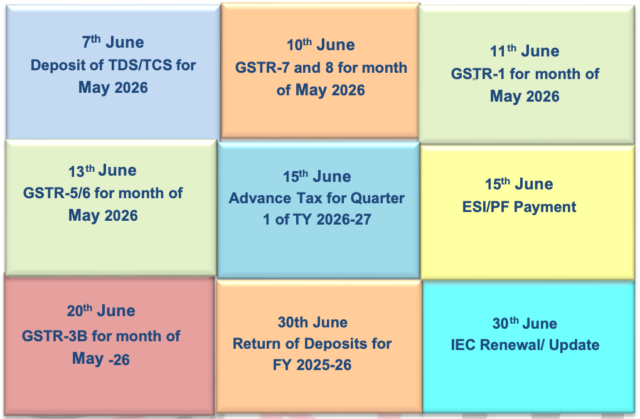

Executive Summary

Income Tax

- ITR Filing Utilities are available on Income Tax Portal for AY 2026-27.

- Offline utility for Forms 145 & 146 has been enabled on Income Tax Portal.

- Challan forms for Tax Year 2026-27 are live on Income Tax Portal.

Goods And Service Tax (GST)

- Instruction F.No.GSTAT/Pr.bench/Portal/125/25-26, Section 112 Central Goods and Services Tax Act, 2017 – Appellate Tribunal – Appeals to – Instructions to be followed by Security Officer, Dated 14.05.2026

- Corrigendum to Notification No. 02/2026 – Central Tax Correction of HSN Tariff Classification for Specified Beverage Products under IGST Rate Notifications (HSN Code amended from 2202 99 90 to 2202 91 00), Dated 08.05.2026

- GSTAT Administrative Circular – Office Order No. 3/GSTAT/PB/2026 Classification and Allocation of Appeals, Dated 14.05.2026

- GSTN Advisory No. 661 – Enhancements in the E-Way Bill (EWB) Portal, Dated on 21.05.2026

Companies Act 2013/ Other Laws

- Corporate Social Responsibility implementation through Zero Coupon Zero Principal instrument

- Ease of investing – modified nomination norms for Demat Accounts & Mutual Fund folios

- Master circular on surveillance of Securities Market

- RBI introduces cooling-off period to strengthen governance in rural Co-Operative Banks

- Key provisions of the Insolvency and Bankruptcy Code (Amendment) Act, 2026 brought into force.

- IBBI simplifies valuation requirements for MSMEs under CIRP

- IBBI rationalises valuation framework under Pre-Packaged Insolvency Process.

- IBBI strengthens governance framework for Insolvency Professional Agencies

- Final Rules Notified Under Four Labour Codes

![]()

![]()

A. ITR FILING UTILITIES FOR AY 2026-27 [29-05-2026]

- The Income Tax Department officially enabled online filing and Excel utilities for ITR-1 and ITR-4 on the e-Filing Portal on May 15, 2026, with offline utilities following on May 20, 2026.

- Online filing and Excel utility for ITR-2 were enabled on May 26, 2026, and the offline utility was made available on May 29, 2026.

B. OFFLINE UTILITY FOR FORM 145 & 146 HAS BEEN ENABLED [29-05-2026]

- Offline Utility for Form 145 and Form 146 has been enabled on the e-Filing Portal. Users can download, fill, and submit the forms directly through the utility available under “Downloads —> Income tax Forms —–> Income Tax Act 2025”.

C. CHALLAN FORMS FOR TAX YEAR 2026-27 [30-05-2026]

- New challan forms are live on e-Filing portal for tax payments under the Income Tax Act, 2025. Users are advised to make payments using the new challans only for Tax Year 2026-27. Please refer latest updates for more details.

![]()

![]()

A. Instruction F.No.GSTAT/Pr.bench/Portal/125/25-26, Section 112 Central Goods and Services Tax Act, 2017 – Appellate Tribunal – Appeals to – Instructions to be followed by Security Officer, Dated 14.05.2026

Security Protocols for GST Appellate Tribunal Premises

GSTAT issued instructions prescribing duties and responsibilities of Security Officers at GSTAT premises to ensure secure handling of appeal records, visitor management, access control, and smooth functioning of Tribunal proceedings.

- Applicable to GSTAT Principal Bench and State Benches.

- Prescribes entry, access control, and visitor verification procedures

- Ensures protection of appeal records and confidential documents.

- Provides guidelines for the movement of litigants, advocates, and departmental officers.

- Strengthens administrative and operational security at GSTAT premises.

Impact:

Businesses involved in GST litigation will benefit from improved security and organized tribunal operations, leading to smoother hearings, better protection of confidential business information, and reduced chances of procedural disruptions during appeal proceedings.

B. Corrigendum to Notification No. 02/2026 – Central Tax Correction of HSN Tariff Classification for Specified Beverage Products under IGST Rate Notifications (HSN Code amended from 2202 99 90 to 2202 91 00), Dated 08.05.2026

Correction in Notification Empowering GSTAT Principal Bench as National Appellate Authority for Advance Ruling (NAAAR)

CBIC issued a corrigendum correcting the notification number appearing in Notification No. 02/2026 – Central Tax relating to the designation of the GSTAT Principal Bench as the National Appellate Authority for Advance Ruling.

