A key understanding of intricacies of newly introduced section 194-Q relating to withholding tax on purchase of goods and its interplay with Section 206AA/206AB, relating to deduction of TDS at higher rates, is essential for day-to-day compliance by organizations. The said provisions of section 194-Q are applicable from 01st July 2021. As special provision for deducting TDS is applicable from 01st July 2021, similarly, section 206CCA is also applicable from 01st July 2021 for the purpose of collecting higher rate of TCS for non-filer of Income tax return.

In this article, we have tried to compile the aforesaid background, along with FAQs and recent changes made at the reporting portal of Income Tax, where a compliance check functional utility released by CBDT for the ease of tax deductor has been introduced.

A. Background

- 194Q: TDS on purchase of goods

The Finance Act, 2020, inserted section 206C(1H) which was effective from 01st October 2020. As per section 206C(1H), seller is liable to collect of TCS @ 0.1% from buyer on amount received as consideration for the sale of goods in excess of Rs. 50 lakhs in any previous year. But to curve-out certain loop-holes, the Finance Bill, 2021, introduced a new Section 194Q to provide for deduction of tax i.e. TDS @ 0.1% by a buyer from the purchase of goods in excess of Rs. 50 lakhs in any previous year.

Accordingly, since from current year, corresponding sections are applicable both for seller and buyer, therefore, buyer and seller need to be very careful while charging or collecting TDS/TCS on goods.

- Section 206AB & 206CCA: Higher rate of TDS/TCS for Non-Filer of Returns

We are already well versed that for non-furnishing of PAN at the time of TDS/TCS, Section 206AA/206CC of the Act provides for higher rate of TDS/TCS gets attracted, now CBDT is getting more stringent for non-furnishing of ITR for taxpayers having higher TDS/TCS credits.

Therefore, similar provision has been inserted by Finance Act 2021, w.e.f. 01st July 2021. As per new section 206AB as a special provision for providing higher rate of TDS and also a new section 206CCA for providing a higher rate of TCS for specified persons.

Rates as per Section 206AB (w.e.f. 01.07.2021):

Higher of:

- Twice the rate specified in the relevant provision of the Act; or

- Twice the rate rates in force; or

- 5%

Rates as per Section 206CCA (w.e.f. 01.07.2021):

Higher of:

- Twice the rate specified in the relevant provision of the Act; or

- 5%

As per Section 206AB/206CCA, specified person means a person who satisfies both the following conditions: –

- He has not filed the returns of income for both of the two assessment years relevant to the two previous years immediately before the previous year in which tax is required to be deducted/collected. Two previous years to be counted are required to be those whose return filing date under sub-section (1) of section 139 has expired.

- Aggregate of tax deducted at source and tax collected at source is rupees fifty thousand or more in each of these two previous years.

B. Key Action Points for Organizations:

- Check applicability of section 194Q/206AB/206CCA for organization.

- Check which customer fall under ambit of this new provision.

- Review terms and conditions of commercial agreements already entered by buyer and seller from TDS perspective.

- Amend the Sales-Purchase agreement between the parties by inserting the TDS clause if required.

- Exchange the declaration for applicability of section 194Q as well as 206AB and check each transaction to safeguard for non-applicability of disallowance of 30% u/s 40a(ia). As section 206AB is also applicable on 01 July 2021, hence a revised declaration needs to be obtained after the due date of filing of original return u/s 139(1).

C. Section 194-Q: Snapshot and Interplay with Sec. 206AA/206AB

D. Frequently Asked Questions (FAQs)

As implementation of sections getting complicated, hence it is essential to understand the practical insights on various parties to deduct / collect the withholding taxes.

For the removal of doubts, we have prepared a list of the Frequently asked Questions (FAQs) based on applicability of TDS on purchase of goods under various situations with effect from 01-07-2021 and a glimpse of its interplay with sections 206AB & 206AA, relating to a higher rate of TDS deduction.

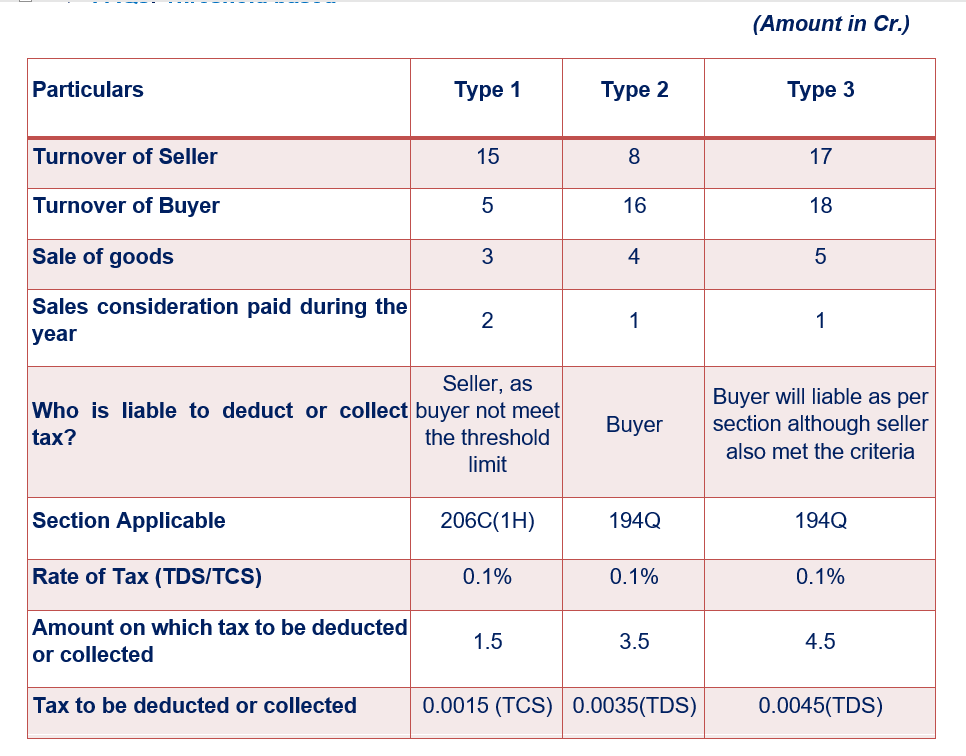

FAQs: Threshold based

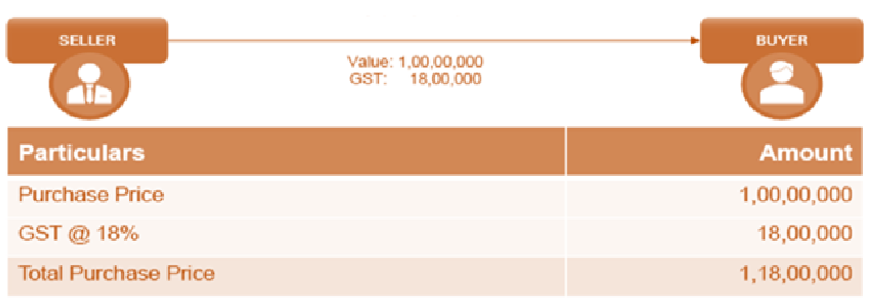

Case Study 1– Whether TDS will be applicable inclusive of GST or not?

