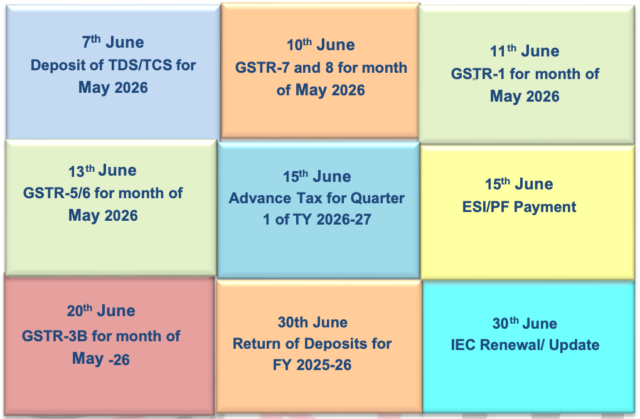

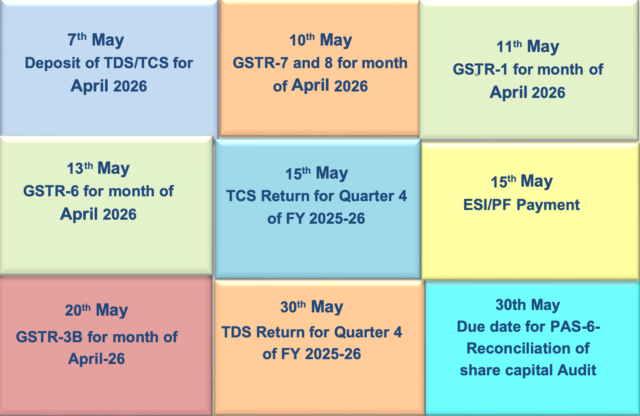

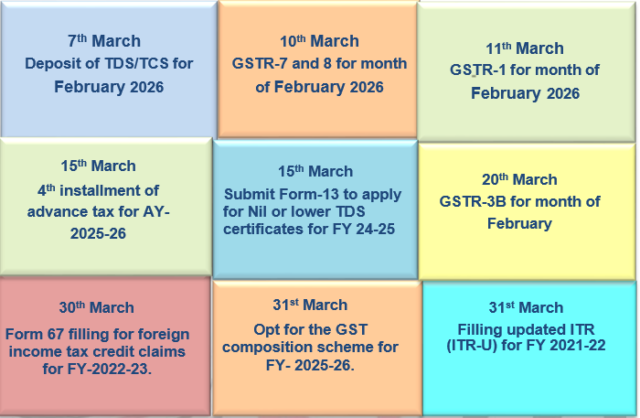

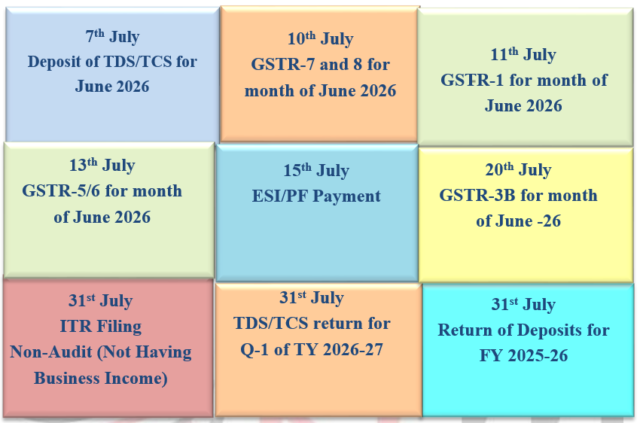

Executive Summary

Income Tax

- Guidelines for compulsory selection of returns for complete scrutiny

Goods And Service Tax (GST)

- GSTN Advisory dated 09.06.2026 – Extension of Timeline for Mandatory ‘Ship-to GSTIN’ and Voluntary Closure of E-Way Bills

