Introduction: The Hidden Threat in Your Tax Return

The Income Tax Department of India has significantly escalated its data-mining operations regarding foreign assets. Through the Automatic Exchange of Information (AEOI) framework, the government now receives real-time data on overseas bank accounts and equity holdings. For many Non-Resident Indians (NRIs) and returning executives, this presents an immediate and severe compliance crisis.

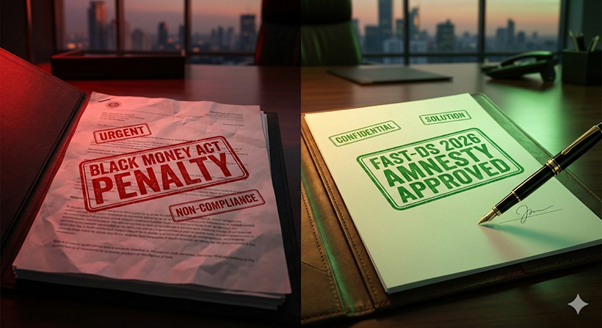

If you hold Employee Stock Ownership Plans (ESOPs) from a foreign parent company or maintain legacy bank accounts overseas, you are currently under the regulatory microscope. The urgency of this situation cannot be overstated. A technical oversight in your past Income Tax Returns (ITR) could now trigger devastating financial penalties under the Black Money Act (BMA).

Fortunately, the newly announced Foreign Asset Settlement and Tax Dispute Scheme (FAST-DS) 2026 provides a critical, limited-time escape route. This article outlines how Category B of this scheme can save you from catastrophic penalties.

The “Schedule FA” Compliance Trap

A widespread misconception among high-net-worth individuals and corporate executives is that paying tax resolves all liabilities. Many taxpayers diligently declare their foreign salary, capital gains, or dividend income. They pay the applicable Indian taxes perfectly on time. However, their tax consultants make a fatal administrative error: failing to fill out “Schedule FA” (Foreign Assets).

Schedule FA is a mandatory disclosure section in the Indian ITR for anyone holding foreign bank accounts, financial interests, immovable property, or equity shares outside India. This includes unvested and vested ESOPs granted by global headquarters. The tax law treats the taxation of income and the disclosure of the asset as two entirely separate legal obligations.

Under the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015, the penalty for failing to report a foreign asset in Schedule FA is a flat ₹10,00,000 per assessment year. If you missed reporting an overseas bank account for three years, you face a ₹30,00,000 penalty, even if that account only held a minimal balance and generated no taxable interest.

Understanding FAST-DS 2026 Category B

To clear the massive backlog of technical litigation, the government has introduced FAST-DS 2026. Category B of this scheme is specifically engineered for “Technical Reporting Lapses.” This category targets individuals who acted in good faith—meaning they offered the underlying income to tax in India but inadvertently missed the Schedule FA disclosure.

Under Category B, eligible taxpayers can regularize their past ITRs by paying a one-time, flat compounding fee of ₹100,000. Paying this fee grants absolute immunity from the ₹10,00,000 per year penalty under the Black Money Act and prevents any future prosecution related to that specific non-disclosure.

Comparison: Black Money Act Penalties vs. FAST-DS 2026 Category B

| Parameter | Standard Black Money Act (BMA) | FAST-DS 2026 Category B Amnesty |

| Penalty Amount | ₹10,00,000 per Assessment Year | Flat ₹100,000 total fee |

| Prosecution Risk | High risk of rigorous imprisonment | Complete immunity from prosecution |

| Multiple Year Impact | Cumulative (e.g., 5 years = ₹50 Lakh) | Single flat fee covers all past lapses |

| Eligibility Criteria | Applies to all non-disclosures | Must prove income was previously taxed |

Step-by-Step Regularization Guide for ESOPs and Bank Accounts

To utilize this amnesty window, executives must move swiftly and systematically. The first step is a comprehensive Portfolio Mapping. You must collate all foreign broker statements (like E*TRADE or Morgan Stanley), overseas bank statements, and past Indian ITRs. Every single asset must be cross-referenced against your Schedule FA filings for the past seven years.