As the provision u/s 194Q suggest, being a buyer liable to pay “any sum to any resident” for purchase of any goods of the value exceeding fifty lakh rupees in any previous year, shall at the time of credit or payment thereof by any mode, Therefore the purchase price paid includes GST. Earlier circular was issued for services only. Further clarification from CBDT is awaited.

Earlier in case of 206C(1H) also, every person, being a seller, who receives any amount as consideration for sale of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year, Therefore the sale price received including GST should be sales consideration.

Case Study 2- Whether TDS should be calculated on the ‘total purchase consideration’ (i.e. INR 90,00,000) or the purchase consideration exceeding INR 50,00,000 (i.e. INR 40,00,000)?

As the provision u/s 194Q suggest, being a buyer liable to pay “any sum to any resident” for purchase of any goods of the value exceeding fifty lakh rupees in any previous year, shall at the time of credit or payment thereof by any mode, deduct TDS from buyer 0.1% of the purchase value exceeding fifty lakh rupees. Therefore, TDS should be calculated on INR 40,00,000

Earlier in case of 206C(1H) also, Every person, being a seller, who receives any amount as consideration for sale of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year, shall at the time of receipt of such amount, collect TCS from buyer 0.1% of the sale consideration exceeding fifty lakh rupees. Therefore, TCS should be calculated on INR 40,00,000.

Case Study 3– Whether TDS is required to be deducted on the Payment of INR 90,00,000?

Date of Purchase: 05 June 2021

Date of Payment: 05 July 2021

As the provision u/s 194Q suggest, being a buyer liable to pay “any sum to any resident” for purchase of any goods of the value exceeding fifty lakh rupees in any previous year, shall at the time of credit or payment thereof by any mode, deduct TDS from buyer 0.1% of the purchase value exceeding fifty lakh rupees.

However, where any of the trigger event (i.e., payment or credit) has occurred before the date of applicability of provision i.e. 01st July 2021, no liability to deduct tax will arise.

Accordingly, in this case no liability to deduct TDS shall arise. Further clarification from CBDT is required.

Case Study 4 – Liability of TDS in case of Part Payment?

Date of Purchase: 10th July 2021

Received Part Payment of INR 40,00,000 15th July 2021

Received Part Payment of INR 20,00,000 10th August 2021

As the provision u/s 194Q suggest, being a buyer liable to pay “any sum to any resident” for purchase of any goods of the value exceeding fifty lakh rupees in any previous year, shall at the time of credit or payment thereof by any mode, deduct TDS from buyer 0.1% of the purchase value exceeding fifty lakh rupees. Therefore, here TDS will be deducted on 10th July 2021 when buyer credit the same in his books of account.

Accordingly, TDS would be applicable on amount of Rs. 10 lacs i.e. amount exceeding the threshold limit of Rs. 50 lacs.

- FAQs: Concept Based

Q1: Situation of Dual Liability: Where a transaction is covered by both the provisions – TDS under Section 194Q and TCS under Section 206C(1H), who shall be liable for deduction/collection of tax?

A: The buyer shall have the primary and foremost obligation to deduct the tax and no tax shall be collected on such transaction under Section 206C(1H). Therefore, if buyer is liable to deduct the TDS and actually deducted then there is no need for tax collection by the Seller.

Q2: In Case Buyer fails to deduct or deduct later on: Where a transaction is covered by both the provisions – TDS under Section 194Q and TCS under Section 206C(1H), however, buyer fails to deduct or deducted later on?

A: The buyer shall have the primary and foremost obligation to deduct the tax and no tax shall be collected on such transaction under Section 206C(1H).

However, if buyer fails to deduct the TDS, then seller is liable to collect the same. In such a case, the buyer shall not be treated as an assessee in default u/s 201(1), if he obtains a declaration in Form No.26A from the seller to the effect that such income has been taken into consideration by the seller in his return of income.

Q3: In Case Buyer Voluntarily Deduct TDS: Where buyer doesn’t meet the threshold criteria but voluntarily deducted TDS, will seller be liable for collecting TCS?

A: Seller liable to collect TCS.

Q4: Advance received before 01.07.2021: If buyer made payment before 01.07.2021, will TDS applicable on it?

A: TDS should be deducted where the payment is made or amount is credited on or after 01-07-2021. Thus, where any of the trigger event (i.e., payment or credit) has occurred before the date of applicability of provision, no liability to deduct tax will arise. Further clarification from CBDT is required.

Q5: Will TDS be applicable on Purchase Return?

A: If purchase return is done before recording of TDS then it is possible to recheck the value of goods for the purpose of threshold limit of INR 50 Lakh.

Q6: Can Lower Deduction certificate is applicable on 194Q?

A: No clarification from CBDT. If we take the same colour of 206C(1H) then Lower Deduction is not applicable in this section.

Q7: Whether TDS u/s 194-Q is applicable if buyer is a non-resident?

A: Yes, TDS would be applicable in this case provided the seller is a resident. However, in practical cases, where goods are exported, it may be difficult to apply such provision hence the CBDT may come up a clarification. Further, TCS u/s 206(1H) is not applicable to export of goods.

Q8: Is TDS applicable on purchase of Capital Goods?

A: Yes, it is applicable.

Q9: When two-year purchase payment more than threshold limit i.e. INR 50 Lakh, whether TDS is applicable?

A: TDS will not applicable. For Example, Year 1 purchases INR 30 Lakh and Year 2 purchase INR 40 lakh. In such case, TDS under section 194Q would not arise for any of the above years since the purchase made for any of these years do not exceed INR 50 lakh. However, applicability of TCS need to check u/s 206C(1H).

- FAQs: Punitive Based

Q10: If seller is not furnishing ITR or PAN details and is a specified person?

A: If seller is not furnishing ITR details like acknowledgement No, date of furnishing or PAN details then higher of rate mentioned in section 206AB or 206AA is applicable on seller and buyer is liable to deduct TDS at such higher rate.

For example, in case of TDS needs to be deducted u/s 194Q and seller is not furnishing requisite details as mentioned then as per section 206AB TDS rates comes to 5% but due to non-furnishing of PAN 206AA is also applicable comes into play i.e. 5% rate, then @5% TDS will be applicable (higher of two, though in this case it is same).

