BACKGROUND

According to Income Tax Act, Permanent Establishment is defined as a fixed place of business where the business of the enterprise is wholly or partly carried on that indicates a business connection between the foreign country and Indian country.

The tax on foreign entities in India is based on different aspects such as place of income, source of income and presence of the entity in India. So, with the increase of global business presence in India, the concept of PE has gained importance. PE is used to determine the right of source state to tax business profits of the foreign enterprise.

Article 7 states as “The profits of an enterprise of a Contracting State shall be taxable only in that State unless the enterprise carries on business in the other Contracting State through a permanent establishment situated therein.”

MEANING

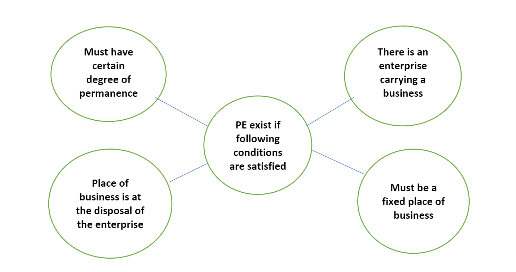

The term “permanent establishment” means a fixed place of business through which the business of an enterprise is wholly or partly carried on.

Article 5(2) specifically includes certain establishments within PE:

- a place of management;

- a branch;

- an office;

- a factory;

- a workshop;

- a mine, an oil or gas well, a quarry or any other place of extraction of natural resources;

- a warehouse in relation to a person providing storage facilities for others;

- a farm, plantation or other place where agriculture, forestry, plantation or related activities are carried on;

- an installation or structure used for the exploration or exploitation of natural resources, but only if so, used for a period of more than 183 days

The establishments mentioned are more by way of illustration. Hence, even an establishment that is not mentioned therein could well constitute a PE Article 5(4) provides that use of the facilities for certain kinds of activities would not constitute a PE.

ACTIVITIES THAT ARE NOT CONSIDERED AS PE:

- The use of facility for the purpose of storage or display of goods

- Maintenance of stock for the purpose of storage or display

- Maintenance of stock belonging to other enterprise for the purpose of processing by other enterprise

- Maintenance of fixed place of business solely for the purpose of purchasing goods or merchandise of collecting information

- Activities which have a preparatory or auxiliary character

- Maintenance of fixed place of business for any combination mentioned above

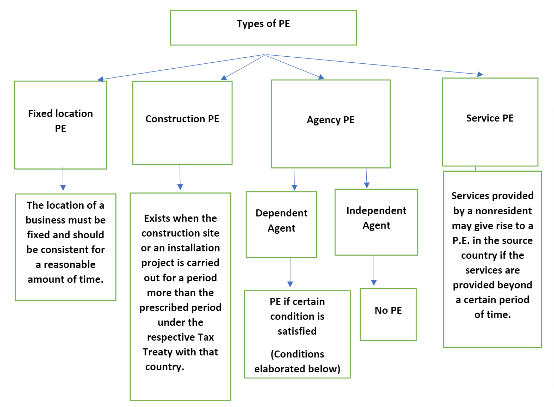

TYPES OF PE:

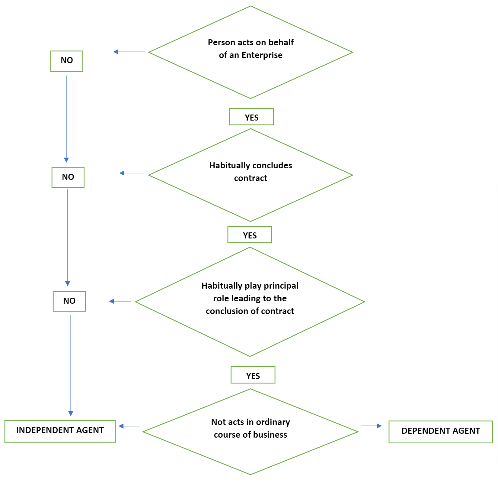

DEPENDENT AGENTS’ CONDITIONS:

CONSEQUENCES OF ESTABLISHMENT OF PE IN INDIA:

CONSEQUENCES OF ESTABLISHMENT OF PE IN INDIA:

Once it is determined that a foreign firm has a PE in India, profits linked to its activities in India will be taxed as “Business Income” in accordance with Article 7 of the treaties.

- Once PE is established profits linked to its activities in India will be taxed as business income.

- Compulsory maintenance of books of accounts.

- Must apply for TAN, PAN and should be registered under regulations of Indirect Taxation

- Mandatory compliance with With-Holding Tax (WHT)

- Expenses incurred for the purpose of the PE’s business, whether incurred in India or elsewhere, are allowed as tax-deductible expenses for determining the PE’s earning

CONCLUSION

PE is the most crucial concept to understand for any enterprise that operates across borders. This is the principal means through which an enterprise may be exposed to corporate income tax, value-added tax, filing tax returns, and compliance with a range of other obligations in the country of source.

KNM India can assist you with a range of complete financial services that range from Corporate advisory to Transaction advisory, Pre-incorporation to Post-incorporation, Insolvency and bankruptcy code to Secretarial services, Assurance to Internal audit services, along with Market entry strategy to Foreign company registration in India. To discuss any of these please book your slot, or call us on +91-99105-04170 – or email us at services@knmindia.com to get a quick response.