- Notification S.O. 4220 (E) dated 17.09.2025 – Section 112 of the Central Goods and Services Tax Act, 2017 – Extension of Time Limit for Filing Appeals before GST Appellate Tribunal (GSTAT)

- Section 11A of the Central Goods and Services Tax Act, 2017 – Waiver of Past GST Dues (Rules under Drafting by CBIC), Dated 25.05.26

- CBIC Advisory dated 11.06.2026 – Introduction of Two-Factor Authentication (2FA) for Central Excise / HSNS Cess / Service Tax & SBS Taxpayers

Companies Act 2013/ Other Laws

- Extension of Due Date for Filing Form DPT-3

- Extension of Name Reservation & Resubmission Period

- Companies (Registered Valuers and Valuation) Amendment Rules, 2026

- SEBI Circular on Strengthening Compliance & Operational Guidelines for Intermediaries

- Reserve Bank of India circular – prudential norms on credit exposure

- IFSCA circular on Annual Compliance Audit reporting for capital market intermediaries

- Reporting of FCNR(B) Deposits & ECB Arrangements

- IBBI circular on revised formats under CIRP Regulations

- IBBI issues Guidelines for conducting Valuation under IBC

- IBBI notifies CIRP (Third Amendment) Regulations, 2026

![]()

![]()

- GUIDELINES FOR COMPULSORY SELECTION OF RETURNS FOR COMPLETE SCRUTINY DURING THE FINANCIAL YEAR 2026-27 [04-06-2025]

The parameters for compulsory selection of returns for complete scrutiny during Financial Year 2026-27 and procedure for compulsory selection in such cases are prescribed as under:

| Scenario Code | Parameters (Cases Covered) | Procedure (Simplified) |

| CS-01 | Survey Cases Cases where survey u/s 133A (excluding section 133A(2A)) was conducted on or after 01.04.2024. | • Selected by Directorate of Income-tax (Systems) based on information from Investigation Wing. • Notice u/s 143(2) issued by the prescribed authority/AO. • If outside Central Charge, transfer within 15 days of notice. |

| CS-02 | Search/Requisition Cases Cases where search u/s 132 or requisition u/s 132A was initiated on or after 01.04.2024. For searches/requisitions on or after 01.09.2024, only the assessment year covered under section 158BA(6) shall be selected. | • Selected by the Jurisdictional AO with prior approval of Pr. CIT/Pr. DIT/CIT/DIT. • If outside Central Charge, transfer within 15 days of notice u/s 143(2). |

| CS-03 | Reassessment Cases (i) Search initiated between 01.04.2021 and 31.08.2024, or survey conducted on or after 01.04.2021. (ii) Other cases where notice u/s 148 has been issued and assessment is to be completed by 31.03.2027. | • AO issues notice u/s 143(2) where return is filed. • AO uploads documents forming the basis of notice u/s 148. • Cases are forwarded to NaFAC for further assessment (except Central/International Taxation cases). |

| CS-04 | Registration/Approval Cases Registration/approval under sections 12A, 12AB, 35, 10(23C), etc. has been rejected, cancelled or withdrawn on or before 31.03.2025, but exemption/deduction is still claimed in ITR-7 not applicable if cancellation has been reversed in appeal. | • Selected by Directorate of Income-tax (Systems). • Notice u/s 143(2) issued through NaFAC or prescribed authority. • AO uploads relevant supporting documents. |

| CS-05 | Recurring Addition Cases Addition on the same issue (including Transfer Pricing) in an earlier year exceeds: • ₹50 lakh (Ahmedabad, Bengaluru, Chennai, Delhi, Hyderabad, Kolkata, Mumbai & Pune), or• ₹20 lakh (other charges).Applicable where the addition has become final or has been upheld in favour of Revenue. | • AO prepares list and obtains approval of Pr. CIT/Pr. DIT/CIT/DIT. • Consolidated list forwarded by Pr. CCIT to Directorate of Systems by 15.06.2026. • Notice u/s 143(2) issued through NaFAC. |

| CS-06 | Specific Tax Evasion Information Specific information regarding tax evasion received from Investigation Wing, Intelligence, Regulatory or other law enforcement agencies, and return has been filed. | • AO prepares list following the same procedure as CS-05. • Cases selected after approval and notice issued through NaFAC. • Cases selected only on specific tax-evasion information. Mere information from AIS, SFT, NMS, CPC-TDS, or I&CI is not sufficient. |