Rates as per Section 206AB (w.e.f. 01.07.2021):

Higher of:

- Twice the rate specified in the relevant provision of the Act; or

- Twice the rate rates in force; or

- 5%

Rates as per Section 206AA:

Higher of:

- Twice the rate specified in the relevant provision of the Act; or

- Twice the rate rates in force; or

- 20% (in case of 194Q &194O, 5% will be substituted in place of 20%)

E. Compliance Check Functionality introduced by CBDT

To ease the functionality of section 206AB/CCA, CBDT comes with a utility vide circular dated 21st June 2021 to check the specified person. The functionality is based on following logic given in the circular:

- A list of specified persons is prepared as on the start of the financial year 2021-22, taking previous years 20 18-19 and 2019-20 as the two relevant previous years. List contains name of taxpayers who did not file return of income for both assessment years 2019-20 and 2020-21 and have aggregate of TDS and TCS of fifty thousand rupees or more in each of these two previous years.

- During the financial year 2021-22, no new names are added in the list of specified persons. This is a taxpayer friendly measure to reduce the burden on tax deductor a collector of checking PANs of non-specified person more than once during the financial year.

- If any specified person files a valid return of income (filed & verified) for assessment year 2019-20 or 2020-21 during the financial year 2021-22, his name would be removed from the list of specified persons. This would be done on the date of filing of the valid return of income during the financial year 2021-22.

- If any specified person files a valid return of income (filed & verified) for assessment year 2021-22, his name would be removed from the list of specified persons. This will be done on the due date of filing of return of income for A. Y. 2021-22 or the date of actual filing of valid return (filed & verified) whichever is later.

- If the aggregate of TDS and TCS, in the case of a specified person, in the previous year 2020-21, is less than fifty thousand rupees, his name would be removed from the list of specified persons. This would be done on the first due date under sub-section (I) of section 139 of the Act falling in the financial year 2021-22. For the financial year 2021-22 this due date of3I” July 2021 has been extended to 30th Sept 2021.

- Belated and revised TCS & TDS returns of the relevant financial years filed during the financial year 2021-22 would also be considered for removing persons from the list of specified persons on a regular basis.

Note: The list would be drawn afresh at the start of each financial year and the above process would have to be repeated. For example, at the beginning of the financial year 2022- 23 a fresh list would be prepared with previous years 2019-20 and 2020-21 as the two relevant previous years. Then, no name would be added to the list of specified persons during the financial year and only name would be removed based on the logic given in the 3rd to 6th above.

Utility Functionality:

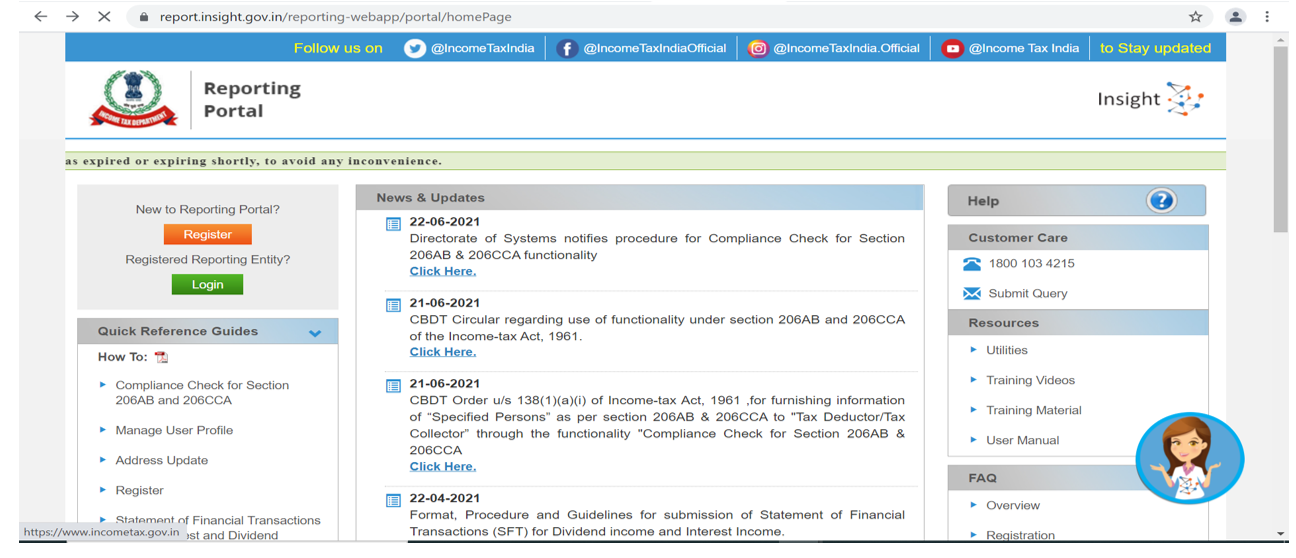

The Utility is available on reporting portal of Income Tax Department and can be login through the Principal Officers of the registered TAN at the home page of Reporting Portal (After Login).

- FAQs

Q1: What are the steps in registration for “Compliance Check for Section 206AB & 206CCA” functionality?

A:To access the “Compliance Check for Section 206AB & 206CCA” functionality, tax deductors/collectors need to register through TAN on the Reporting Portal of Income-tax Department. Following steps may be followed for registration of TAN on reporting portal:

Step: 1 Go to Reporting Portal at URL https://report.insight.gov.in.

Step: 2 On the left sidebar of the Reporting Portal homepage, click on Register button.

Step: 3 User is redirected to the e-filing login page. Or

Step: 4 Directly navigated to e-filing portal through http://www.incometax.gov.in/

