Considering the second wave of Covid-19, in order to provide ease of compliance to the taxpayers, the GST council had recommended various relaxations under the GST law. Presented herewith is a consolidated summary of various notifications issued for implementation of such relaxations:

A. Relaxations recommended by GST Council: 43rd GST Council Meeting

(Notified by respective notifications dated 01st June 2021)

The following are some of the key relaxations suggested by the GST council and notified, for ease of compliance of taxpayers:

1. Relaxation in filing of returns and waiver of late fee

| Relaxation | Particulars | Revised Dates |

|---|---|---|

| Filing of: GSTR-3B and waiver of Late fee Notification nos. 19/2021 dated 01st June 2021 | Return Period Covered: March, April and May 2021 | .. |

| Category-A: Taxpayers with turnover* > Rs. 5 Crores Relaxation allowed: 15 days from original due date *during FY 2020-21 | March 2021- 5th May2021 April 2021- 4th June 2021 May 2021- 5th July 2021 | |

| Category-B: Taxpayers with turnover < Rs. 5 Crores Relaxation allowed: For March 2021- 60 days from original due date For April 2021- 45 days from original due date For May 2021- 30 days from original due date | March 2021-19th June 2021 April 2021- 4th July 2021 May 2021- 20th July 2021 | |

| Category-C: For Quarterly taxpayers (QRMP Scheme) Relaxation allowed: From Jan to Mar 2021- 60 days from original due date | Cat-1 states – 21st June2021 Cat-2 states- 23rd June2021 | |

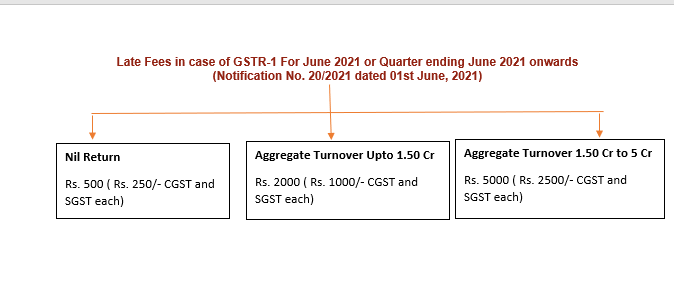

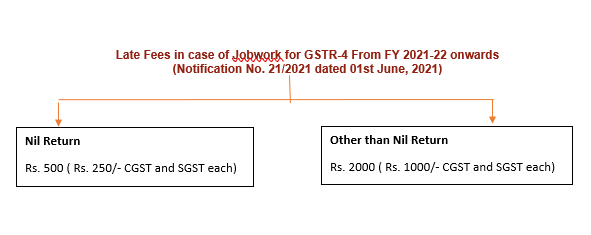

| Filing of GSTR-1, IFF, GSTR-4, ITC-04 (Notification no. 17/2021, 25 /2021, and26/2021 dated 01st June, 2021) Issuance of Notice filing of appeal, furnishing of returns, completion of proceedings (Notification no.24/2021 dated 01st June, 2021) | For Regular Taxpayers: GSTR-1 For Regular Taxpayers: IFF For Composition Dealers (Quarterly) : GSTR-4 For Job-Worker: ITC-4- For Completion of any proceeding or passing of any order or issuance of any notice, intimation, notification, sanction or approval, by any authority, commission or tribunal – Filing of any appeal, reply or application or furnishing of any report, document, return, statement etc. Original Due Date: 15th April 2021 to 29th June 2021 | May 2021: 26th June 2021 May 2021: 28th June 2021 March 2021: 31st July 2021 March 2021: 30th June 2021Revised Due Date: 30th June 2021 |

2. Reductions in Interest rates on delay in deposit of GST

| Relaxation | Particulars |

|---|---|

| Interest payment (Notification no.18/2021 dated 01st June 2021) | Category-A: – No relaxation from Interest – Interest @ 9% p.a. if filed within relaxed period – Interest @ 18% p.a. if filed after relaxed periodCategories B and C: For March 2021 – Relaxation from Interest for first 15 days from original due date – Interest @ 9% p.a. from 16th day till 60 days – Interest @ 18% p.a. after 60th day For April 2021 – Relaxation from Interest for first 15 days from original due date – Interest @ 9% p.a. from 16th day till 45 days – Interest @ 18% p.a. after 45th day For May 2021 – Relaxation from Interest for first 15 days from original due date – Interest @ 9% p.a. from 16th day till 30 days – Interest @ 18% p.a. after 30th day For Composition dealers – Relaxation from Interest for first 15 days from original due date – Interest @ 9% p.a. from 16th day till 60 days – Interest @ 18% p.a. after 60th day |

