem of duty inversion in certain sectors | |||

| 48 | 2515 12 20, 6802 10 00, 6802 21 10, 6802 21 20, 6802 21 90, 6802 91 00, 6802 92 00 | Marble Slabs | 20% | 40% |

| 49 | Any Chapter | Raw material, parts or accessories for use manufacture of artificial kidneys, disposable sterilized dialyzer and micro-barrier of artificial kidney | Applicable rate | Nil |

| II | Reduction in customs duty to promote renewable energy | |||

| 50 | 2612 10 00 | All forms of Uranium ores and concentrates, for generation of nuclear power | 2.5% | Nil |

| 51 | 2844 20 00 | Uranium enriched in U-235 or its compounds, plutonium and its compounds, mixtures etc. for generation of nuclear power | 7.5% | Nil |

| 52 | 9801 | All goods required for setting up of Nuclear power plant under project imports: – a) MahiBanswara Atomic Power project- 1 to 4, b) Kaiga Atomic Power project – 5 & 6, c) Gorakhpur Atomic Power project- 3 & 4, d) Chutka Atomic Power project- 1 & 2) | Applicable rate | Nil |

| III | Duty rationalization/ withdrawal | |||

| 53 | 2709 20 00 | Petroleum crude | Nil | Re. 1 per tonne |

| 54 | 84, 85 or 90 | Specified electronic goods such as switches, sockets, plugs, connectors, relays etc. | Nil | Applicable rate |

| 55 | 84, 85 or 90 | Capital goods used for manufacturing of specified electronic items, namely- (i) Cathode Ray tubes; (ii) CD/CD-R/DVD/DVD-R; (iii) Deflection components, CRT monitors/CTVs; (iv) Plasma Display Panel | Nil | Applicable rate |

| IV | Export Promotion for sports goods | |||

| 56 | 39, 44 | Foam/ EVA foam and pine wood are being included in the list of item allowed duty free import upto 3% of FOB value of sports goods exported in the preceding financial year | Applicable rate | Nil |

| V | Reduction in customs duty for Defence sector | |||

| 57 | Any Chapter | Specified Military equipment and their parts imported by Ministry of Defence or Armed forces | Applicable rate | Nil |

| VI | Additional revenue measures | |||

| 58 | 7106 | Silver (including silver plated with gold or platinum) unwrought or in semi-manufactured forms, or in powder form | 10% | 12.50% |

| 59 | 7106 | Silver dore bar, having silver content not exceeding 95% | 8.50% | 11% |

| 60 | 7107 00 00 | Base metals clad with silver, not further worked than semi-manufactured | 10% | 12.50% |

| 61 | 7108 | Gold (including gold plated with platinum) unwrought or in semi-manufactured forms, or in powder form | 10% | 12.50% |

| 62 | 7108 | Gold dore bar, having gold content not exceeding 95% | 9.35% | 11.85% |

| 63 | 7109 00 00 | Base metals or silver, clad with gold, not further worked than semi-manufactured | 10% | 12.50% |

| 64 | 7110 | Platinum, unwrought or in semi-manufactured forms, or in powder form [ other than Rhodium] | 10% | 12.50% |

| 65 | 7111 00 00 | Base metals, silver or gold, clad with platinum, not further worked than semi-manufactured | 10% | 12.50% |

| 66 | 7112 | Waste and scrap of precious metals or of metal clad with precious metals; other waste and scrap containing precious metal compounds, of a kind used principally for the recovery of precious metal. | 10% | 12.50% |

| 67 | 71 or 98 | Gold and Silver imported by an eligible passenger as baggage | 10% | 12.50% |

| Road and infrastructure cess (customs) | ||||

| 68 | 2710 | Motor spirit commonly known as petrol, High speed diesel oil | Rs 8 per litre | Rs 9 per litre |

- PROPOSALS INVOLVING CHANGE IN EXCISE DUTY RATES:

| Tariff Item | Commodity | Rate of Duty | ||||||

| From | To | |||||||

| A | Basic Excise Duty | |||||||

| 1 | 2402 20 10 | Other than filter cigarettes, of length not exceeding 65 millimetres | Nil | Rs. 5 per thousand | ||||

| 2 | 2402 20 20 | Other than filter cigarettes, of length exceeding 65 millimetres but not exceeding 70 millimetres | Nil | Rs. 5 per thousand | ||||

| 3 | 2402 20 30 | Filter cigarettes of length (including the length of the filter, the length of filter being 11 millimetres or its actual length, whichever is more) not exceeding 65 millimetres | Nil | Rs. 5 per thousand | ||||

| 4 | 2402 20 40 | Filter cigarettes of length (including the length of the filter, the length of filter being 11 millimetres or its actual length, whichever is more) exceeding 65 millimetres but not exceeding 70 millimetres | Nil | Rs. 5 per thousand | ||||

| 5 | 2402 20 50 | Filter cigarettes of length (including the length of the filter, the length of filter being 11 millimetres or its actual length, whichever is more) exceeding 70 millimetres but not exceeding 75 millimetres | Nil | Rs. 5 per thousand | ||||

| 6 | 2402 20 90 | Other Cigarettes | Nil | Rs. 10 per thousand | ||||

| 7 | 2402 90 10 | Cigarettes of tobacco substitutes | Nil | Rs. 5 per thousand | ||||

| 8 | 2403 11 10 | Hookah or gudaku tobacco | Nil | 0.5% | ||||

| 9 | 2403 19 10 | Smoking mixtures for pipes and cigarettes | Nil | 1% | ||||

| 10 | 2403 19 21 | Other than paper rolled biris, manufactured without the aid of machine | Nil | 5 paisa per thousand | ||||

| 11 | 2403 19 29 | Other (biris) | Nil | 10 paisa per thousand | ||||

| 12 | 2403 19 90 | Other smoking tobacco | Nil | 0.5% | ||||

| 13 | 2403 91 00 | “Homogenised” or “reconstituted” tobacco | Nil | 0.5% | ||||

| 14 | 2403 99 10 | Chewing tobacco | Nil | 0.5% | ||||

| 15 | 2403 99 20 | Preparations containing chewing tobacco | Nil | 0.5% | ||||

| 16 | 2403 99 30 | Jarda scented tobacco | Nil | 0.5% | ||||

| 17 | 2403 99 40 | Snuff | Nil | 0.5% | ||||

| 18 | 2403 99 50 | Preparations containing snuff | Nil | 0.5% | ||||

| 19 | 2403 99 60 | Tobacco extracts and essence | Nil | 0.5% | ||||

| 20 | 2403 99 90 | Other (manufactured tobacco and substitutes) | Nil | 0.5% | ||||

| 21 | 2709 20 00 | Petroleum crude | Nil | Re.1 per tonne | ||||

| Special additional excise duty | ||||||||

| 22 | 2710 | Motor spirit commonly known as petrol | Rs 7 per litre | Rs 8 per litre | ||||

| 23 | 2710 | High speed diesel oil | Re 1 per litre | Rs 2 per litre | ||||

| Road and infrastructure cess | ||||||||

| 24 | 2710 | Motor spirit commonly known as petrol, High speed diesel oil | Rs 8 per litre | Rs 9 per litre | ||||

Disclaimer: Information in this note is intended to provide only a general update of the subjects covered. It is not intended to be a substitute for detailed research or the exercise of professional judgment. KNM accepts no responsibility for loss arising from any action taken or not taken by anyone using this publication