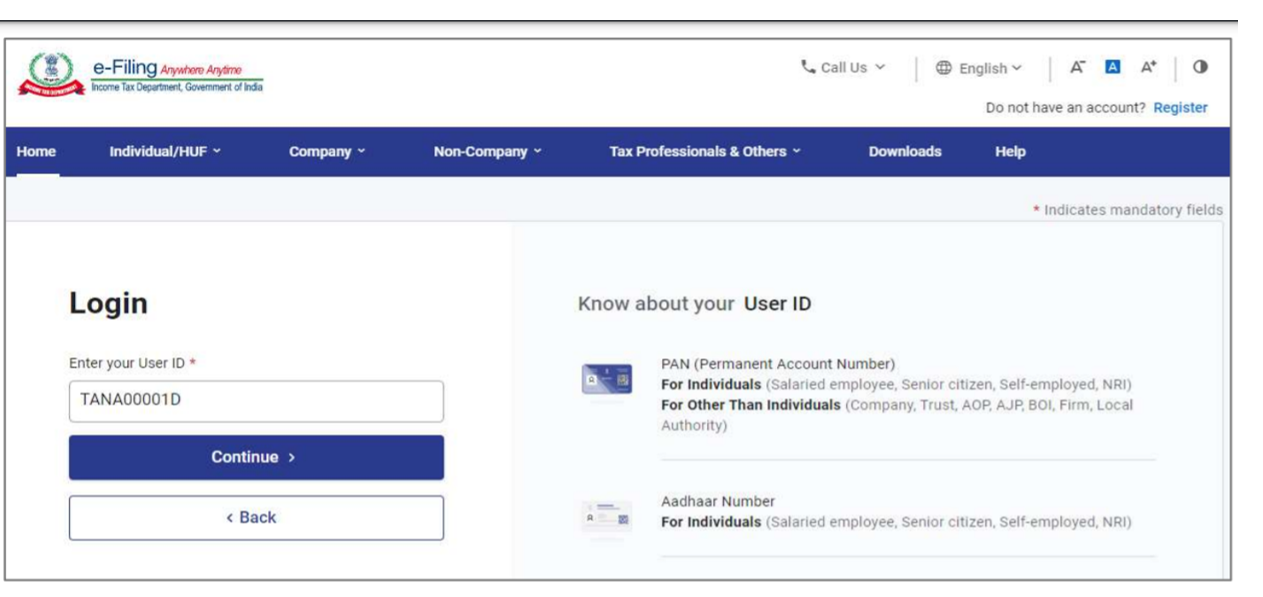

Step: 5 Log in to e-filing using e-filing login credential of TAN.

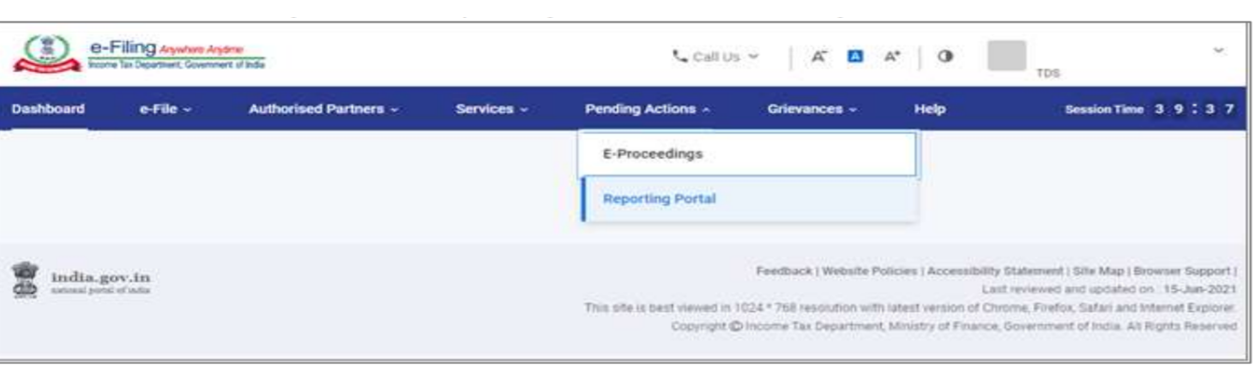

Step: 6 Under “Pending Actions”, select “Reporting Portal”.

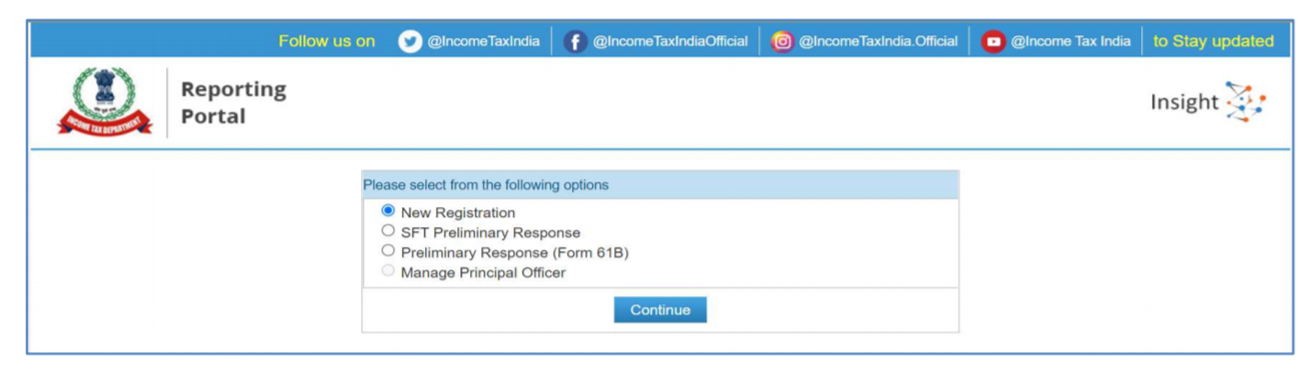

Step: 7 After being redirected to the Reporting portal, select New Registration option and click Continue.

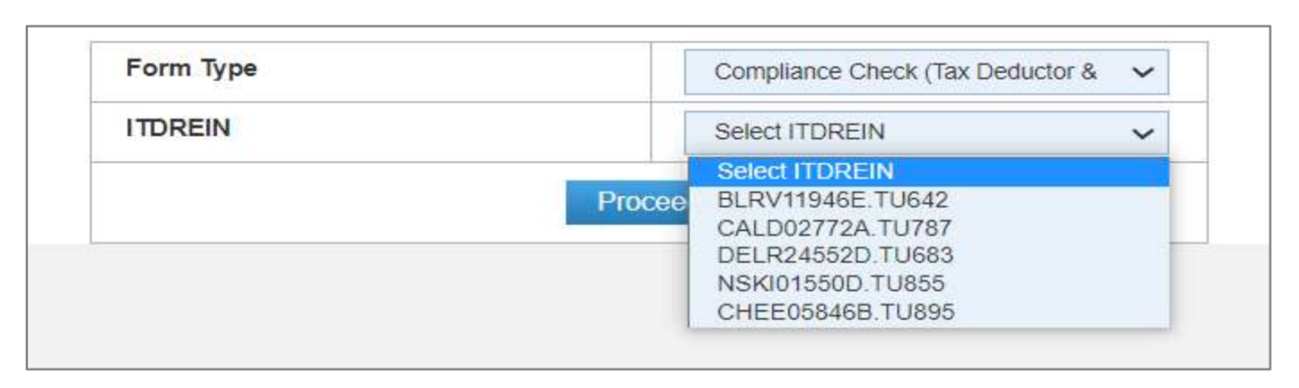

Step: 8 On the next screen, select the Form type as Compliance Check (Tax Deductor & Collector). The Entity Category will be displayed based on the category in which TAN is registered at e-filing. Click Continue to navigate to entity details page.

Step: 9 Enter relevant entity details on entity details page and click on “Add Principal Officer” button to add Principal Officer.

