Executive Summary

Income Tax

- Cost inflation Index (CII) under section 48 for financial year 2024-25

- Exemption under section 10 (46) of Income of Tamil Nadu Water Supply and Drainage Board subject to few conditions.

- CBDT releases new functionality in AIS For Taxpayers.

- CBDT issues guidelines for compulsory selection of Income-tax Returns (ITRs) for complete scrutiny during FY 2024-25

Goods And Service Tax (GST)

- Advisory on launch of E-Way Bill 2 Portal

- Information from manufacturers of Pan Masala and Tobacco taxpayer

Companies Act 2013/ Other Laws

- Relaxation of Additional Fees and Extension of Last Date of Filing of Form No. LLP BEN 2 and LLP Form No. 4D under the Limited Liability Partnership Act, 2008

- RBI decides to regularize prior issuance of partly paid units by AIFs to non-residents via compounding under FEMA

- SEBI strengthens risk management framework for Clearing Corporations (CCs);

- SEBI updates Investor Charter for stock exchanges and depositories to include new services and guidelines

- Master Circular for Issue and Listing of Non-convertible Securities, Securitised Debt Instruments, Security Receipts, Municipal Debt Securities and Commercial Paper

![]()

![]()

- Cost inflation Index under section 48 For Financial Year 2024-25

- In exercise of the powers conferred by clause (v) of the Explanation to section 48 of the Income-tax Act, 1961, the Central Government hereby makes the following further amendments in the notification published in the Gazette of India, Extraordinary, Part II, section 3, sub-section (ii) number O. 1790(E), dated the 5th June, 2017, namely: —

- In the said notification, in the Table, after serial number 23 and the entries relating thereto, the following serial number and entries shall be inserted, namely: –

TABLE

| Sl. No. | Financial Year | Cost Inflation Index |

| (1) | (2) | (3) |

| “24 | 2024-25 | 363″ |

- This notification shall come into force with effect from the assessment year 2025-26 and subsequent assessment years.

- Exemption under section 10 (46) of Income of Tamil Nadu Water Supply and Drainage Board subject to few conditions.

- In exercise of the powers conferred by clause (46) of section 10 of the Income-tax Act, 1961 (43 of 1961), the Central Government hereby notifies for the purposes of the said clause, ‘Tamil Nadu Water Supply and Drainage Board, Chennai’ (PAN: AAALT0834F), a Board constituted under the Tamil Nadu Water Supply and Drainage Board Act, 1970 (Tamil Nadu Act of 1971), in respect of the following specified income arising to the said Board, namely: —

- Water charges for supply of water to recover the maintenance cost.

- Centage charges received from local bodies work like water supply scheme and sewerage scheme to compensate for establishment charges.

- Investigation and Detailed Project Report preparation charges for water supply and drainage scheme for establishment charges.

- Interest earned on Bank Deposits.

- This notification shall be effective subject to the conditions that Tamil Nadu Water Supply and Drainage Board, Chennai-

- shall not engage in any commercial activity.

- its activities and the nature of the specified income shall remain unchanged throughout the financial year(s); and

- shall file return of income in accordance with the provision of clause (g) of sub-section (4C) of section 139 of the Income-tax Act, 1961.

- This notification shall be applicable from AY 2024-25 to AY 2028-29.

- CBDT Releases new functionality in AIS For Taxpayers

In AIS, taxpayers have been provided with a functionality to furnish feedback on every transaction displayed therein. This feedback helps the taxpayer to comment on the accuracy of the information provided by the Source of such information. In case of wrong reporting, the same is taken up with the Source for their confirmation, in an automated manner. It may be noted that information confirmation is currently made functional with regard to information furnished by Tax Deductors /Collectors and Reporting Entities.

The Central Board of Direct Taxes (CBDT) has now rolled out a new functionality in AIS to display the status of information confirmation process. This will display whether the feedback of the taxpayer has been acted upon by the Source, by either partially or fully accepting or rejecting the same. In case of partial or full acceptance, the information is required to be corrected by filing a correction statement by the Source. The following attributes shall be visible to the taxpayer for status of Feedback confirmation from Source.

- Whether Feedback is shared for confirmation: – This will let the taxpayer know if the feedback has been shared with the Reporting Source for confirmation or not.

- Feedback Shared on: – This will let the taxpayer know the date on which the feedback has been shared with the Reporting Source for confirmation.

- Source responded on: – This will let the taxpayer know the date on which the Reporting Source has responded on the feedback shared with it for confirmation.

- Source response: – This will let the taxpayer know the response provided by the Source on the taxpayer’s feedback.

- The CBDT has issued parameters and procedures for compulsory selection of ITRs during FY 2024-25, in below cases.

- Cases pertaining to Survey u/s 133A of the Income-tax Act

- Cases pertaining to Search & Seizure

- Cases in which notice u/s 142(1) of the Income-tax Act has been issued, but no ITR has been furnished

- Cases in which notice u/s 148 has been issued,

- Cases relating to to registration / approval of charitable trusts / institutions claiming tax exemption

- Cases involving addition in an earlier Assessment Year on a recurring issue of law / fact

- Cases relating to specific information regarding tax evasion

![]()

![]()

- Advisory on launch of E0way Bill 2 Portal:

GSTN is pleased to inform that NIC is releasing the E-Way Bill 2 Portal (https://ewaybill2.gst.gov.in) on 1st June 2024. This portal ensures high availability and runs in parallel to the e-way Bill main portal. The e-way bill 2 portal synchronizes the e-way bill details with main portal within a few seconds. The highlights of the portal are as follows-:

- Presently, E-Way Bill 2 Portal provides the critical services of E-Way Bill system, and gradually it will be extended with other services of e-way bill system.