| ITC as per Rule 36(4) of CGST Rules, 2017 (Notification no.27/2021 dated 01st June 2021 | – ITC Availment on the basis of GSTR-2A to be checked cumulatively for the tax period April, May and June 2021; – Any adjustment for the said periods shall be made in Return in Form GSTR 3B to be furnished for the month of June 2021 |

| Filing of GSTR-3B, GSTR-1 or using IFF, Through EVC (Notification no.27/2021 dated 01st June 2021) | – Registered person registered under the provisions of the Companies Act, 2013 allowed to verify GSTR-3B, GSTR-1 or IFF, through electronic verification code till 31st August 2021. |

| Appeals to Appellate Tribunal (Notification no.16/2021 dated 01st June 2021) | Provisions of section 112 of the Act relating to Appeals to appellate tribunal shall come into force from 1st June, 2021. |

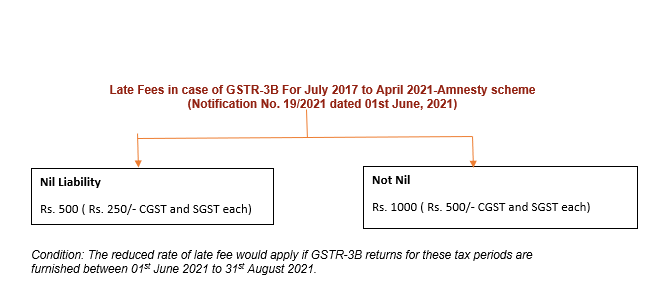

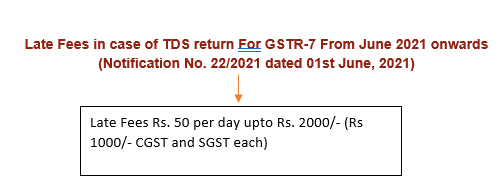

3. Capping of Late fee- Introduction of Amnesty Scheme for Non-Filers

4. Filing of Annual Return for Financial Year 2020-21

– In order to ease compliance in filing of Annual return- GSTR-9 for the FY 2020-21, amendments were made in Finance Act, 2021 omitting the requirement for obtaining certified Reconciliation Statement in GSTR-9C, from a chartered accountant.

– Accordingly, compliance for the FY 2020-21 regarding annual return is as under:

| Annual Aggregate Turnover for FY 2020-21 | Compliance Requirement |

|---|---|

| Exceeding Rs. 5 Crores | Mandatory to file self-certified GSTR-9C, along with Annual return in GSTR-9 |

| Up to Rs. 2 Crores | Optional to file Annual Return in GSTR-9/9A. |

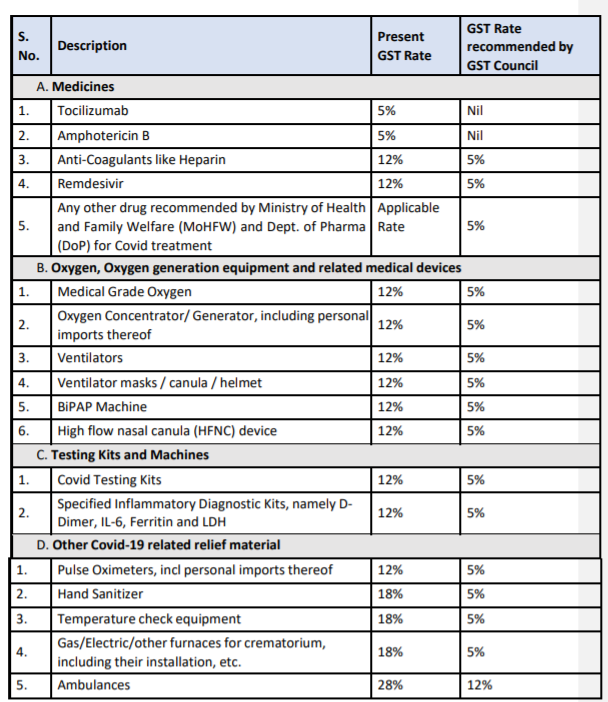

B. Reduction in GST rates for items of Covid-19 relief and management: 44th GST Council Meeting

The GST council in its 44th meeting held on 12th June, 2021 recommended reduction in GST rates on goods on specific items (tabulated below) being used in COVID -19 relief and management.

The said reduction shall be in force up to 30th September 2021. Corresponding exemptions have also been provided under the Customs Act for the benefit of taxpayers:

Disclaimer: Information in this note is intended to provide only a general update of the subjects covered. It is not intended to be a substitute for detailed research or the exercise of professional judgment. KNM accept no responsibility for loss arising from any action taken or not taken by anyone using this publication.