- Corrected clerical error in the original notification

- Clarified reference to Notification No. 02/2026 – Central Tax.

- No change in legal provisions or effective date.

- Continue authorization of GSTAT Principal Bench to hear appeals against conflicting Advance Rulings.

Impact:

Businesses operating in multiple States now have greater certainty regarding the appellate mechanism for conflicting Advance Rulings. This helps in achieving uniform GST treatment across locations, reducing tax disputes and improving business planning.

C. GSTAT Administrative Circular – Office Order No. 3/GSTAT/PB/2026 Classification and Allocation of Appeals, Dated 14.05.2026

Framework for Classification and Allocation of GST Appeals Across GSTAT Benches

GSTAT issued administrative instructions for systematic classification, allocation, and hearing of GST appeals before various Tribunal Benches.

- Appeals classified into categories such as ITC, classification, valuation, refund, registration, and penalty matters.

- All appeals to be initially placed before a Division Bench

- Standardized allocation of cases across GSTAT Benches.

- Jurisdiction and case management procedures streamlined.

- Hybrid, virtual, and physical hearing facilities are enabled.

Impact:

Businesses can expect faster disposal of GST disputes, improved transparency in appeal allocation, reduced litigation timelines, and lower legal and travel costs through virtual hearing facilities. Quicker resolution of disputes helps reduce blockage of working capital and business uncertainty.

D. GSTN Advisory No. 661 – Enhancements in the E-Way Bill (EWB) Portal, dated 21.05.2026

Enhancements in E-Way Bill Portal Functionality

GSTN introduced new functionalities and validation controls in the E-Way Bill Portal to improve compliance monitoring and ease of use.

- Mandatory reporting of “Ship-To GSTIN” in applicable Bill-To/Ship-To transactions.

- Voluntary E-Way Bill Closure facility introduced.

- API specifications updated for ERP/GSP/ASP integration.

- Enhanced validation checks to reduce data-entry errors.

- Rollout planned up to 15.06.2026.

Impact:

Businesses involved in the movement of goods will experience better tracking and documentation accuracy, reducing the risk of E-Way Bill mismatches, detention of goods, penalties, and compliance notices. The voluntary closure facility also helps maintain accurate records of completed consignments and strengthens GST compliance.

![]()

![]()

A. CORPORATE SOCIAL RESPONSIBILITY IMPLEMENTATION THROUGH ZERO COUPON ZERO PRINCIPAL INSTRUMENT:

The Ministry of Corporate Affairs has notified the Companies (Corporate Social Responsibility Policy) Amendment Rules, 2026, effective from 27 May 2026. The amendment introduces the concepts of “Not for Profit Organization” and “Zero Coupon Zero Principal (ZCZP) Instrument” into the CSR framework, enabling companies to undertake CSR activities through investments in ZCZP instruments issued by eligible NPOs listed on the Social Stock Exchange. Companies may allocate up to 10% of their annual CSR expenditure through such instruments and will be exempt from conducting impact assessments for projects funded through them. The rules also prescribe conditions for NPOs regarding project duration, utilization of funds, and transfer of unspent amounts to Schedule VII funds upon termination of listing, thereby strengthening transparency and accountability in CSR implementation.

![]()

![]()

B. EASE OF INVESTING – MODIFIED NOMINATION NORMS FOR DEMAT ACCOUNTS & MUTUAL FUND FOLIOS

The Securities and Exchange Board of India (SEBI) has issued this circular addressed to Asset Management Companies (AMCs) of Mutual Funds, their Registrars and Transfer Agents (RTAs), Recognized Depositories, and Depository Participants regarding modifications in nomination norms for demat accounts and mutual fund folios. This follows SEBI’s earlier circular dated January 10, 2025, which introduced revised nomination facilities effective from March 01, 2025, aimed at simplifying investor onboarding and reducing unclaimed financial assets. However, based on stakeholder representations highlighting certain operational difficulties in implementation, SEBI has reviewed the framework and, after public consultation feedback, has decided to further ease and refine the nomination process to improve investor convenience and streamline compliance across the securities market ecosystem.

C. MASTER CIRCULAR ON SURVEILLANCE OF SECURITIES MARKET

The Securities and Exchange Board of India (SEBI) has issued an updated Master Circular consolidating all directions relating to surveillance of the securities market for better accessibility and regulatory clarity for all stakeholders, including stock exchanges, depositories, listed companies, intermediaries, and fiduciaries under the SEBI (Prohibition of Insider Trading) Regulations, 2015. This updated circular incorporates key provisions from earlier circulars relating to financial disincentives for surveillance lapses at market infrastructure institutions, permissions regarding subscription to non-convertible securities during trading window closures, and extensions of automated trading window restrictions to immediate relatives of designated persons during financial result declarations. With this consolidation, all earlier circulars covered under the appendix stand rescinded to the extent of surveillance-related provisions; however, actions already taken, applications pending, and rights or liabilities accrued under the previous circulars shall remain valid and enforceable as if those circulars continue to be in force. This Master Circular has been issued under Section 11(1) of the SEBI Act, 1992 to strengthen investor protection and enhance the regulatory framework governing surveillance in the Indian securities market.