![]()

![]()

- GSTN ADVISORY DATED 09.06.2026 – EXTENSION OF TIMELINE FOR MANDATORY ‘SHIP-TO GSTIN’ AND VOLUNTARY CLOSURE OF E-WAY BILLS

GSTN has extended the implementation date for mandatory capture of ‘Ship-to GSTIN’ in Bill-to/Ship-to transactions and the Voluntary Closure of E-Way Bills from 15 June 2026 to 1 August 2026.

Key Highlights:

- Mandatory capture of ‘Ship-to GSTIN’ deferred to 1 August 2026.

- Facility for Voluntary Closure of E-Way Bills is also effective from 1 August 2026.

- Applicable to taxpayers generating E-Way Bills through the portal and APIs.

- Provides additional time for ERP and API integration updates.

- Businesses should validate customer master data before implementation.

Impact:

Businesses should use the extended timeline to update their ERP systems, API integrations and internal processes to ensure seamless E-Way Bill generation and avoid compliance issues from 1 August 2026.

- NOTIFICATION S.O. 4220 (E) DATED 17.09.2025 – SECTION 112 OF THE CENTRAL GOODS AND SERVICES TAX ACT, 2017 – EXTENSION OF TIME LIMIT FOR FILING APPEALS BEFORE GST APPELLATE TRIBUNAL (GSTAT)

The Government has prescribed a special time limit up to 30 June 2026 for filing appeals before the GST Appellate Tribunal (GSTAT) in cases where the Order-in-Appeal was communicated before 1 April 2026. For orders communicated on or after 1 April 2026, the normal limitation period under Section 112 shall apply.

Key Highlights:

- Applicable to appeals against Orders-in-Appeal communicated before 1 April 2026.

- Last date for filing such pending appeals before GSTAT is 30 June 2026.

- Normal limitation period of 3 months continues for orders communicated on or after 1 April 2026.

- Ensures taxpayers receive an opportunity to file appeals due to the delayed operationalization of GSTAT.

- Applicable across all GSTAT Principal and State Benches.

Impact:

Businesses having pending GST appellate matters should review all Orders-in-Appeal received before 1 April 2026 and ensure appeals are filed on or before 30 June 2026. Failure to file within the prescribed timeline may result in the loss of the statutory right to appeal.

- SECTION 11A OF THE CENTRAL GOODS AND SERVICES TAX ACT, 2017 – WAIVER OF PAST GST DUES (RULES UNDER DRAFTING BY CBIC), DATED 25.05.26

CBIC is drafting the rules to operationalize Section 11A of the CGST Act, 2017, which empowers the Government, on the recommendation of the GST Council, to waive GST dues that arise due to a generally prevalent trade practice followed by an industry. The provision was inserted through the Finance (No. 2) Act, 2024 and is yet to be implemented through detailed rules and notifications.

Key Highlights:

- Enables waiver of past GST dues for notified industries.

- Applicable where non-payment or short payment occurred due to a generally prevalent trade practice.

- Relief can be granted only on the recommendation of the GST Council.

- Detailed rules and implementation framework are under preparation by CBIC.

- No notification or circular has been issued yet for operationalizing the provision.

Impact:

Once notified, eligible businesses may receive relief from historical GST demands arising from industry-wide trade practices, reducing litigation and providing greater certainty in tax compliance.

- CBIC ADVISORY DATED 11.06.2026 – INTRODUCTION OF TWO-FACTOR AUTHENTICATION (2FA) FOR CENTRAL EXCISE / HSNS CESS / SERVICE TAX & SBS TAXPAYERS

CBIC has introduced Two-Factor Authentication (2FA) for users logging into the ACES/CBIC portal for Central Excise, HSNS Cess, Service Tax and SBS taxpayers to enhance portal security.

