CONTENTS

1. General update on Covid-19

2. Change in TCS-Section 206C & its implications

3. Change in TDS-Section 194-O & its implications

1. General update on Covid-19

The 2019–20 coronavirus pandemic is an ongoing pandemic of coronavirus disease 2019 (COVID-19) caused by severe acute respiratory syndrome coronavirus (SARS-CoV-2). The disease was first identified in December 2019 in Wuhan, the capital of China’s Hubei province, and has since spread globally, resulting in the ongoing coronavirus pandemic. The World Health Organization (WHO) declared the 2019–20 coronavirus outbreak a Public Health Emergency of International Concern on January 30, 2020 and a pandemic on March 11, 2020.

| Countries impacted Countries | 215 |

| Total Cases as on September 17, 2020 | 30,042,776 |

| Total deaths as on September 17, 2020 | 945,166 |

| Recovered Cases as on September 17, 2020 | 21,808,582 |

Updated on September 17, 2020 till 6:49 GMT

*Please note that total countries includes territories and international conveyances also.

TABLE-1: ECONOMIC OUTLOOK FOR MAJOR ECONOMIES

| Real y-o-y growth (%) | ’19 | ’20 | ‘21 |

| Gross Domestic Product | |||

| World | 2.9 | -4.4 | 4.0 |

| US | 2.2 | -5.9 | 1.5 |

| Eurozone | 1.3 | -8.9 | 4.3 |

| -Germany | 0.6 | -5.8 | 3.7 |

| -France | 1.5 | -11.0 | 6.6 |

| -Italy | 0.3 | -10.8 | 4.6 |

| -Spain | 2.0 | -13.8 | 5.3 |

| -Netherlands | 1.6 | -5.2 | 2.1 |

| United Kingdom | 1.5 | -10.5 | 4.4 |

| China | 6.1 | 1.2 | 4.7 |

| Japan | 0.7 | -4.9 | 2.9 |

| Brazil | 1.1 | -5.9 | 3.6 |

| India | 4.8 | -4.8 | 9.0 |

| Australia | 1.8 | -5.5 | 3.2 |

| Level in US dollars | |||

| Oil | 64 | 41 | 50 |

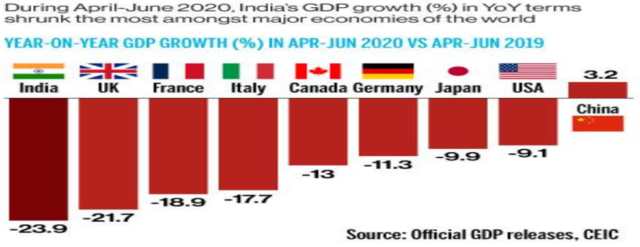

India GDP Growth

In 2019-20, the Indian economy grew by 4.2% against 6.1% expansion in 2018-19. Economic growth slowed to an 11-year low of 4.2% in 2019-20, according to data released by the National Statistical Office.

ØMoody’s has projected India’s real GDP to contract by 11.5 % in FY21, reported against to 2.5%

ØIndia Ratings and Research, the India GDP growth forecast for FY21 was revised further down to a contraction of 11.8 % from the earlier contraction of 5.3%.

ØFitch Ratings has revised India’s GDP outlook for FY21, stating that it will contract 10.5 %, as against an earlier estimate of 5 % contraction.

ØGoldman Sachs estimated real GDP growth to contract 14.8%, in FY21.

Economists at State Bank of India projected a negative growth of 10.9 %.

CHANGING CONSUMER BEHAVIOR DURING THE PANDEMIC

WHAT’S THE NEXT–NORMAL

GUIDELINES ON UNLOCK 4, WILL BE IN FORCE UP TO SEPTEMBER 30, 2020

In areas outside the containment Zones, all activities will be permitted, except the following:-

1.Schools, colleges, educational and coaching institutions will continue to remain closed for students and regular class activity up to September 30. However, Online/distance learning shall continue to be permitted and shall be encouraged.

2.Cinema halls, swimming pools, entertainment parks, theatres and similar places will remain closed. However, open air theatres will be permitted to open with effect from September 21, 2020.