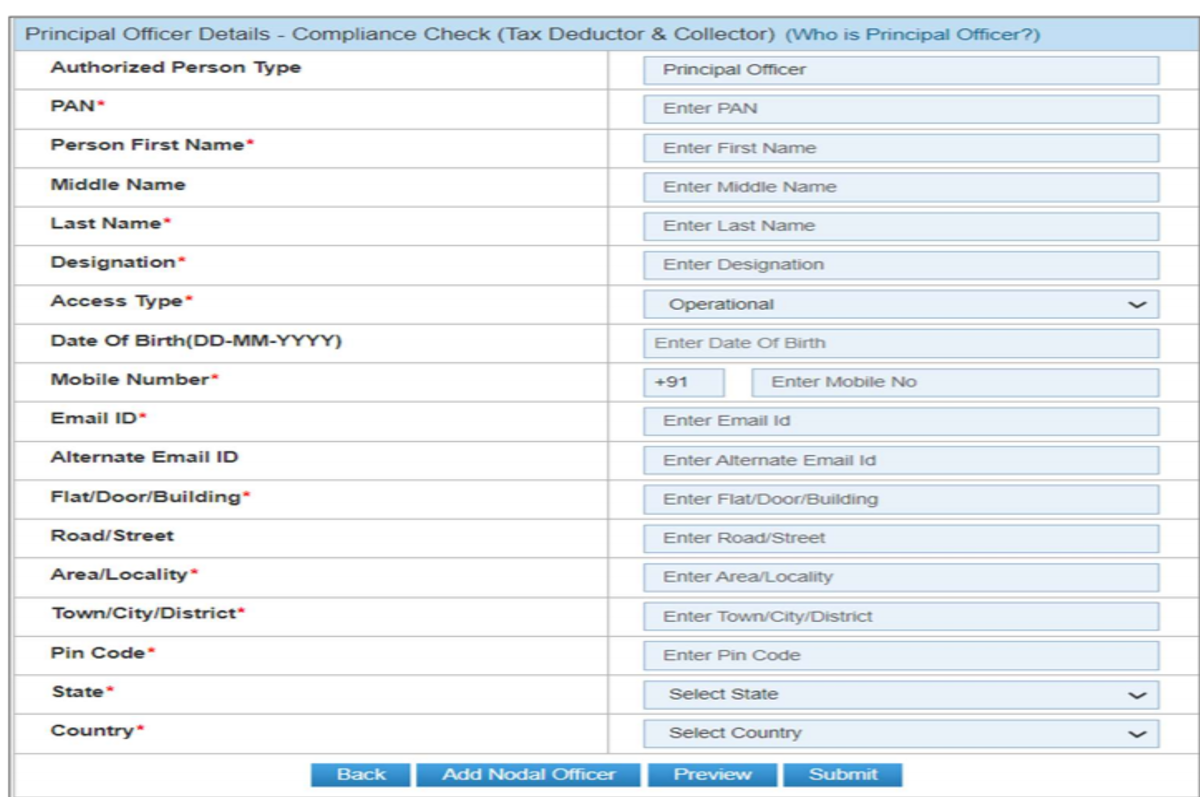

Step: 10 Enter Principal Officer details on the Principal Officer Details page.

Step: 11 If more users such as Nodal Officer, Alternate Nodal Officer and other users are to be registered at this instance, adding the details of such users can be continued, otherwise the same can be done after registration also.

Step: 12 Click on Preview button to view the entered entity and principal officer details.

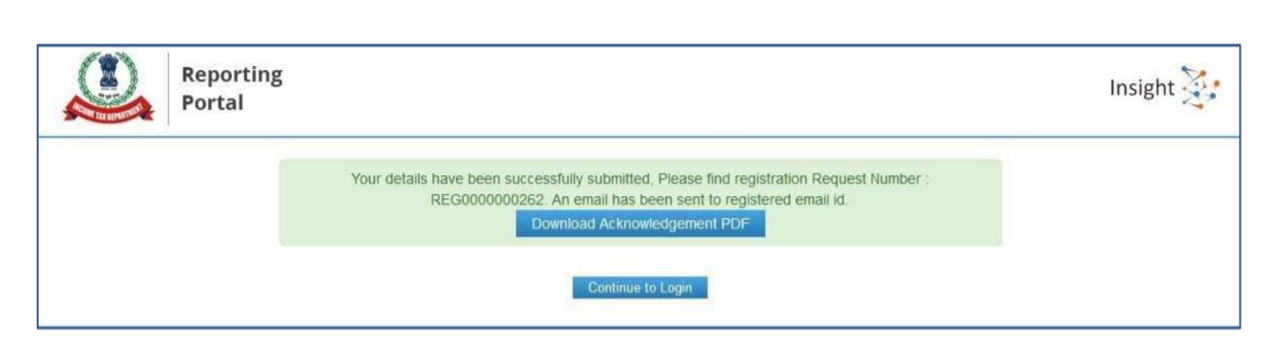

Step: 13 Click on Submit button to submit the registration request.

Step: 14 Acknowledgement receipt of registration request is provided through portal and the same will also be shared through an email notification to the Principal Officer.

Step: 15 Once the registration request is approved by Income tax Department, email notification will be shared with the Principal Officer along with ITDREIN details and login credentials

Q2: How can the Principal Officer access the “Compliance Check for Section 206AB & 206CCA” functionality?

A: Following steps may be followed for registration of TAN on reporting portal,

Step: 1 Go to Reporting Portal at URL https://report.insight.gov.in.

Step: 2 On the left sidebar of the Reporting Portal homepage, click the Login button.

Step: 3 Enter the required details (of Principal Officer) in the respective fields (PAN and Password as received in the email or updated password) and click Login to continue.

Step: 4 If Principal Officer’s PAN is registered for multiple Forms & ITDREIN, he/she needs to select Form type as Compliance Check (Tax Deductor & Collector) and associated ITDREINs from the drop-down.