Key Highlights:

- 2FA made mandatory at the time of user login.

- Applicable to Central Excise, HSNS Cess, Service Tax and SBS taxpayers.

- Login requires OTP verification in addition to user credentials.

- Enhances security against unauthorized access.

- Registered mobile numbers and email should be updated for smooth authentication.

Impact:

Businesses should ensure that authorised users’ contact details are updated on the portal to avoid login disruptions. The new authentication mechanism enhances data security and safeguards sensitive tax information.

![]()

![]()

- EXTENSION OF DUE DATE FOR FILING FORM DPT-3:

The Ministry of Corporate Affairs has via General Circular No. 02/2026 dated 20 June 2026 extended the due date for filing Form DPT-3 (Return of Deposits) for FY 2025–26 till 31 July 2026. The extension provides relief to companies facing compliance challenges and ensures adequate time for accurate filing without additional penalties.

- EXTENSION OF NAME RESERVATION & RESUBMISSION PERIOD

In view of technical issues (including data centre disruptions), MCA has extended the validity of reserved company names and resubmission timelines up to 10 July 2026. This ensures that stakeholders are not adversely impacted due to system-related delays.

- COMPANIES (REGISTERED VALUERS AND VALUATION) AMENDMENT RULES, 2026

The Ministry of Corporate Affairs (MCA) amended the Companies (Registered Valuers and Valuation) Rules, 2017 by introducing a minimum paid-up share capital requirement of ₹25 lakh for Registered Valuers Organisations (RVOs). Existing RVOs that do not meet this requirement have been granted a transition period up to 31 March 2028 to comply. This move aims to strengthen the financial credibility and operational capacity of valuation entities.

![]()

![]()

- SEBI CIRCULAR ON STRENGTHENING COMPLIANCE & OPERATIONAL GUIDELINES FOR INTERMEDIARIES

The Securities and Exchange Board of India (SEBI) has issued Circular No. HO/38/12/11(5)2026-MIRSD-POD/I/14660/2026 under the MIRSD (Market Intermediaries Regulation and Supervision Department), with the objective of streamlining regulatory requirements and enhancing compliance standards for intermediaries operating in the securities market. The circular forms part of SEBI’s broader initiative to consolidate and rationalize operational guidelines, ensuring greater transparency, investor protection, and uniformity in regulatory practices. It emphasizes adherence to updated procedures, improved reporting mechanisms, and alignment with existing master circulars issued in 2026 for market intermediaries such as research analysts, investment advisers, and other registered entities.

![]()

![]()

A. RESERVE BANK OF INDIA CIRCULAR – PRUDENTIAL NORMS ON CREDIT EXPOSURE

The Reserve Bank of India issued this circular to further strengthen prudential norms relating to credit exposure and risk management for banks and financial institutions. The circular primarily focuses on refining existing regulatory frameworks to ensure better monitoring of borrower exposure, improved credit discipline, and enhanced transparency in lending practices. It reinforces the importance of adherence to prescribed exposure limits and prudent credit appraisal mechanisms in order to mitigate systemic risks in the banking sector.

B. IFSCA CIRCULAR ON ANNUAL COMPLIANCE AUDIT REPORTING FOR CAPITAL MARKET INTERMEDIARIES

The International Financial Services Centres Authority (IFSCA) has issued a circular prescribing a standardized reporting format and compliance norms for the Annual Compliance Audit of Capital Market Intermediaries (CMIs) operating in IFSCs. As per the circular, all CMIs are required to submit an Annual Compliance Audit Report (ACAR) along with a detailed Annual Compliance Audit Checklist (ACAC) in the specified format to IFSCA by 30th September every year for the preceding financial year. Additionally, certain intermediaries such as broker dealers, clearing members, and depository participants are also required to submit these reports to their respective Market Infrastructure Institutions. This circular aims to enhance regulatory oversight, ensure uniform compliance standards, and strengthen governance practices across capital market intermediaries in IFSCs.