![]()

![]()

A. RBI INTRODUCES COOLING-OFF PERIOD TO STRENGTHEN GOVERNANCE IN RURAL CO-OPERATIVE BANKS

The Reserve Bank of India (RBI) has issued the Rural Co-operative Banks (Governance) Amendment Directions, 2026, effective immediately from May 25, 2026, to curb practices that undermine statutory tenure limits of directors in State and Central Co-operative Banks. The amendment introduces a mandatory three-year cooling-off period after completion of a continuous ten-year tenure on the Board of a Rural Co-operative Bank, before a director can be reappointed in any capacity through election, co-option, or otherwise. During this cooling-off period, the individual may only remain associated with the bank as a member or customer. The clarification also defines how continuous tenure is to be calculated, ensuring stricter compliance with governance norms and reinforcing the intent of existing legal provisions.

![]()

![]()

A. KEY PROVISIONS OF THE INSOLVENCY AND BANKRUPTCY CODE(AMENDMENT) ACT, 2026 BROUGHT INTO FORCE

The Central Government has notified 26 May 2026 as the effective date for the enforcement of several significant provisions of the Insolvency and Bankruptcy Code (Amendment) Act, 2026. Through Notification S.O. 2625(E) dated 22 May 2026, a wide range of amendments, including Sections 2 to 6, 8 to 33, 35 to 39, 41, 43 to 44, 46, 48 to 59, 61 to 66, 68, and specified provisions of Sections 69, 70 and 72, have been brought into operation. The notification marks a major step in implementing the amended insolvency framework, aimed at enhancing the efficiency, transparency, and effectiveness of India’s insolvency resolution process.

B. IBBI SIMPLIFIES VALUATION REQUIREMENTS FOR MSMEs UNDER CIRP

The Insolvency and Bankruptcy Board of India (IBBI), through the Insolvency Resolution Process for Corporate Persons (Second Amendment) Regulations, 2026, has amended Regulation 27 to streamline the valuation process for MSMEs undergoing Corporate Insolvency Resolution Process (CIRP). Effective from 19 May 2026, the amendment provides that, for corporate debtors classified as Micro, Small and Medium Enterprises (MSMEs), the Resolution Professional shall appoint only one set of registered valuers by default. A second set of valuers may be appointed only if the Committee of Creditors records specific reasons in writing. The change is expected to reduce compliance costs and expedite insolvency proceedings for MSMEs.

C. IBBI RATIONALISES VALUATION FRAMEWORK UNDER PRE-PACKAGED INSOLVENCY PROCESS

The Insolvency and Bankruptcy Board of India (IBBI) has notified the Pre-Packaged Insolvency Resolution Process (Second Amendment) Regulations, 2026, introducing significant changes to the valuation framework under pre-pack insolvency proceedings. The amendment substitutes Regulation 38 to provide for the appointment of a single set of registered valuers by default, with the Committee of Creditors retaining the option to appoint two sets of valuers for recorded reasons. It also clarifies eligibility restrictions for valuers and revises Regulation 39 to streamline the methodology for determining fair value and liquidation value where one or two sets of valuers are appointed. These changes are aimed at enhancing efficiency, reducing procedural complexity, and ensuring greater consistency in valuation outcomes during the pre-packaged insolvency resolution process.

D. IBBI STRENGTHENS GOVERNANCE FRAMEWORK FOR INSOLVENCY PROFESSIONAL AGENCIES

The Insolvency and Bankruptcy Board of India (IBBI) has notified the Model Bye-Laws and Governing Board of Insolvency Professional Agencies (Amendment) Regulations, 2026, introducing key changes to enhance governance and oversight of Insolvency Professional Agencies (IPAs). The amendment to Regulation 5 mandates the inclusion of a nominee director appointed by the Board on the governing board of IPAs, along with revised eligibility and composition norms for directors, including clarity on independent director requirements. It also provides that the second term of key officials such as the managing director will be subject to satisfactory performance review and prior approval of the Board. Additionally, Regulation 5A now requires IPAs to submit at least two names to the Board for approval of appointment or renewal of the managing director at least one month before the expiry of the existing tenure, thereby strengthening regulatory oversight and ensuring better governance standards.

![]()

![]()

A. FINAL RULES NOTIFIED UNDER FOUR LABOUR CODES

The Ministry of Labour & Employment notified the final Central Rules under the following Labour Codes on 8 May 2026:

- Code on Wages, 2019

- Industrial Relations Code, 2020

- Code on Social Security, 2020

- Occupational Safety, Health and Working Conditions Code, 2020

With this notification, the Central Government has completed the rule-making process under all four Labour Codes, paving the way for uniform implementation across India, subject to notification of corresponding State Rules wherever applicable.

![]()

![]()

Disclaimer Information in this note is intended to provide only a general update of the subjects covered. It is not intended to be a substitute for detailed research or the exercise of professional judgment. KNM accepts no responsibility for loss arising from any action taken or not taken by anyone using this publication. Updates for the period 31.05.2026