- E-Way Bills can be generated and updated on the E-Way Bill 2 Portal independently.

- E-Way Bill 2 portal provides the web and API modes of operations for e-way bill services.

- The taxpayers and logistic operators can use the E-Way Bill 2 portal with the login credentials of the main portal.

- The taxpayers and logistic operators can use the E-Way Bill 2 portal during technical glitches in e-way bill main portal or any other exigencies.

- The Criss-Cross operations of printing and updating of Part-B of E-Way Bills can be carried out on these portals. That is, updating of Part-B of the E-Way bills of portal 1 can be done at portal 2 and vice versa.

- In case E-Way Bill main portal is non-operational because of technical reasons, the Part-B can be updated to the E-Way Bills, generated at Portal 1, at portal 2 and carry both the E-way Bill slips.

- For further details, please visit the e-way bill portals.

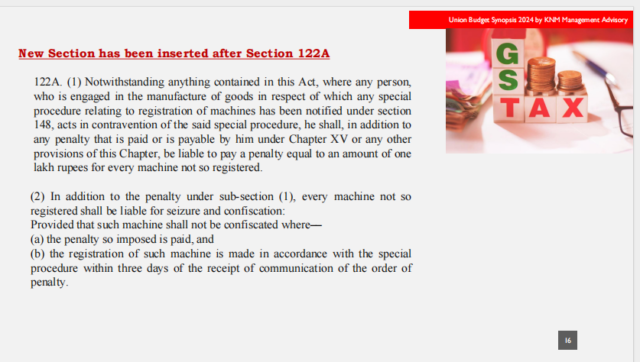

- Information from manufacturers of Pan Masala and Tobacco taxpayers:

The government had issued a notification to seek information from taxpayers dealing in the goods mentioned therein vide Notification No. 04/2024 – Central Tax dated 05-01-2024. Two forms have been notified vide this notification namely GST SRM-I and GST SRM-II. The former pertains to registration and disposal of machines while the later asks information on inputs and outputs during a month.

To begin with, facility to register the machines have been made available on the GST Portal to file the information in Form GST SRM-I. All taxpayers dealing in the items mentioned in the said notification may use the facility to file the information about machines. Form GST SRM-II will also be made available on the portal shortly.

![]()

![]()

- Relaxation of additional fees and extension of last date of Filing of Form No. LLP Ben 2 and LLP form no. 4D under The Limited Liability Partnership Act, 2008

The Ministry of Corporate Affairs (MCA) has notifed that relaxation of additional fees and extension of last date of filing of Form No. LLP BEN-2 and LLP Form No. 4 under the Limited Liability Partnership Act, 2008 in the view of transition of MCA-21 from version- to version-3. These forms shall be filed without any addition fees upto July 01, 2024.

![]()

![]()

- RBI decides to regularize prior issuance of partly paid units by AIFs to non-residents via compounding under FEMA

The Reserve Bank of India (“RBI”) vide its circular dated May 21, 2024 (“Circular”) has required that issuance of partly paid-up units by Alternative Investment Funds (“AIFs”) to foreign investors prior to March 14, 2024, should be regularised through compounding under Foreign Exchange Management Act, 1999 (“FEMA”). Compounding by RBI is prescribed for the contravention of foreign exchange regulations as per Foreign Exchange (Compounding Proceedings) Rules, 2000, and involve payment of a fees. In many instances, compounding requires payment of a monetary penalty to RBI.

![]()

![]()

- SEBI strengthens risk management framework for Clearing Corporations (CCs)

SEBI has reviewed the existing collaterals accepted by CCs and specified the prudential norms for exposure of CCs. As per the amended norms units of growth plan of overnight mutual fund schemes shall be accepted as Cash Equivalent by CCs with a haircut of 5%. Earlier, a limit of 10% was specified. The 10% haircut remains unchanged for other overnight mutual fund plans. Further, the Prudential Norms for Exposure of CCs has also been specified. The circular shall be effective from 01st Aug, 2024.

- SEBI updates Investor Charter for stock exchanges and depositories to include new services and guidelines

In November 2021, SEBI formulated the Investor Charter for Depositories/ Depository Participants (DPs) and Stock exchanges. It contains information on services provided to investors, such as grievance redressal mechanisms, rights and obligations of investors, etc. With the recent introduction of the Online Dispute Resolution (ODR) platform and SCORES 2.0 by SEBI, the Investor Charter has been updated to incorporate these new services.

- Master Circular for Issue and Listing of Non-convertible Securities, Securitised Debt Instruments, Security Receipts, Municipal Debt Securities and Commercial Paper

The Securities and Exchange Board of India has consolidated all the applicable circulars/ directions at one place which are applicable for for Issue and Listing of Non-convertible Securities, Securitised Debt Instruments, Security Receipts, Municipal Debt Securities and Commercial Paper, till May 21, 2024.

![]()

![]()

Disclaimer: Information in this note is intended to provide only a general update of the subjects covered. It is not intended to be a substitute for detailed research or the exercise of professional judgment. KNM accepts no responsibility for loss arising from any action taken or not taken by anyone using this publication. Updates are for the period 30.05.2024.