C. REPORTING OF FCNR(B) DEPOSITS & ECB ARRANGEMENTS

The Reserve Bank of India (RBI) vide A.P. (DIR Series) Circular No. 15 dated June 2026 introduced updated reporting requirements relating to Foreign Currency Non-Resident (Bank) [FCNR(B)] deposits and External Commercial Borrowings (ECB). The circular mandates Authorised Dealer (AD) Category-I banks to ensure timely and accurate submission of prescribed returns under FEMA. It further clarifies that data from 8 June 2026 onwards must be incorporated in the first reporting cycle due on 22 June 2026, thereby strengthening monitoring of foreign currency liabilities and borrowings. These directions have been issued under the provisions of the Foreign Exchange Management Act, 1999, with the objective of improving transparency and regulatory oversight in cross-border transactions.

![]()

![]()

- IBBI CIRCULAR ON REVISED FORMATS UNDER CIRP REGULATIONS

The Insolvency and Bankruptcy Board of India (IBBI) has issued Circular No. IBBI/CIRP/94/2026 prescribing revised and standardized formats under the Insolvency Resolution Process for Corporate Persons (CIRP) Regulations, 2016, pursuant to the Third Amendment Regulations, 2026. The circular notifies updated forms for various stages of the CIRP, including public announcement (Form A), consent of resolution professionals (Forms AA & AB), claims submission by creditors (Forms B to F), withdrawal of CIRP (Form FA), invitation for expression of interest (Form G), approval of resolution plan (Form GA), and compliance certificate (Form H). These formats are now required to be used by insolvency professionals and stakeholders to ensure uniformity, procedural consistency, and improved efficiency in insolvency proceedings. The circular also reflects a shift towards notifying forms through circulars rather than embedding them in regulations, thereby allowing greater flexibility and timely updates in documentation requirements.

2. IBBI ISSUES GUIDELINES FOR CONDUCTING VALUATION UNDER IBC

The Insolvency and Bankruptcy Board of India (IBBI) has issued comprehensive Guidelines for Conducting Valuation under the Insolvency and Bankruptcy Code, 2016, applicable with immediate effect. The circular mandates standardised formats, detailed documentation, and uniform reporting practices for valuation assignments undertaken under various insolvency processes including CIRP, liquidation, and voluntary liquidation. It aims to bring consistency, transparency, and comparability in valuation reports, addressing earlier variations in methodologies and assumptions. Registered valuers are now required to maintain proper working papers, clearly justify valuation approaches, and adhere to prescribed reporting standards, thereby enhancing the reliability and credibility of valuation outcomes within the insolvency framework.

3. IBBI NOTIFIES CIRP (THIRD AMENDMENT) REGULATIONS, 2026

The Insolvency and Bankruptcy Board of India (IBBI) has notified the Insolvency Resolution Process for Corporate Persons (CIRP) (Third Amendment) Regulations, 2026, pursuant to the amendments introduced under the Insolvency and Bankruptcy Code (Amendment) Act, 2026. The amendments are aimed at enhancing transparency, improving information availability, and reducing litigation during the insolvency process. Key changes include mandatory comprehensive disclosures at the initiation stage by operational creditors and corporate applicants, such as GST records, e-way bills, details of part-payments, guarantees, and ongoing proceedings. The amendments also seek to streamline insolvency proceedings and align regulatory provisions with the updated framework under the Code, including provisions relating to the treatment of guarantors’ assets, thereby strengthening the overall efficiency and credibility of the CIRP mechanism.

![]()

![]()

Disclaimer Information in this note is intended to provide only a general update of the subjects covered. It is not intended to be a substitute for detailed research or the exercise of professional judgment. KNM accepts no responsibility for loss arising from any action taken or not taken by anyone using this publication. Updates for the period 30.06.2026