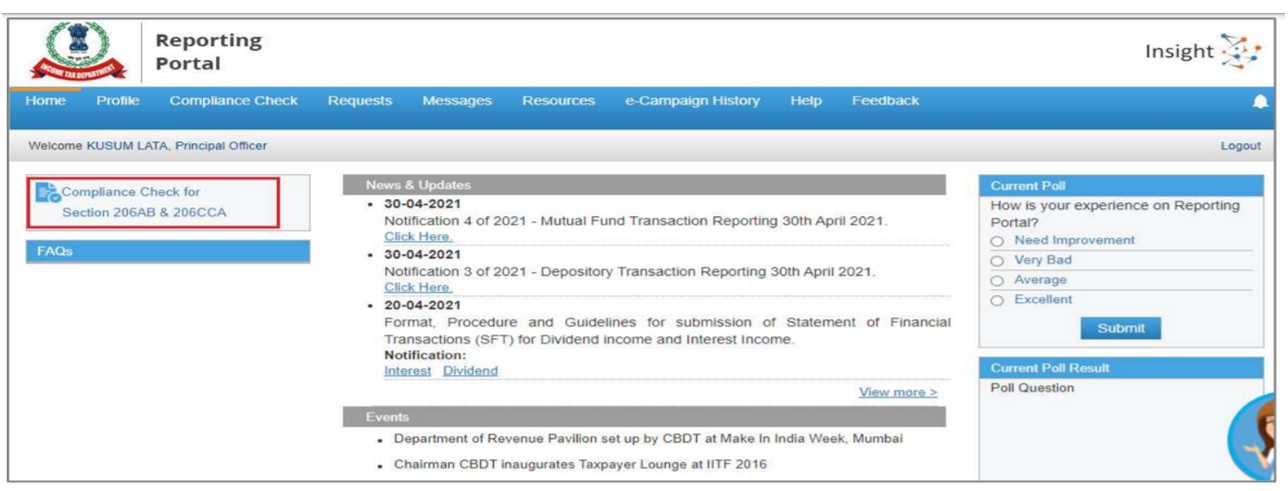

Step: 5 After successfully logging in, the home page of Reporting Portal appears.

Step: 6 Click on Compliance Check for Section 206AB & 206CCA link provided as shortcut on left panel.

Q3: What are the various modes available in the functionality for verifying Specified Person status of a PAN as per section 206AB & 206CCA?

A: Upon clicking Compliance Check for Section 206AB & 206CCA at home page, the compliance check functionality page appears. Through the functionality, tax deductors or collectors can verify if any person (PAN) is a “Specified Person” as defined in Section 206AB & 206CCA.

The same can be done in two modes:

- PAN Search: To verify for single PAN

- Bulk Search: To verify for PANs in bulk

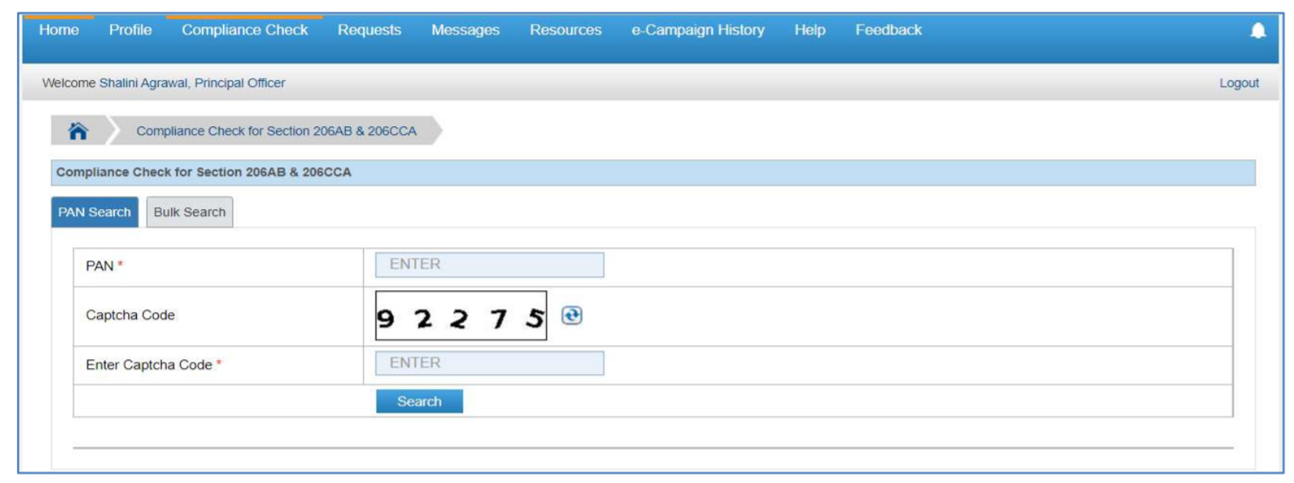

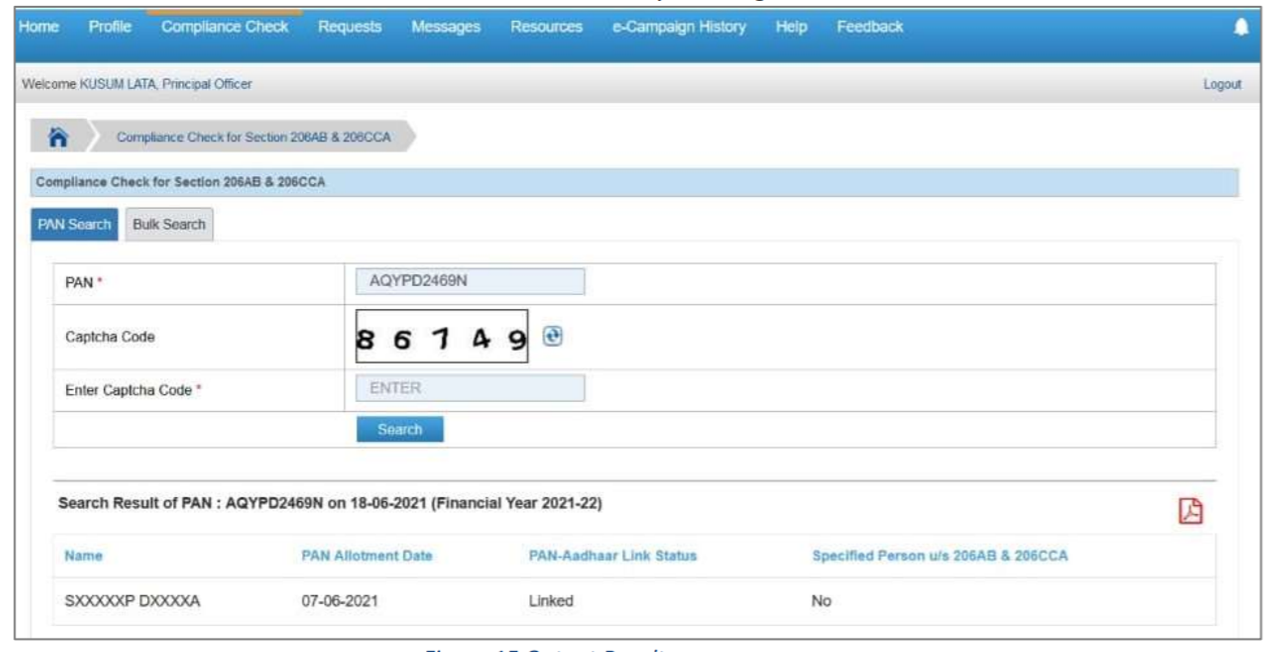

PAN Search (Single PAN Search)

Step 1: Select PAN Search tab under Compliance Check for Section 206AB & 206CCA functionality.