3.International air travel of passengers, except as permitted by MHA.

4.Social/academic/sports/entertainment/cultural/religious/political functions and other congregations with a ceiling of 100 persons, will be permitted with effect from September 21, 2020, with mandatory wearing of face masks, social distancing, provision for thermal scanning and hand wash or sanitizer.

2. Change in TCS-Section 206C & its implications

Background

Indian Income Tax act has the provisions for tax collection at source. Section 206C of the Income-tax act governs the goods on which the seller has to collect tax from the buyer at the time of sale. In order to widen the tax brackets Government has come forward with some more item to be covered. New Item has been proposed in the Union Budget 2020 and was applicable from April, 01st 2020 but later on as per Finance Act 2020, it will be applicable from October, 01st 2020.

Let’s discuss the provisions of TCS in detail:

ØItem covered

- Existing Covered Item: Existing item covered under TCS provisions and rates applicable to them

- New Item covered:

a.TCS on Sale of Goods- 206C(1H)

b.TCS on Foreign Remittance & Overseas tour Programme – 206C(1G)

ØGeneral Compliances

- TCS Payments

- TCS Returns & Certificate

- TCS Exemptions

Existing Covered Item:

The rate of TCS is different for goods specified under different categories :

| Type of Goods | %Rates (Relief rate due to covid-19) | Time of Collection |

| Liquor of alcoholic nature, made for consumption by humans | 1 | Debit of amount payable or receipt of such amount, whichever is earlier. |

| Timber wood under a forest leased/other mode than forest leased | 2.5(1.875) | |

| Tendu leaves | 5(3.75) | |

| A forest produce other than Tendu leaves and timber | 2.5 (1.875) | |

| Scrap | 1 (.75) | |

| Minerals like lignite, coal and iron ore | 1 (.75) | |

| Parking lot, Toll Plaza and Mining and Quarrying | 2 (1.5) | |

| Purchase of Motor vehicle exceeding Rs. 10 Lakhs | 1(.75) | Receipt of Sales consideration |

Section 206C(1H) – TCS on Sale of any goods (Except those already covered under this section & Export of Goods out of India)

Applicability: If consideration exceeds INR50 lakhs in a year and TCS will be collected at the time of receipt on the amount exceed INR50 lakhs

Rate :TCS @0.1% (.075% until 31 March 2021 as per Covid-19 relief by the CBDT) (In non PAN/Aadhar case-1%)

Lower Deduction Certificate: No option to get certificate at Lower/Nil rate.

Sellers means whose total sales, gross receipts or turnover from the business carried on by it exceed INR 10 crore during the financial year immediately preceding the financial year but doesn’t include the person as the CG notifies.

Buyer means a person who purchases any goods but does not include:

a.Buyer is liable to deduct TDS and has withheld such amount

b.Buyer is

-Central Government/ State Government/Embassy / High Commission / Legation / Commission / Consulate / Trade Representation of a Foreign State/– Local Authority such as Panchayat, Municipality etc.

– Person importing goods into India

– any other person as notified by the Central Govt. (No notification issued till date).

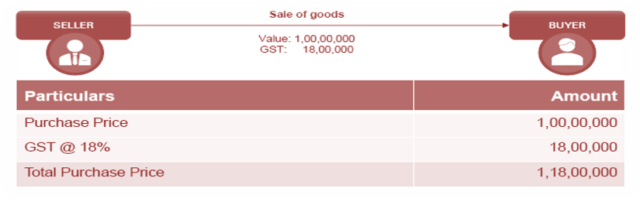

Case Study 1- Whether Sale consideration inclusive of GST or not?

Now CBDT has clarified by Circular no17/2020 that since it’s a collection based tax, so no adjustment is required for any discount, sales return, or indirect taxes

As the provision suggest, Every person, being a seller, who receives any amount as consideration for sale of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year, Therefore the sale price received including GST should be sales consideration. Further clarification from CBDT is awaited

Case Study 2- Whether TCS should be calculated on the ‘total sale consideration’ (i.e. INR 90,00,000) or the sale consideration exceeding INR 50,00,000 (i.e. INR 40,00,000)?