The second step is Eligibility Assessment. To qualify for Category B, you must demonstrate a clear audit trail proving that whenever a taxable event occurred (such as the exercise of ESOPs or the receipt of foreign dividends), the income was included in your Indian tax computation. If taxes were evaded, you fall into a different, much costlier category of the scheme.

The final step is the preparation and submission of the FAST-DS declaration. This requires drafting a highly technical legal submission. The declaration must precisely quantify the peak balance of the foreign bank accounts and the fair market value of the ESOPs, mapping them to the exact assessment years where the reporting lapse occurred.

If you are a corporate executive facing these discrepancies, immediate action is required. We strongly advise engaging experts in [Link to KNM Management Advisory Services] to conduct a preemptive audit of your foreign assets before the tax department issues a formal notice.

The KNM India Advantage in Tax Dispute Resolution

Resolving international tax discrepancies requires more than basic accounting; it requires sophisticated legal and financial strategy. KNM India provides premier Management Advisory Services designed to protect the wealth and reputation of C-suite executives and NRIs. Our specialized tax teams conduct forensic reviews of your past filings to identify hidden BMA exposures before they trigger statutory notices.

Furthermore, we are recognized as a leading Accounting firm in India with Japanese support. We understand that executives returning from assignments in Tokyo or working for Japanese multinationals face unique complexities regarding ESOP taxation and cross-border banking. Our bilingual desks and deep understanding of international tax treaties allow us to seamlessly bridge the gap between foreign financial documents and strict Indian compliance standards.

Do not wait for a scrutiny notice to arrive. The FAST-DS 2026 window is a temporary relief measure that demands immediate attention. Protect your assets and your professional standing by rectifying past Schedule FA lapses today.

[Link to KNM Assurance & Audit Services] [Link to KNM NRI Specialized Services] [External Link to Income Tax Department: e-Filing Portal]

Key Takeaways

- The Schedule FA Trap: Paying tax on foreign income is not enough; failing to report the underlying foreign asset in Schedule FA attracts severe penal action.

- Draconian Penalties: The Black Money Act (BMA) imposes a strict ₹10,00,000 penalty per year for mere non-disclosure of foreign bank accounts or ESOPs, even without tax evasion.

- The FAST-DS 2026 Window: Category B of the new amnesty scheme allows taxpayers who previously offered income to tax to regularize their disclosure lapses for a flat ₹100,000 fee.

- Strategic Resolution: Engaging experts in Management Advisory Services is critical to audit past filings, quantify the exposure, and successfully file under the limited-time FAST-DS window.

Frequently Asked Questions (FAQs)

Q1: Does the ₹100,000 FAST-DS fee apply per year or per asset? Under Category B provisions, the ₹100,000 fee is a consolidated flat fee intended to cure the technical reporting lapse across multiple assessment years, provided the taxpayer meets all other eligibility criteria regarding the payment of taxes.

Q2: I hold unvested ESOPs that generate no income. Do I still need to report them? Yes. Indian tax law requires the disclosure of any financial interest held overseas. Even if the ESOPs are unvested and no taxable event has occurred, failing to report them in Schedule FA attracts the ₹10 Lakh BMA penalty.

Q3: What if I never paid tax on the foreign income because I was unaware? If taxes were not paid on the foreign income, you do not qualify for Category B (the ₹1 Lakh flat fee). You must apply under Category A of the scheme, which involves paying the pending tax, plus substantial interest and elevated penalties.

Q4: How can an Accounting firm in India with Japanese support help me? If your assets include Japanese broker accounts or employment benefits from a Japanese parent company, translating those documents and aligning them with the Indian financial year requires specialized expertise to ensure the FAST-DS declaration is perfectly accurate.

Q5: Will filing under FAST-DS 2026 trigger an audit of my entire tax return? No. The scheme is designed to ring-fence the specific issue of foreign asset disclosure. Declarations made under FAST-DS are generally granted immunity from being used as evidence to reopen other unrelated aspects of your tax assessments.

🌐 Website: https://knmindia.com

📞 Telephone and Contact Information:

Tokyo: +81-3-6869-0850

India: +91-124-4295170, +91-99105-04170

📧 Email: services@knmindia.com

📩 Contact: The contact page on knmindia.com allows you to contact our experts.