Step 2: Enter valid PAN & captcha code and click Search.

Following Output result will be displayed upon entering a valid PAN & captcha code. Output result will not be shown if Invalid PAN is entered.

Output Result–

- Financial Year: Current Financial Year

- PAN: As provided in the input.

- Name: Masked name of the Person (as per PAN).

- PAN Allotment date: Date of allotment of PAN.

- PAN-Aadhaar Link Status: Status of PAN-Aadhaar linking for individual PAN holders as on date. The response options are Linked (PAN and Aadhaar are linked), Not Linked (PAN & Aadhaar are not linked), Exempt (PAN is exempted from PAN-Aadhaar linking requirements as per Department of Revenue Notification No. 37/2017 dated 11th May 2017) or Not-Applicable (PAN belongs to non-individual person).

- Specified Person u/s 206AB & 206CCA: The response options are Yes (PAN is a specified person as per section 206AB/206CCA as on date) or No (PAN is not a specified person as per section 206AB/206CCA as on date). Output will also provide the date on which the “Specified Person” status as per section 206AB and 206CCA is determined.

Step 3: Click PDF icon to download the details in PDF format.

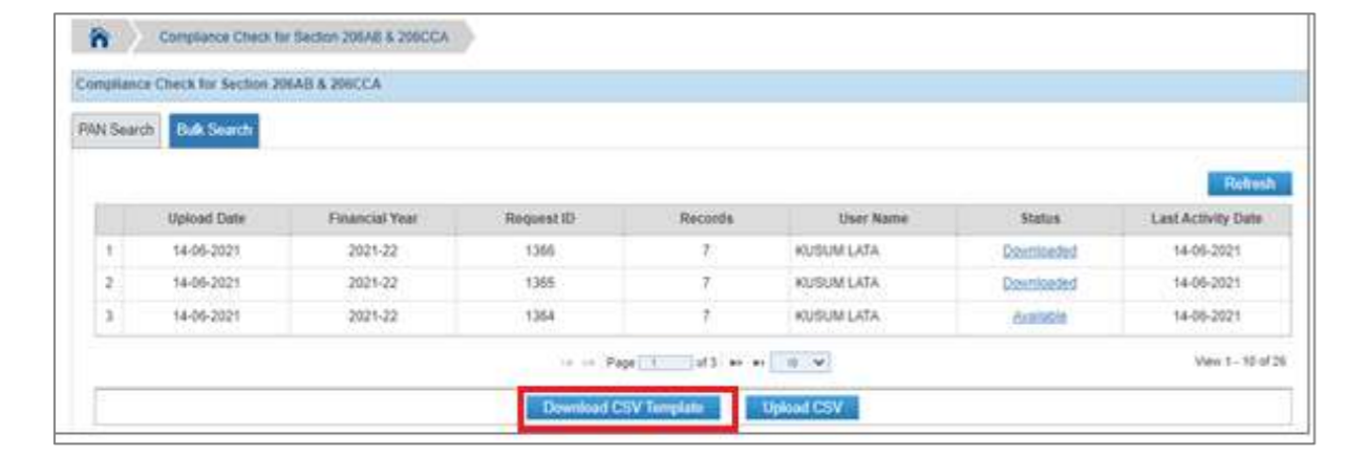

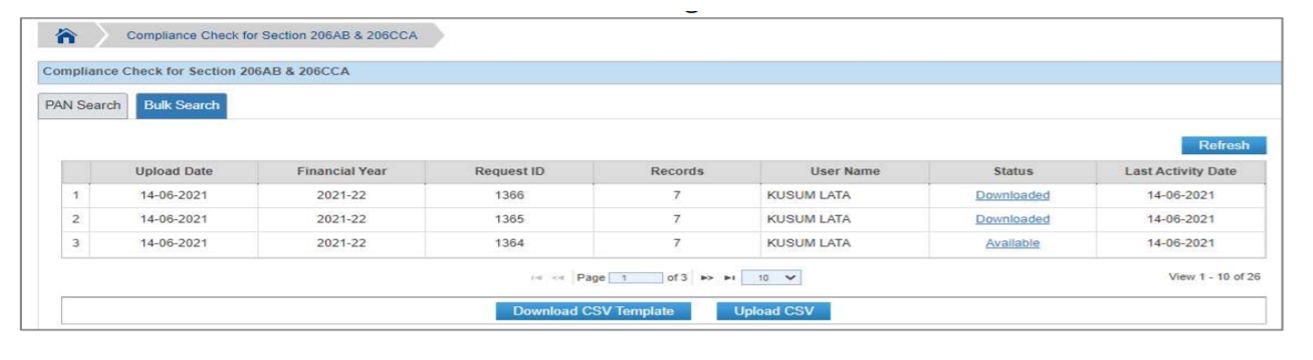

Bulk Search

Step 1: Select “Bulk Search” tab.

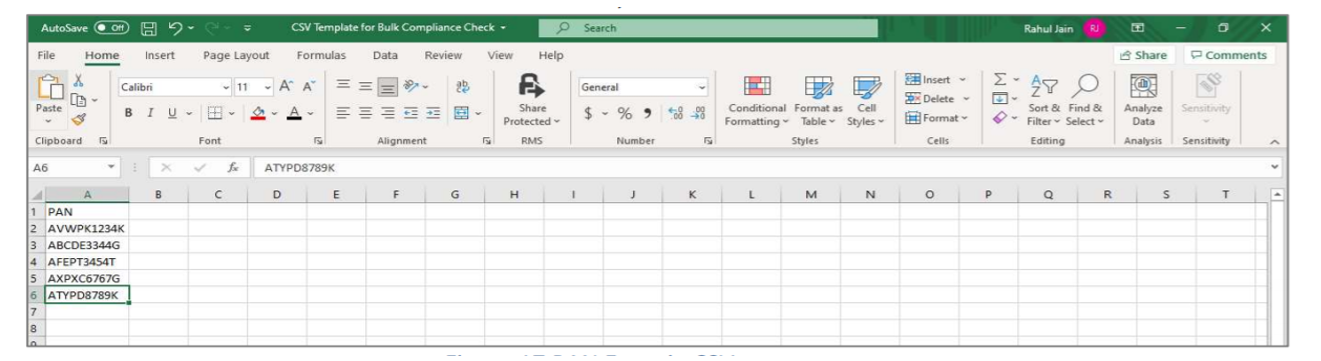

Step 2: Download the CSV Template by clicking on “Download CSV template” button.

Step 3: Fill the CSV with PANs for which “Specified Person” status is required. (Provided PANs should be valid PANs and count of PANs should not be more than 10,000).