As the provision suggest, Every person, being a seller, who receives any amount as consideration for sale of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year, shall at the time of receipt of such amount, collect TCS from buyer 0.1% of the sale consideration exceeding fifty lakh rupees. (.075% until 31 March 2021 as per Covid-19 relief by the CBDT) Therefore, TCS should be calculated on INR 40,00,000.

Case Study 3- Whether TCS is required to be collected on the receipt of INR 90,00,000?

Now CBDT has confirmed by Circular No. 17/2020 that TCS will be applicable on any amount received on or after Oct 01 2020 for sales done even before Oct, 01 2020

As the provision suggest, Every person, being a seller, who receives any amount as consideration for sale of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year, shall at the time of receipt of such amount, collect TCS from buyer 0.1% of the sale consideration exceeding fifty lakh rupees (.075% until 31 March 2021 as per Covid-19 relief by the CBDT). Therefore, TCS should be calculated on INR 40,00,000 (INR 90,00,000 – INR50,00,000) as the date of receipt is 10th oct, 2020 after provision takes place, if receipt done before provision took place i.e. 1st oct, 2020. then there will be no TCS.

Case Study 4 – Liability of TCS in case of Part Payment

As the provision suggest, Every person, being a seller, who receives any amount as consideration for sale of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year, shall at the time of receipt of such amount, collect TCS from buyer 0.1% of the sale consideration exceeding fifty lakh rupees (.075% until 31 March 2021 as per Covid-19 relief by the CBDT). Therefore TCS should be collected on INR 39,50,00,000 (INR 40,00,00,000 – INR 50,00,000) in October & on INR 20,00,00,000 in January

Case Study 5 – Whether Sale 1 should be considered for calculating the threshold limit of INR 50,00,000?

Now CBDT has confirmed by Circular No.17/2020 that threshold limit will includes sales done for FY 2020-21 (Apr to Mar)

As the provision suggest, Every person, being a seller, who receives any amount as consideration for sale of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year, shall at the time of receipt of such amount, collect TCS from buyer 0.1% of the sale consideration exceeding fifty lakh rupees (.075% until 31 March 2021 as per Covid-19 relief by the CBDT). Therefore Sale 1 should be considered for calculating threshold limit of INR 50,00,000. Although clarification required in this regard..

Case Study 6 – On what amount is TCS payable? Can refund be claimed on TCS pertaining to sales return? If yes, who can claim a refund?

As per the provision, TCS should be collected on INR 1,50,00,000 ( INR 2,00,00,000 – INR 50,00,000) on date of receipt that is 30th Nov, 2020. Now provision does not clarify in relation to Sales Return.

But as per general understanding TCS deposited by seller on INR 25,00,000 can be claimed by buyer while filing of ROI of that year, however there will be mismatch in Form 26AS with books

Case Study 7 – Whether the seller is required to pay TCS? If yes, what is the amount of TCS to be deposited with the government?

As per the provision, TCS should be collected on sale consideration INR 1,50,00,000( INR 2,00,00,000 – INR 50,00000) if buyer refuses still seller is responsible to collect & pay TCS on sale consideration as absolute liability is on seller.

PRIOR ACTION TO BE TAKEN:

- 1.Check applicability for organisation

- 2.Check which customer fall under ambit of this new provision

- 3.Review terms and conditions of commercial agreements already entered by buyer and seller from TCS perspective.

- 4.Amend the Sales-Purchase agreement between the parties by inserting the TCS clause if required.

- 5.Change the format for sales invoice, purchase order, as now you need to intimate your customers for collection of TCS and same can be intimated in T&C section/Footnote of your invoice.

- 6.Existing domestic Letter of Credit (LC) need to be reviewed from prospective of TCS.