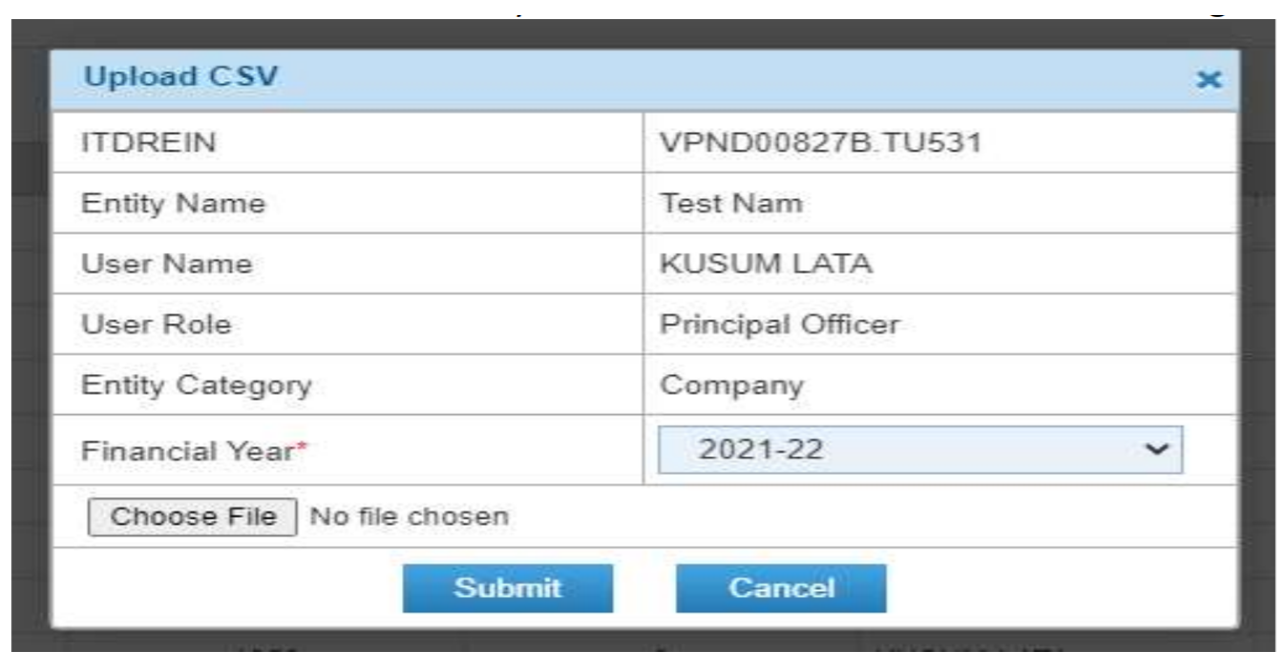

Step 4: Upload the CSV by clicking on “Upload CSV” button.

Step 5: Uploaded file will start reflecting with Uploaded status. The status will be as follows:

- Uploaded – The CSV has been uploaded and pending for processing.

- Available – Uploaded CSV has been processed and results are ready for download.

- Downloaded – The user has downloaded the output results CSV.

- Link Expired – Download link has been expired.

Step 6: Download the output result CSV once status is available by clicking on Available link.

Step 7: After downloading the file, the status will change to Downloaded and after 24 hours of availability of the file, download link will expire and status will change to Link Expired.

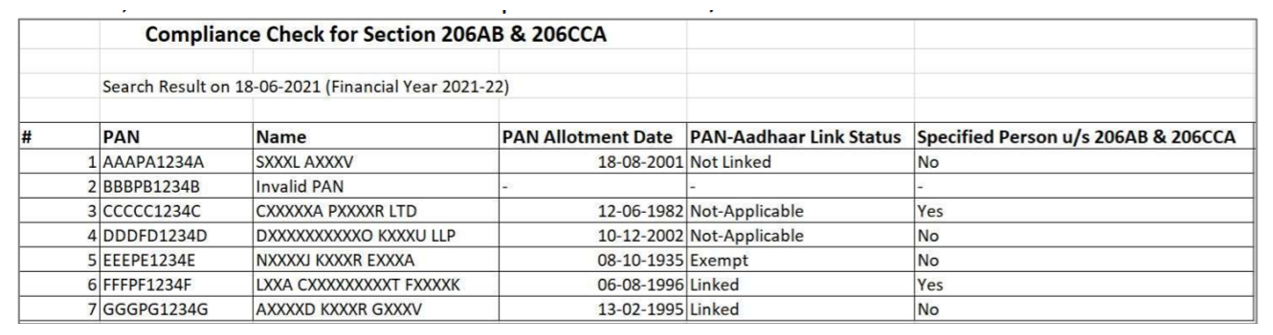

Output Result (CSV): Output result CSV file will have following details:

- Financial Year: Current Financial Year

- PAN: As provided in the input. Status shall be “Invalid PAN” if provided PAN does not exist.

- Name: Masked name of the Person (as per PAN).

- PAN Allotment date: Date of allotment of PAN.

- PAN-Aadhaar Link Status: Status of PAN-Aadhaar linking for individual PAN holders as on date. The response options are Linked (PAN and Aadhaar are linked), Not Linked (PAN & Aadhaar are not linked), Exempt (PAN is exempted from PAN-Aadhaar linking requirements as per Department of Revenue Notification No. 37/2017 dated 11th May 2017) or Not-Applicable (PAN belongs to non-individual person).

- Specified Person u/s 206AB & 206CCA: The response options are Yes (PAN is a specified person as per section 206AB/206CCA as on date) or No (PAN is not a specified person as per section 206AB/206CCA as on date).

Output will also provide the date on which the “Specified Person” status as per section 206AB and 206CCA is determined.

Concluding Remarks

Provisions regarding withholding of taxes at higher rates for non-furnishing of PAN already exist under the Income Tax law. Introduction of Section 206AB would serve as a further step, in addition furnishing of PAN, to ensure compliance by taxpayers with respect to furnishing of returns of income.

The above interplay of section 206AB with Section 194Q is an insight into the newly introduced provisions with respect to withholding taxes on goods. It is essential to understand that provisions of section 206AB also come to play with respect to various TDS provisions under the Income Tax Law. Accordingly, it becomes essential for organizations to prepare themselves for a closer look at payee’s status of tax compliance while making withholding tax compliance.

The article has been contributed by:

Sr. Manager-Direct Tax

Further, we shall be happy to assist in case of any clarifications. For a deeper discussion, feel free to revert us at services@knmindia.com

Disclaimer: Information in this note is intended to provide only a general update of the subjects covered. It is not intended to be a substitute for detailed research or the exercise of professional judgment. KNM accepts no responsibility for loss arising from any action taken or not taken by anyone using this publication.