Section 206C(1G) – TCS on foreign remittance & Overseas tour Programme

a.Remittance through Liberalised Remittance Scheme(LRS): An authorised dealer receiving an amount or an aggregate of amounts of INR 7 lakhs or more in a financial year for remittance out of India shall be liable to collect TCS from the buyer-

- under the LRS of RBI –@5% (In non PAN/Aadhar case-10%)

- for the purpose any education if such remittance is out of loan obtained from any financial institute as defined by Section 80E-@0.5% (In non PAN/Aadhar case-5%)

of the amount remitted in excess of INR 7 lakhs.

Note: Currently under LRS, USD 250000 is allowed to remit by the Resident Individual.

b.Overseas tour Programme Package: A seller of an overseas tour program package who receives any amount from any buyer, being a person who purchases such package, shall be liable to collect TCS @5%. (In non PAN/Aadhar case-10%)

Here overseas tour Programme includes expenses for travel or hotel stay or boarding or lodging or any other expense of similar nature or in relation thereto.

Exception:

a)Authorised dealer shall not collect the sum on an amount in respect of which the sum has been collected by the seller

b)buyer is liable to deduct TDS and has withheld such amount

c)buyer is Central Government/ State Government/ Embassy / High Commission / Legation / Commission / Consulate / Trade Representation of a Foreign State

– Local Authority such as Panchayat, Municipality etc.,

–Any other person as notified by the Central Government (No notification issued till date).

Lower Deduction Certificate: There is No option to obtain certificate at Lower / Nil rate.

Case Study:

- Whether TCS on foreign remittance through Liberalised Remittance Scheme (LRS) will be applicable on entire amount of remittance or only on excess of Rs 7 Lacs?

Eg: (I)Transaction 1 – Rs. 5,00,000

(II)Transaction 2 – Rs 8,00,000

Ans: TCS shall be applicable on amount in excess of ₹ 7 lakhs in a financial year and not on the total amount.

| Transaction | TCS Applicability |

| Transaction 1 – Rs. 5,00,000 | No Tax will be collected since the amount is below Rs 7,00,000/- |

| Transaction 2 – Rs 8,00,000 | TCS will be applicable on Rs 1,00,000 (If we aggregate Transaction 1 & Transaction 2 then TCS will be collected on Rs.6,00,000) |

2. Whether all foreign remittance transactions through Liberalised Remittance Scheme (LRS) will be charged at 5%?

Ans: Normally, Yes all remittance out of India under the LRS of RBI, shall be liable to collect TCS at 5%. But in non-PAN/Aadhaar cases the rate shall be 10%.

TCS Payment:

The seller deposits the TCS amount in Challan 281 within 7 days from the last day of the month in which the tax was collected. TCS for the month of March will be paid on or before May 15th of next Financial year.

*All sums collected by an office of the Government should be deposited on the same day of collection.

TCS Return & Certificate

Every tax collector has to submit quarterly TCS return i.e. in Form 27EQ in respect of the tax collected by him in a particular quarter. Form 27D is the certificate issued for TCS returns filed.

| Quarter Ending | Date for Filing of Form 27EQ | Date for generating Form 27D |

| -on 30th June | 15th July | 30th July |

| -on 30th September | 15th October | 30th October |

| -on 31st December | 15th January | 30th January |

| -on 31st March | 15th May | 30th May |

TCS Exemptions(for existing covered Items)

Tax collection at source is exempted in the following cases :

1.When the eligible goods are used for personal consumption.

2.The purchaser buys the goods for manufacturing, processing or production and not for the purpose of trading of those goods.

- Note: If the tax collector responsible for collecting the tax and depositing the same to the government does not collect the tax or after collecting doesn’t pay it to the government as per above due dates, then he will be liable to pay interest of 1% per month or a part of the month.

- Note Penalty to failure to collect or pay is equals to TCS amount and the person responsible to collect shall become assessee in default, however for earlier item covered there is relaxation.

3. Change in TDS -Section 194O & its implications

Background

Section 194-O has been proposed in the Union Budget 2020 and was applicable from April, 01st 2020 but later on as per Finance Act 2020, it will be applicable from October, 01st 2020. According to Section 194-O, an e-Commerce operator is required to deduct TDS for facilitating any sale of goods or providing services through an e-Commerce participant. Here E-Commerce means the supply of goods or services or both, including digital products, over digital or electronic network. Earlier, there was no tax deduction on payments made to e-Commerce participants. There are many small e-Commerce participants didn’t file their income tax returns and escaped the tax liability, now they were required to independently file their income tax returns.

Let’s discuss the provisions of Section 194-O in detail:

- Purpose of Section 194-O

- Who are e-Commerce operators and participants?

- Scope of Section 194-O

- exceptions to Section 194-O, if any

- Conclusion.

Purpose of Section 194-O

Often, customers prefer digital platforms for buying or selling of goods and services because:

From the sellers’ perspective: It requires less cost for creating the setup and less effort for the search of buyers.

From the buyers’ perspective: Many options are available at one platform and the comparison of products becomes very easy. This has resulted in an increase in the number of e-Commerce users over a period of time.

Income tax authorities already introduced provisions of Equalization levy to make a check on Non-resident E-commerce Participant, however there is no such provision exist for Resident one. In order to bring the parity & to increase the taxation base, finance act 2020 come up with new section 194-O in the chapter XVIIB. By introduction of Section 194-O TDS base is widen enough to brings the Resident e-Commerce participants under the tax net.

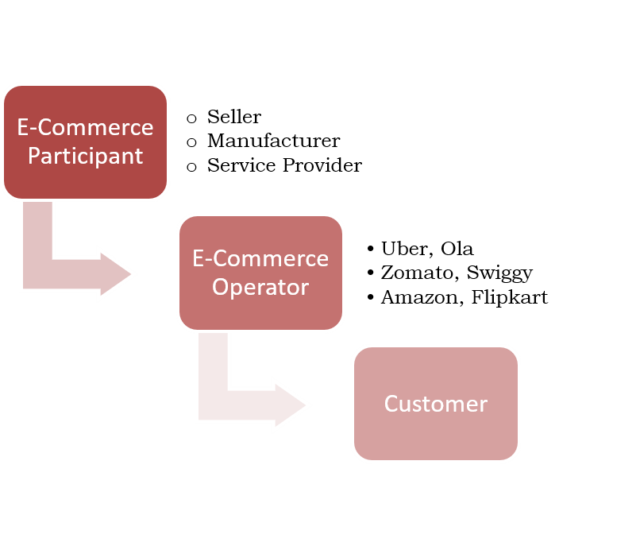

Who are e-Commerce operators and participants?

“e-Commerce participant” means a person resident in India selling goods or providing services or both, including digital products, through digital or electronic facility or platform for electronic commerce.

“e-Commerce operator’’ An e-Commerce operator is a person who owns, operates, or manages a digital or electronic facility or platform for supply of goods or services or both, including digital products, over digital or electronic network.

Note: Residential status of e-Commerce operator doesn’t matter here.

Scope of Section 194-O

An e-Commerce operators shall deduct TDS @1% (now reduced to 0.75% upto March 31st 2021 on account of COVID-19 relief) economic relief) at the time of credit of the amount of sale of goods, services, or both to the account of an e-commerce participant or at the time of making payment to an e-Commerce participant by any other mode, whichever is earlier.

Condition for Applicability of TDS:

| Condition | For Individual or HUF | Other than Individual or HUF |

| Sale/Service Amount or both | Gross Amount of Sale/Service or both>INR 5 Lakh & | _ |

| PAN or Aadhar | Furnish PAN or Aadhar- If not then rate of TDS will be 5% as per section 206AA | If not then rate of TDS will be 5% as per section 206AA |

Note: For the purposes of this section, e-commerce operator shall be deemed to be the person responsible for paying to e-commerce participant directly.

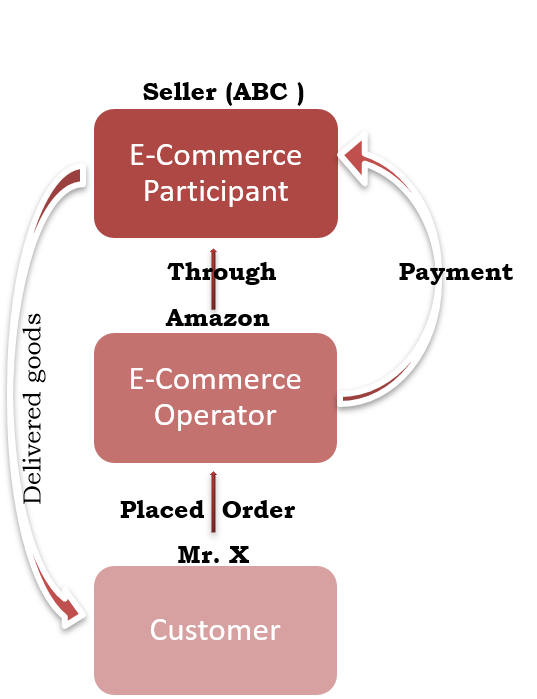

Example 1

Key facts:

- A proprietary firm ABC (e-commerce participant) is selling its products through Amazon (e-commerce operator).

- Mr. X buys this product online from ABC for Rs 6,00,000 on 2nd October 2020.

- Amazon credits the account of ABC on 1st October 2020, and Amazon made payment to XYZ on 9th October 2020.

Here, Amazon is required to deduct TDS @1% on Rs 6,00,000 at the time of credit to the party or making payment, whichever is earlier. In this case, TDS should be deducted on 2nd October 2020.

Note: Rate of TDS now reduced to 0.75% upto March 31st ,2021 on account of COVID-19 relief)

Now CBDT has confirmed by Circular No.17/2020 that threshold limit will includes sales or services of both done for FY 2020-21 (Apr to Mar)

Example 2

Key facts:

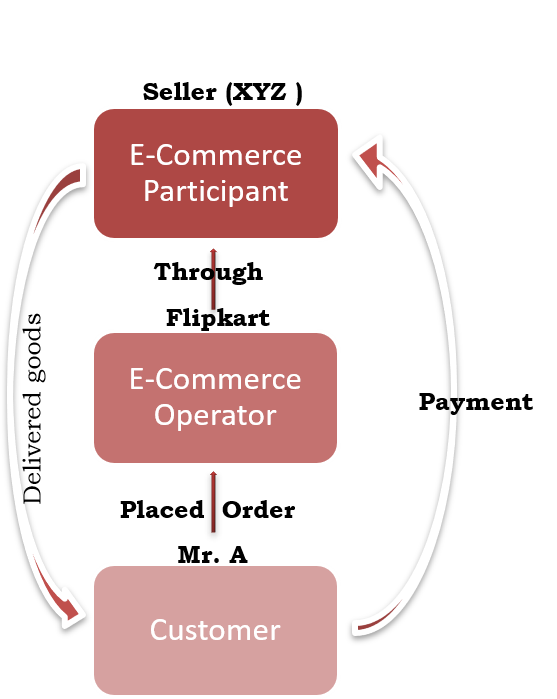

- A proprietary firm XYZ (e-commerce participant) is selling its products through Flipkart (e-commerce operator).

- Mr. A buys this product online from XYZ for Rs 50,000 on 1st October 2020.

- Flipkart credits the account of XYZ on 1st October 2020, but the customer makes the payment directly to XYZ on 15th October 2020.

Here, Flipkart is required to deduct TDS @1% on Rs 50,000 at the time of credit to the party or making payment, whichever is earlier. In this case, TDS should be deducted on 1st October 2020.

Note: Rate of TDS now reduced to 0.75% upto March 31st ,2021 on account of COVID-19 relief)

Exceptions to Section 194O, if any

Non-resident e-Commerce participants are exempted from the scope of this section however, they might be covered under Equalization Levy u/s 165A of Equalization Levy Act.

- A ceiling limit of Rs. 5 lakh is set only for resident individuals and HUF. Thus, an e-Commerce operator is not required to deduct TDS if the amount, paid or credited to individuals/HUF during a financial year, does not exceed Rs. 5 lakh.

Conclusion:

The introduction of Section 194-O shall result in an increase in the tax revenue for the government by brining the more taxpayer in tax net.